10B2 - Calculator HP - Free user manual and instructions

Find the device manual for free 10B2 HP in PDF.

| Product Type | Financial Calculator |

| Brand | HP |

| Model | 10B2 |

| Dimensions | Approximately 15 x 8 x 1.5 cm |

| Weight | Approximately 120 g (with batteries) |

| Power Source | 2 LR44 / AG13 button cell batteries |

| Display | 12-digit LCD screen |

| Main Functions | Financial calculations (NPV, IRR, amortization), statistics, percentages, memory |

| Maintenance and Cleaning | Wipe with a soft, dry cloth. Do not use solvents. |

| Safety | No special conditions. Keep out of reach of young children. |

| Spare Parts and Repairability | User-replaceable batteries. No user-serviceable internal parts. |

| General Information | Made in China. Complies with Canadian electromagnetic compatibility (EMC) standard Class B. |

Frequently Asked Questions - 10B2 HP

User questions about 10B2 HP

0 question about this device. Answer the ones you know or ask your own.

Ask a new question about this device

Download the instructions for your Calculator in PDF format for free! Find your manual 10B2 - HP and take your electronic device back in hand. On this page are published all the documents necessary for the use of your device. 10B2 by HP.

USER MANUAL 10B2 HP

hp 10BII financial calculator

user's guide

i n v e n t

Edition 1

HP part number F1902-90001

Notice

REGISTER YOUR PRODUCT AT: www.registerer.hp.com

THIS MANUAL AND ANY EXAMPLES CONTAINED HEREIN ARE PROVIDED "AS IS" AND ARE SUBJECT TO CHANGE WITHOUT NOTICE. HEWLETT-PACKARD COMPANY MAKES NO WARRANTY OF ANY KIND WITH REGARD TO THIS MANUAL, INCLUDING, BUT NOT LIMITED TO, THE IMPLIED WARRANTYES OF MERCHANTABILITY, NON-INFRINGEMENT AND FITNESS FOR A PARTICULAR PURPOSE.

HEWLETT-PACKARD CO. SHALL NOT BE LIABLE FOR ANY ERRORS OR FOR INCIDENTAL OR CONSEQUENTIAL DAMAGES IN CONNECTION WITH THE FURNISHING, PERFORMANCE, OR USE OF THIS MANUAL OR THE EXAMPLES CONTAINED HEREIN.

Copyright 1988, 1989, 2001, 2004 Hewlett-Packard Development Company, L.P. Reproduction, adaptation, or translation of this manual is prohibited without prior written permission of Hewlett-Packard Company, except as allowed under the copyright laws.

Hewlett-Packard Company

4995 Murphy Canyon Rd,

Suite 301

San Diego, CA 92123

Welcome to the HP 10BII

Your HP 10BII reflects the superior quality and attention to detail in engineering and manufacturing that have distinguished Hewlett-Packard products for 60 years. Hewlett-Packard stands behind this calculator—we offer expertise to support its use (see inside the back cover) and worldwide service.

Hewlett-Packard Quality

Our calculators are made to excel and to be easy to use.

This calculator is designed to withstand the drops, vibrations, pollutants (smog, ozone), temperature extremes, and humidity variations that it may encounter in everyday work life.

The calculator and its manual have been designed and tested for ease of use. We added many examples to highlight the varied uses of the calculator.

- Low-power electronics and an advanced power management system gives extended battery life.

- The microprocessor has been optimized for fast and reliable computations using 15 digits internally for precise results.

- Extensive research has created a design that has minimized the adverse effects of static electricity, a potential cause of malfunctions and data loss in calculators.

Features

The features of the HP 10BII and the manual reflect the needs and wishes of many customers:

A large 12-character display.

An At-a-Glance section in the manual for quick reference.

Applications to solve business and financial tasks:

- Time Value of Money. Loans, savings, leases, and amortization schedules.

- Interest Conversion. Nominal and effective rates.

- Cash Flows. Net present value and internal rate of return.

- Business Percentages. Percent change, markup, and margin calculations.

-

Statistics. Mean, standard deviation, correlation coefficient, and linear regression forecasting, plus other statistical calculations.

-

Enough memory to store an initial cash flow and 14 cash flow groups, with up to 99 cash flows per group.

Ten numbered storage registers.

Easy access to functions saves keystrokes and adds convenience. -

Auto-increment capability for amortization schedules.

-

Labels for amortization and cash flows.

Automatic constant.

3-key memory. -

Many examples are included in the manual so you can combine them for your specific needs.

Contents

11 At a Glance...

11 Basics—At a Glance...

12 Percentages—At a Glance...

13 Memory Keys—At a Glance...

14 Time Value of Money (TVM)—At a Glance...

15 TVM What if...—At a Glance...

16 Amortization—At a Glance...

17 Interest Rate Conversion—At a Glance...

18 IRR/YR and NPV—At a Glance...

19 Statistics—At a Glance...

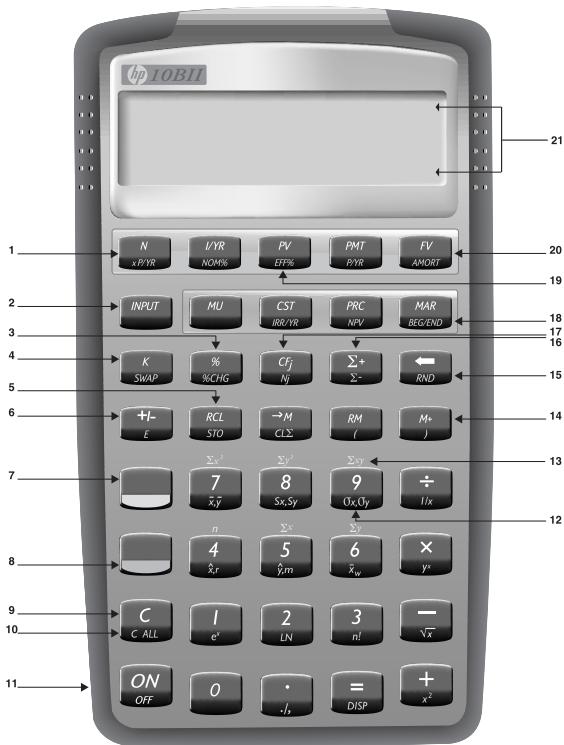

21 Keyboard Map

1 23 Getting Started

23 Power On and Off

23 Adjusting the Display Contrast

23 Simple Arithmetic Calculations

25 Understanding the Display and Keyboard

25 Cursor

25 Clearing the Calculator

25 Clearing Memory

26 Annunciators

27 Shift Key

27 Statistics Key

28 INPUT Key

28 SWAP Key

28 Math Functions

29 Display Format of Numbers

30 Specifying Displayed Decimal Places

30 Scientific Notation

31 Displaying the Full Precision of Numbers

31 Interchanging the Period and Comma

32 Rounding Numbers

32 Messages

| 2 | 33 | Business Percentages |

| 33 | Percent Key | |

| 33 | Finding a Percent | |

| 34 | Adding or Subtracting a Percent | |

| 34 | Percent Change | |

| 35 | Margin and Markup Calculations | |

| 35 | Margin Calculations | |

| 35 | Markup on Cost Calculations | |

| 36 | Using Margin and Markup Together | |

| 3 | 37 | Number Storage and Arithmetic |

| 37 | Using Stored Numbers in Calculations | |

| 37 | Using Constants | |

| 39 | Using the M Register | |

| 40 | Using Numbered Registers | |

| 41 | Doing Arithmetic Inside Registers | |

| 42 | Doing Arithmetic | |

| 43 | Power Operator | |

| 43 | Using Parentheses in Calculations | |

| 4 | 45 | Picturing Financial Problems |

| 45 | How to approach a Financial Problem | |

| 46 | Signs of Cash Flows | |

| 47 | Periods and Cash Flows | |

| 47 | Simple and Compound Interest | |

| 47 | Simple Interest | |

| 48 | Compound Interest | |

| 49 | Interest Rates | |

| 49 | Two Types of Financial Problems | |

| 49 | Recognizing a TVM Problem | |

| 51 | Recognizing a Cash Flow Problem |

5

53 Time Value of Money Calculations

53 Using the TVM Application

54 Clearing TVM

55 Begin and End Modes

55 Loan Calculations

60 Savings Calculations

63 Lease Calculations

67 Amortization

72 Interest Rate Conversions

72 Investments With Different Compounding Periods

73 Compounding and Payment Periods Differ

6

75 Cash Flow Calculations

75 How to Use the Cash Flow Application

77 NPV and IRR/YR: Discontinuing Cash Flows

77 Organizing Cash Flows

78 Entering Cash Flows

Viewing and Replacing Cash Flows

80 Calculating Net Present Value

83 Calculating Internal Rate of Return

84 Automatic Storage of IRR/YR and NPV

7

85 Statistical Calculations

85 Clearing Statistical Data

86 Entering Statistical Data

86 One-Variable Statistics

86 Two-Variable Statistics and Weighted Mean

87 Correcting Statistical Data

87 Correcting One-Variable Data

87 Correcting Two-Variable Data

87 Summary of Statistical Calculations

88 Mean, Standard Deviations, and Summation Statistics

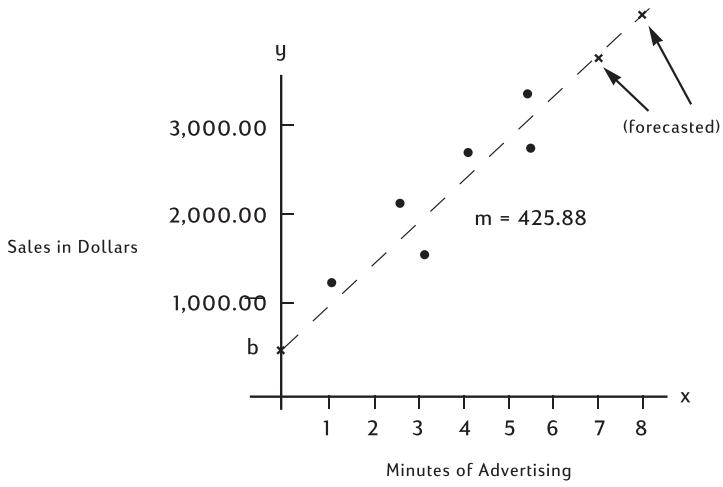

90 Linear Regression and Estimation

93 Weighted Mean

| 8 | 95 | Additional Examples |

| 95 | Business Applications | |

| 95 | Setting a Sales Price | |

| 96 | Forecasting Based on History | |

| 97 | Cost of Not Taking a Cash Discount | |

| 98 | Loans and Mortgages | |

| 98 | Simple Annual Interest | |

| 98 | Continuous Compounding | |

| 99 | Yield of a Discounted (or Premium) Mortgage | |

| 101 | Annual Percentage Rate for a Loan With Fees | |

| 103 | Loan With a Partial (Odd) First Period | |

| 104 | Automobile Loan | |

| 105 | Canadian Mortgages | |

| 106 | What if ... TVM Calculations | |

| 108 | Savings | |

| 108 | Saving for College Costs | |

| 110 | Gains That Go Untaxed Until Withdrawal | |

| 112 | Value of a Taxable Retirement Account | |

| 113 | Cash Flow Examples | |

| 113 | Wrap-Around Mortgages | |

| 115 | Net Future Value | |

| A | 117 | Assistance, Batteries, and Service |

| 117 | Answers to Common Questions | |

| 118 | Environmental Limits | |

| 119 | Power and Batteries | |

| 119 | Low Power Annunciator | |

| 119 | Battery Specifications | |

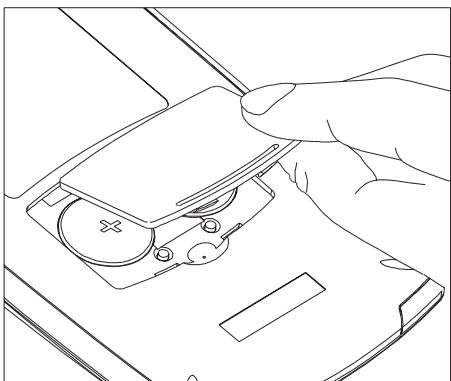

| 119 | Installing Batteries | |

| 121 | Determining if the Calculator Requires Service | |

| 122 | Limited One-Year Warranty | |

| 122 | What Is Covered | |

| 122 | What Is Not Covered | |

| 123 | Consumer Transactions in the United Kingdom |

123 If the Calculator Requires Service

123 Obtaining Service

124 Service Charge

124 Shipping Instructions

124 Warranty on Service

125 Service Agreements

125 Regulatory Information

126 End-user terms and conditions

B 129 More About Calculations

129 IRR/YR Calculations

129 Possible Outcomes of Calculating IRR/YR

130 Halting and Restarting IRR/YR

130 Entering a Guess for IRR/YR

131 Effect of Using - to Correct Data

131 Range of Numbers

132 Equations

132 Margin and Markup Calculations

132 Time Value of Money (TVM)

132 Amortization

133 Interest Rate Conversions

134 Cash-Flow Calculations

135 Statistics

C 137 Messages

139 Index

At a Glance…

This section is designed for you if you're already familiar with calculator operation or financial concepts. You can use it for quick reference. The rest of the manual is filled with explanations and examples of the concepts presented in this section.

Basics—At a Glance…

| Keys: | Display: | Description: |

| ON | 0.00 | Turns calculator on. |

| [orange label] | 0.00 | Displays shift annunciator (SHIFT). |

| 0.00 | Discontinues shift. | |

| 123 | 12_ | Erases last character. |

| C | 0.00 | Clears display. |

| CLE | 0.00 | Clears statistics memory. |

| C ALL | 0.00 | C clears all memory. |

| OFF | Turns calculator off. |

Percentages—At a Glance…

%

Percent.

CST

Cost.

PRC

Price.

MAR

Margin.

MU

Markup.

Add (15\%) to \(17.50.

Keys:

Display:

Description:

17·50+

17.50

Enters number.

①⑤%%

20.13

Adds 15% .

Find the margin if the cost is 15.00 and selling price is22.00.

①⑤⑥

15.00

Enters cost.

②②PRG

22.00

Enters price.

MAR

31.82

Calculates margin.

If the cost is $20.00 and the markup is 33%, what is the selling price?

②①⑤

20.00

Enters cost.

③③MU

33.00

Enters markup.

PRC

26.60

Calculates price.

Memory Keys—At a Glance…

Stores a constant operation.

- M Stores a value in the M register (memory location).

Recalls a value from the M register.

^+ Addsa value to the number stored in the M register.

STO Stores a value in a numbered register.

RCL Recalls a value from a numbered register.

Multiply 17, 22, and 25 by 7, storing “ × 7” as a constant operation.

| Keys: | Display: | Description: |

| ①⑦×⑦⑧ | 7.00 | Stores “× 7” as a constant operation. |

| 三 | 119.00 | Multiplies 17 × 7. |

| ②②三 | 154.00 | Multiplies 22 × 7. |

| ②⑤三 | 175.00 | Multiplies 25 × 7. |

Store 519 in register 2, then recall it.

| 519.00 | Stores in register 2. |

| 0.00 | Clears display. |

| 519.00 | Recalls register 2. |

Time Value of Money (TVM)—At a Glance…

Enter any four of the five values and solve for the fifth.

A negative sign in the display represents money paid out; money received is positive.

N Number of payments.

I/YR Interest per year.

PV Present value.

Payment.

FV Future value.

REGENBegin or End mode.

Number of payments per year mode.

If you borrow $14,000 (PV) for 360 months (N) at 10% interest (I/YR), what is the monthly repayment?

Set to End mode. Press if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 36ON | 360.00 | Enters number of payments. |

| 10IYR | 10.00 | Enters interest per year. |

| 14000PV | 14,000.00 | Enters present value. |

| 0FV | 0.00 | Enters future value. |

| PMT | -122.86 | Calculates payment if paid at end of period. |

TVM What if...—At a Glance…

It is not necessary to reenter TVM values for each example. Using the values you just entered (page 14), how much can you borrow if you want a payment of $100.00?

| Keys: | Display: | Description: |

| 10+/-PMT | -100.00 | Enters new payment amount. (Money paid out is negative.) |

| PV | 11,395.08 | Calculates amount you can borrow. |

How much can you borrow at a 9.5% interest rate?

| 9.50 | Enters new interest rate. |

| 11,892.67 | Calculates new present value for $100.00 payment and 9.5% interest. |

| 10.00 | Reenters original interest rate. |

| 14,000.00 | Reenters original present value. |

| -122.86 | Calculates original payment. |

Amortization—At a Glance…

After calculating a payment using Time Value of Money (TVM), enter the periods to amortize and press AMORT. Then press to continually cycle through the principal, interest, and balance values (indicated by the PRIN, INT, and BAL announcciators respectively).

Using the previous TVM example (page 14), amortize a single payment and then a range of payments.

Amortize the 20^th payment of the loan.

| Keys: | Display: | Description: |

| 20INPUT | 20.00 | Enters period to amortize. |

| AMORT | 20 – 20 | Displays period to amortize. |

| € | -7.25 | Displays principal. |

| € | -115.61 | Displays interest. (Money paid out is negative.) |

| € | 13,865.83 | Displays balance. |

Amortize the 1^st through 12^th loan payments.

| 1 (INPUT) 1 2 | 12_ | Enters range of periods to amortize. |

| AMORT | 1 - 12 | Displays range of periods (payments). |

| = | -77.82 | Displays principal. |

| = | -1,396.50 | Displays interest. (Money paid out is negative.) |

| = | 13,922.18 | Displays balance. |

Interest Rate Conversion—At a Glance…

To convert between nominal and effective interest rates, enter the known rate and the number of periods per year, then solve for the unknown rate.

NOM%

Nominal interest percent.

EFF%

Effective interest percent.

P/YR

Periods per year.

Find the annual effective interest rate of 10% nominal interest compounded monthly.

Keys:

Display:

Description:

0

NOM%

10.00

Enters nominal rate.

2

P/YR

12.00

Enters payments per year.

EFF%

10.47

Calculates annual effective interest.

IRR/YR and NPV—At a Glance...

P/YR

Number of periods per year (default is 12).

Cash flows, up to 15 ("j" identifies the cash flow number).

Number of consecutive times cash flow "j" occurs.

Internal rate of return per year.

Net present value.

If you have an initial cash outflow of 40,000, followed by monthly cash inflows of4,700, 7,000,7,000, and $23,000, what is the IRR/YR? What is the IRR per month?

Keys:

Display:

0.00

12.00

-40,000.00

4,700.00

7,000.00

2.00

23,000.00

15.96

1.33

Description:

Clears all memory.

Sets payments per year.

Enters initial outflow.

Enters first cash flow.

Enters second cash flow.

Enters number of consecutive times cash flow occurs.

Enters third cash flow.

Calculates IRR/YR.

Calculates IRR per month.

What is the NPV if the discount rate is 10%

10.00

Enters I / YR

622.85

Calculates NPV.

Statistics—At a Glance…

CL

number +

number 2 -

number1 (INPUT) number2 +

number1 (INPUT) number2

X,y SWAP

Xw

,Sy SWAP

_x,O_y

y-valueX,SWAP

x-value ym

0.3m SWAP

Clear statistical registers.

Enter one-variable statistical data.

Delete one-variable statistical data.

Enter two-variable statistical data.

Delete two-variable statistical data.

Means of x and y .

Mean of x weighted by y .

Sample standard deviations of x and y .

Population standard deviations of x and y .

Estimate of x and correlation coefficient.

Estimate of y

y -intercept and slope.

Using the following data, find the means of x and y , the sample standard deviations of x and y , and the y -intercept and the slope of the linear regression forecast line. Then, use summation statistics to find n and xy .

| x-data | 2 | 4 | 6 |

| y-data | 50 | 90 | 160 |

| Keys: | Display: | Description: |

| CLX | 0.00 | Cleared statistics registers. |

| 2INPUT 50 Σ+ | 1.00 | Enters first x,y pair. |

| 4INPUT 90 Σ+ | 2.00 | Enters second x,y pair. |

| 6INPUT 160 Σ+ | 3.00 | Enters third x,y pair. |

| xy | 4.00 | Displays mean of x. |

| SWAP | 100.00 | Displays mean of y. |

| Sx,Sy | 2.00 | Displays sample standard deviation of x. |

| SWAP | 55.68 | Displays sample standard deviation of y. |

| 0 ym | -10.00 | Displays y-intercept of regression line (predicted y value for x=0). |

| SWAP | 27.50 | Displays slope of regression line. |

| 4 | 3.00 | Displays n, number of data points entered. |

| 9 | 1,420.00 | Displays Σxy, sum of the products of x- and y-values. |

Keyboard Map

- Time value of money (page 53)

- Separate two numbers (page 28)

- Percent (page 33)

- Constant (page 37)

- Store and recall (page 40)

- Change sign (page 24)

- Statistics key (page 27)

- Shift key (page 27)

- Clear display, cancel operation (page 25)

- Clear all memory (page 25)

- On (page 87)

-

Statistical functions (page 87)

-

n through xy : statistical summation registers (page 88)

- 3-key memory (page 39)

- Backspace (page 25)

- Accumulate statistical data (page 86)

- Cash flows (page 75)

- Business functions: margin, markup, cost, price (page 35)

- Interest conversion (page 72)

- Amortization (page 67)

- Annunciator lines (page 26)

Getting Started

Power On and Off

To turn on your HP 10BII, press ON. To turn the calculator off, press the orange shift key (O), then ON (also written OFF).

Since the calculator has continuous memory, turning it off does not affect the information you have stored. To conserve energy, the calculator turns itself off approximately

10 minutes after you stop using it. The calculator uses two lithium batteries. If you see the low-battery symbol (□) in the display, replace the batteries. Refer to appendix A for more information.

Adjusting the Display Contrast

To change the brightness of the display, hold down ON and then press + or - .

Simple Arithmetic Calculations

Arithmetic Operators. The following examples demonstrate using the arithmetic operators , , , and ÷ .

If you press more than one operator consecutively, for example , all are ignored except the last one.

If you make a typing mistake while entering a number, press + to erase the incorrect digits.

Keys:

Display:

Description:

②④·⑦①+

62473

87.18

Adds 24.71 and 62.47.

When a calculation has been completed (by pressing ), pressing a number key starts a new calculation.

19× 12· 68 = 240.92

Calculates 19 × 12.68 .

If you press an operator key after completing a calculation, the calculation is continued.

115 53 356.42

Completes calculation of 240.92 + 115.5 .

You can do chain calculations without using after each step.

6.9X5.35÷ 36.92

Pressing ± displays intermediate result (6.9× 5.35)

40.57

Completes calculation.

Chain calculations are interpreted in the order in which they are entered. Calculate 4 + 9 × 3 .

4+9X 13.00

Adds 4 + 9

③ 39.00

Multiplies 13 × 3 .

Negative Numbers. Enter the number and press +/- to change the sign. Calculate -75 ÷ 3 .

Keys: Display:

Description:

7⑤+/- -75

Changes the sign of 75.

+3-25.00

Calculates result.

Understanding the Display and Keyboard

Cursor

The cursor (_) is visible when you are entering a number.

Clearing the Calculator

When the cursor is on, erases the last digit you entered. Otherwise, clears the display and cancels the calculation.

While you are entering a number, pressing clears it to zero. Otherwise, clears the display of its current contents and cancels the current calculation.

Clearing Messages. When the HP 10BII is displaying an error message, or clears the message and restores the original contents of the display. See "Messages" on page 137 for a complete list of messages and meanings.

Clearing Memory

| Keys | Description |

| C ALL | Cleared all memory. Does not reset modes.* |

| CL∑ | Cleared statistical memory. |

| * Modes on your HP 10BII are number of payments per year (page 54), Begin and End (page 55), and the display formats (page 29). | |

To clear all memory and reset calculator modes, press and hold down ON, then press and hold down both N and FV. When you release all three, all memory is cleared. The All Clear message is displayed.

Annunciators

Annunciators are symbols in the display that indicate the status of the calculator.

| Annunciator | Status |

| SHIFT | The shift key (〇) has been pressed. When another key is pressed, the function labeled in orange on the key is executed. |

| STATS | The statistics key (〇) is active. When another key is pressed, the function labeled in mauve above the key is executed. |

| PEND | An operation is waiting for another operand. |

| BEGIN | Begin mode is active (page 55); that is, pay-ments are at the beginning of a period. |

| INPUT | The INPUT key has been pressed and a number stored. |

| Battery power is low (page 119). | |

| AMORT | The amortization annunciator is lit, together with one of the following four annunciators.: |

| BAL | The balance of an amortization is displayed (page 68). |

| INT | The interest of an amortization is displayed (page 69). |

| PRIN | The principal of an amortization is displayed (page 68). |

| PER | A range of periods for an amortization is used (page 68). |

| C-FLOW | The cash flow annunciator is lit, together with one of the following 2 annunciators: |

| CF | The cash flow number appears briefly, then the cash flow is shown. |

| N | The cash flow number appears briefly, then the number of times the cash flow is repeated is shown. |

| ERROR | The error annunciator is lit, together with one of the following four annunciators: |

| TVM | There is a TVM error (such as solving for P/YR). |

| Annunciator | Status (Continued) |

| FULL | More than 15 cash flows have been entered, or more than 5 unsolved brackets used. |

| STAT | Incorrect data used in a statistics calculation or, when ERROR is not lit, a statistical calculation has been performed. |

| FUNC | A math error has occurred (for example, division by zero). |

| STAT | A statistical calculation has been performed. |

Shift Key

Most of the HP 10BII keys have a second or "shifted" function printed in orange on the key. The orange shift key () is used to access these functions.

When you press , the shift annunciator (SHIFT) is displayed to indicate that the shifted functions are active. To turn the SHIFT annunciator off, press again.

For example, press followed by ^2 (also shown as ^2 ) to multiply a number in the display by itself.

Statistics Key

The statistics key (, colored mauve) is used to access summary statistics from the statistics memory registers.

When you press , the statistics annunciator (STATS) is displayed. This indicates that you can recall one of six summary statistics with the next keystroke (see page 88). To turn the STATS annunciator off, press again.

For example, press followed by to recall the sum of the x values entered.

INPUT Key

The key is used to separate two numbers when using two-number functions or two-variable statistics. The key can also be used to evaluate any pending arithmetic operations, in which case the result is the same as pressing .

SWAP Key

Pressing SWAP exchanges the following:

The last two numbers that you entered; for instance, to change the order of division or subtraction.

The results of functions that return two values.

The x - and y -values when using statistics.

Math Functions

One-Number Functions. Math functions involving one number use the number in the display.

Keys:

8925√x

③·⑤⑦+②·③

1/x

Display:

9.45

0.42

3.99

Description:

Calculates square root.

1/2.36 is calculated first.

Adds 3.57 and 1/2.36

Two-Number Functions. When a function requires two numbers, the numbers are entered like this: number1 (INPUT) number2 followed by the operation. Pressing (INPUT) evaluates the current expression and displays the INPUT annunciator. For example, the following keystrokes calculate the percent change between 17 and 29.

Keys:

Display:

17.00

Description:

Enters number1, displays the INPUT annunciator.

29_

70.59

Enters number2.

Calculates the percent change.

Display Format of Numbers

When you turn on the HP 10BII for the first time, numbers are displayed with two decimal places and a period as the decimal point. The display format controls how many digits appear in the display.

If the result of a calculation is a number containing more significant digits than can be displayed in the current display format, the number is rounded to fit the current display setting.

Regardless of the current display format, each number is stored internally as a signed, 12-digit number with a signed, three-digit exponent.

Specifying Displayed Decimal Places

To specify the number of displayed decimal places:

- Press DISP.

- Enter the number of digits (0 through 9) that you wish to appear after the decimal point.

| Keys: | Display: | Description: |

| ○ | 0.00 | Clears display. |

| ○DISP 3 | 0.000 | Displays three decimal places. |

| 456× | 5.727 | |

| 1256= | ||

| ○DISP 9 | 5.727360000 | Displays nine decimal places. |

| ○DISP 2 | 5.73 | Restores two decimal places and rounds number in display. |

When a number is too large or too small to be displayed in DISP format, it automatically displays in scientific notation.

Scientific Notation

Scientific notation is used to represent numbers that are too large or too small to fit in the display. For example, if you enter the number 10,000,000 × 10,000,000 , the result is 1.00E14, which means "one times ten to the fourteenth power" or "1.00 with the decimal point moved fourteen places to the right." You can enter this number by pressing 1 14. The E stands for "exponent of ten."

Exponents can also be negative for very small numbers. The number 0.000000000004 is displayed as 4.00E - 12 , which means "four times ten to the negative twelfth power" or "4.0 with the decimal point moved 12 places to the left." You can enter this number by pressing 4 + / - 12 .

Displaying the Full Precision of Numbers

To set your calculator to display numbers as precisely as possible, press DISP (trailing zeros are not displayed.) To temporarily view all 12 digits of the number in the display (regardless of the current display format setting), press DISP and hold. The number is displayed as long as you continue holding. The decimal point is not shown.

Start with two decimal places (DISP 2).

Keys:

①0÷7=

DISP

Display:

1.43

142857142857

Description:

Divides.

Displays all 12 digits.

Interchanging the Period and Comma

To switch between the period and comma (United States and International display) used as the decimal point and digit separator, press .

For example, one million can be displayed as 1,000,000.00 or 1.000.000.00.

Rounding Numbers

The calculator stores and calculates using 12-digit numbers. When 12 digit accuracy is not desirable, use RND to round the number to the displayed format before using it in a calculation. Rounding numbers is useful when you want the actual (dollars and cents) monthly payment.

| Keys: | Display: | Description: |

| 9·87654321 | 9.87654321_ | Enters a number with more than two non-zero decimal places. |

| DISP 2 | 9.88 | Displays two decimal places. |

| DISP = | 987654321000 | Displays all digits without the decimal while you press Ⓞ. |

| RND | 9.88 | Rounds to two decimal places (specified by pressing ☐DISP 2). |

| DISP = | 9880000000000 | Shows rounded, stored number. |

Messages

The HP 10BII displays messages about the status of the calculator or informs you that you have attempted an incorrect operation. To clear a message from the display, press or . See "Messages" on page 137 for a list of meanings.

Business Percentages

You can use the HP 10BII to calculate simple percent, percent change, cost, price, margin, and markup.

Percent Key

The % key has two functions: finding a percent and adding or subtracting a percent.

Finding a Percent

The % key divides a number by 100 unless it is preceded by an addition or subtraction sign.

Example. Find 25% of 200.

Keys:

200x

② ⑤ %

Display:

200.00

0.25

50.00

Description:

Enters 200.

Converts 25% to a decimal.

Multiplies 200 by 25% .

Adding or Subtracting a Percent

You can add or subtract a percent in one calculation.

Example. Decrease 200 by 25% .

| Keys: | Display: | Description: |

| 2000 | 200.00 | Enters 200. |

| 25% | 50.00 | Multiplies 200 by 0.25. |

| 3 | 150.00 | Subtracts 50 from 200. |

Example. You borrow (1,250 from a relative, and you agree to repay the loan in a year with (7 \%) simple interest. How much money will you owe?

| Keys: | Display: | Description: |

| 1250+7% | 87.50 | Calculates loan interest. |

| € | 1,337.50 | Adds $87.50 and $1,250.00 to show repayment amount. |

Percent Change

Calculate the percent change between two numbers ( n_1 and n_2 , expressed as a percent of n_1 ) by entering n_1 n_2 , then press % CHG .

Example. Calculate the percent change between 291.7 and 316.8.

| Keys: | Display: | Description: |

| 291 | 291.70 | Enters n1. |

| 3168 | 8.60 | Calculates percent change. |

Example. Calculate the percent change between (12 × 5) and (65 + 18) .

| Keys: | Display: | Description: |

| ①②×⑤INPUT | 60.00 | Calculates and enters n1. |

| ⑥⑤+①⑧-%CHG | 38.33 | Calculates percent change. |

Margin and Markup Calculations

The HP 10BII can calculate cost, selling price, margin, or markup.

| Application | Keys | Description |

| Margin | CST, PRC, MAR | Margin is markup expressed as a percent of price. |

| Markup | CST, PRC, MU | Markup calculations are expressed as a percent of cost. |

To see any value used by the Margin and Markup application, press RCL and then the key you wish to see. For example, to see the value stored as CST, press RCL CST. Margin and Markup share the same storage register. For example, if you store 20 in MAR, then press RCL MU, you will see 20.00 displayed.

Margin Calculations

Example. Kilowatt Electronics purchases televisions for 255. The televisions are sold for300. What is the margin?

| Keys: | Display: | Description: |

| ②⑤⑤④① | 255.00 | Stores cost in CST. |

| ③①①①① | 300.00 | Stores selling price in PRC. |

| MAR | 15.00 | Calculates margin. |

Markup on Cost Calculations

Example. The standard markup on costume jewelry at Kleiner's Kosmetique is 60% . They just received a shipment of chokers costing $19.00 each. What is the retail price per choker?

| Keys: | Display: | Description: |

| 19CST | 19.00 | Stores cost. |

| 60MU | 60.00 | Stores markup. |

| PRC | 30.40 | Calculates retail price. |

Using Margin and Markup Together

Example. A food cooperative buys cases of canned soup with an invoice cost of $9.60 per case. If the co-op routinely uses a 15% markup, for what price should it sell a case of soup? What is the margin?

| Keys: | Display: | Description: |

| 9 • 6 • CST | 9.60 | Stores invoice cost. |

| 1 • 5 • MU | 15.00 | Stores markup. |

| PRC | 11.04 | Calculates the price on a case of soup. |

| MAR | 13.04 | Calculates margin. |

Number Storage and Arithmetic

Using Stored Numbers in Calculations

You can store numbers, for reuse, in several different ways:

- Use (Constant) to store a number and its operator for repetitive operations.

Use 3 Key Memory () , () , and (+) to store, recall, and sum numbers with a single keystroke. - Use STO and RCL to store to, and recall from, the 10 numbered registers.

Using Constants

Use to store a number and arithmetic operator for repetitive calculations. Once the constant operation is stored, enter a number and press 三 . The stored operation is performed on the number in the display.

| Keys | Operation |

| ⊕ number⊕ = | Stores “+ number” as constant. |

| ⊕ number⊕ = | Stores “- number” as constant. |

| ⊕ number⊕ = | Stores “× number” as constant. |

| ⊕ number⊕ = | Stores “÷ number” as constant. |

| ⊕ value⊕ = | Stores “y value,” as constant. |

| ⊕ number⊕%⊕ = | Stores “+ number%” as constant. |

| ⊕ number⊕%⊕ = | Stores “- number%” as constant. |

| ⊕ number⊕%⊕ = | Stores “× number%” as constant. |

| ⊕ number⊕%⊕ = | Stores “÷ number%” as constant. |

Example. Calculate 5 + 2, 6 + 2 , and 7 + 2 .

| Keys: | Display: | Description: |

| ⑤⊕②K | 2.00 | Stores “+ 2” as constant. |

| Ξ | 7.00 | Adds 5 + 2. |

| ⑥Ξ | 8.00 | Adds 6 + 2. |

| ⑦Ξ | 9.00 | Adds 7 + 2. |

Example. Calculate 10 + 10% , 11 + 10% , and 25 + 10% .

| Keys: | Display: | Description: |

| 10+10%K | 1.00 | Stores “+ 10%” as constant. |

| = | 11.00 | Adds 10% to 10. |

| = | 12.10 | Adds 10% to 11. |

| 25= | 27.50 | Adds 10% to 25. |

Example. Calculate 2^3 and 4^3 .

| Keys: | Display: | Description: |

| 2 y 3 K | 3.00 | Stores “y3” as con-stant. |

| = | 8.00 | Calculates 23. |

Using the M Register

The -M , , and + keys perform memory operations on a single storage register, called the M register. In most cases, it is unnecessary to clear the M register, since -M replaces the previous contents. However, you can clear the M register by pressing -M . To add a series of numbers to the M register, use -M to store the first number and + to add subsequent numbers. To subtract

the displayed number from the number in the M register, press +/- followed by ^+ .

| Keys | Description |

| -M | Stores displayed number in the M register. |

| -RM | Recalls number from the M register. |

| -M+ | Adds displayed number to the M register. |

Example.Use the M register to add 17, 14.25, and 16.95. Then subtract 4.65 and recall the result.

| Keys: | Display: | Description: |

| 17M | 17.00 | Stores 17 in M register. |

| 1425M+ | 14.25 | Adds 14.25 to M register. |

| 1695M+ | 16.95 | Adds 16.95 to M register. |

| 465+/-M+ | -4.65 | Adds -4.65 to M register. |

| RM | 43.55 | Recalls contents of the M register. |

Using Numbered Registers

The and RCL keys access the 10 user registers. The key is used to copy the displayed number to a designated register. The RCL key is used to copy a number from a register to the display.

To store or recall a number in two steps:

- Press or RCL. (To cancel this step, press * or C.)

- Enter the register number (0 through 9).

In the following example, two storage registers are used. Calculate the following:

$$ \frac {4 7 5 . 6}{3 9 . 1 5} \text {a n d} \frac {5 6 0 . 1 + 4 7 5 . 6}{3 9 . 1 5} $$

| Keys: | Display: | Description: |

| 47560 | Stores 475.60 (dis- played number) in R1. | |

| 39.15 | Stores 39.15 in R2. | |

| 12.15 | Completes first calculation. | |

| 475.60 | Recalls R1. | |

| 39.15 | Recalls R2. | |

| 26.45 | Completes second calculation. |

With the exception of statistics, you can also use and RCL for application registers. For example, stores the number from the display in the I/YR register. RCL copies the contents from I/YR to the display.

In most cases, it is unnecessary to clear a storage register since storing a number replaces the previous contents. However, you can clear a single register by storing 0 in it. To clear all the registers at once, press C ALL.

Doing Arithmetic Inside Registers

You can do arithmetic inside storage registers R_0 through R_9 . The result is stored in the register.

| Keys | New Number in Register |

| □STO+register number | Old contents + displayed number. |

| □STO-register number | Old contents – displayed number. |

| □STO×register number | Old contents × displayed number. |

| □STO÷register number | Old contents ÷ displayed number. |

Example. Store 45.7 in R_3 , multiply by 2.5, and store the result in R_3 .

| Keys: | Display: | Description: |

| 45·7·STO 3 | 45.70 | Stores 45.7 in R3. |

| 2·5·STO × 3 | 2.50 | Multiplies 45.7 in R3 by 2.5 and stores result (114.25) in R3. |

| RCL 3 | 114.25 | Displays R3. |

Doing Arithmetic

Math functions operate on the number in the display.

Example. Calculate 14 , then calculate 20 + 47.2 + 1.1^2 .

| Keys: | Display: | Description: |

| 4 1/x | 0.25 | Calculates the reciprocal of 4. |

| 20 √x | 4.47 | Calculates √20. |

| +47 ∙2+ | 51.67 | Calculates √20 + 47.20. |

| 1 ∙1 x | 1.21 | Calculates 1.12. |

| - | 52.88 | Completes the calculation. |

Example. Calculate natural logarithm (e^2.5) . Then calculate 790 + 4!

| Keys: | Display: | Description: |

| 2·5·e | 12.18 | Calculates e2.5. |

| LN | 2.50 | Calculates natural logarithm of the result. |

| 790+4n! | 24.00 | Calculates 4 factorial. |

| = | 814.00 | Completes calculation. |

Power Operator

The power operator, raises the preceding number (y-value) to the power of the following number (x-value).

Example. Calculate 125^3 , then find the cube root of 125.

Keys:

Display:

1,953,125.00

5.00

Description:

Calculates 125^3

Calculates the cube root of 125, or 125^1 / 3

Using Parentheses in Calculations

Use parentheses to postpone calculating an intermediate result until you've entered more numbers. You can enter up to four open parentheses in each calculation. For example, suppose you want to calculate:

$$ \frac {3 0}{(8 5 - 1 2)} \times 9 $$

If you enter ③ 0 ÷ 8 5 - , the calculator displays the intermediate result, 0.35. This is because calculations without parentheses are performed from left to right as you enter them.

To delay the division until you've subtracted 12 from 85, use parentheses. Closing parentheses at the end of the expression can be omitted. For example, entering “ 25 ÷ (3 × (9 + 12) = ” is equivalent to “ 25 ÷ (3 × (9 + 12)) = ”.

| Keys: | Display: | Description: |

| ③0÷①85- | 85.00 | No calculation yet. |

| ①2-1 | 73.00 | Calculates 85 - 12. |

| × | 0.41 | Calculates 30 ÷ 73. |

| ⑨= | 3.70 | Multiplies the result by 9. |

Picturing Financial Problems

How to approach a Financial Problem

The financial vocabulary of the HP 10BII is simplified to apply to all financial fields. For example, your profession may use the term balance, balloon payment, residual, maturity value, or remaining amount to designate a value that the HP 10BII knows as (future value).

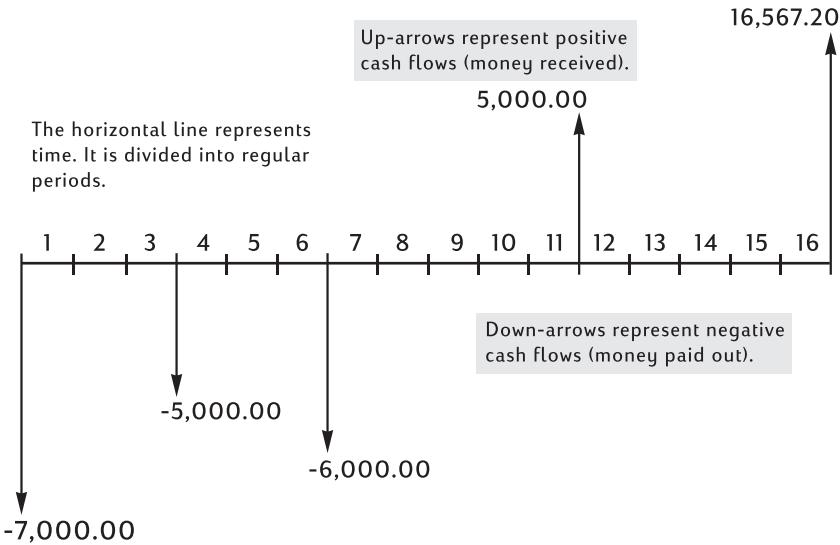

The simplified terminology of the HP 10BII is based on cash flow diagrams. Cash flow diagrams are pictures of financial problems that show cash flows over time. Drawing a cash flow diagram is the first step to solving a financial problem.

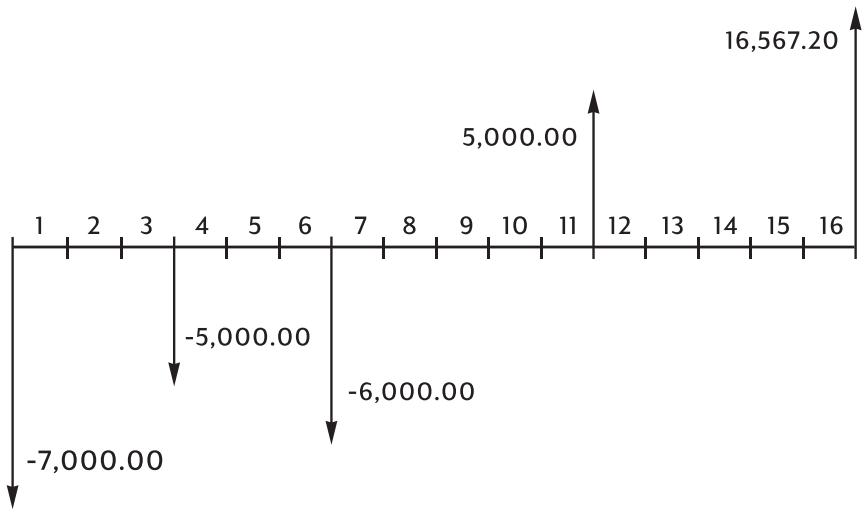

The following cash flow diagram represents investments in a mutual fund. The original investment was 7,000.00, followed by investments of 5,000.00 and 6,000.00 at the end of the third and sixth months. At the end of the 11th month,5,000.00 was withdrawn. At the end of the 16th month, $16,567.20 was withdrawn.

Any cash flow example can be represented by a cash flow diagram. As you draw a cash flow diagram, identify what is known and unknown about the transaction.

Time is represented by a horizontal line divided into regular time periods. Cash flows are placed on the horizontal line when they occur. Where no arrows are drawn, no cash flows occur.

Signs of Cash Flows

In cash flow diagrams, money invested is shown as negative and money withdrawn is shown as positive. Cash flowing out is negative, cash flowing in is positive.

For example, from the lender's perspective, cash flows to customers for loans are represented as negative. Likewise, when a lender receives money from customers, cash flows are represented as positive. In contrast, from the borrower's perspective, cash borrowed is positive while cash paid back is negative.

Periods and Cash Flows

In addition to the sign convention (cash flowing out is negative, cash flowing in is positive) on cash flow diagrams, there are several more considerations:

- The time line is divided into equal time intervals. The most common period is a month, but days, quarters, and annual periods are also common. The period is normally defined in a contract and must be known before you can begin calculating.

- To solve a financial problem with the HP 10BII, all cash flows must occur at either the beginning or end of a period.

If more than one cash flow occurs at the same place on the cash flow diagram, they are added together or netted. For example, a negative cash flow of -250.00 and a positive cash flow of750.00 occurring at the same time on the cash flow diagram are entered as a $500.00 cash flow (750 - 250 = 500).

A valid financial transaction must have at least one positive and one negative cash flow.

Simple and Compound Interest

Financial calculations are based on the fact that money earns interest over time. There are two types of interest: simple interest and compound interest. The basis for Time Value of Money and cash flow calculations is compound interest.

Simple Interest

In simple-interest contracts, interest is a percent of the original principal. The interest and principal are due at the end of the contract. For example, say you loan 500 to a friend for a year, and you want to be repaid with (10% simple interest. At the end of the year, your friend owes you )550.00 (50 is 10% of 500). Simple interest calculations are done using the 12 key on your HP 10BII. An example of a simple interest calculation is on page 98.

Compound Interest

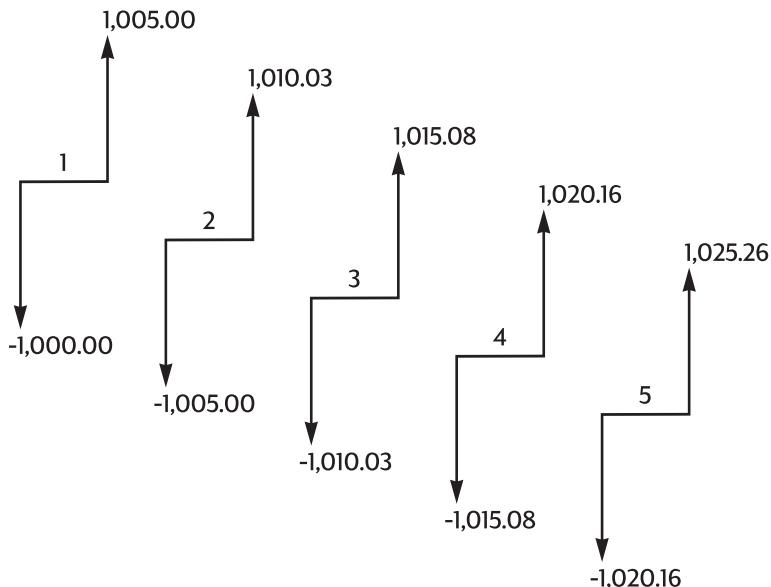

A compound-interest contract is like a series of simple-interest contracts that are connected. The length of each simple-interest contract is equal to one compounding period. At the end of each period the interest earned on each simple-interest contract is added to the principal. For example, if you deposit 1,000.00 in a savings account that pays (6% annual interest, compounded monthly, your earnings for the first month look like a simple-interest contract written for 1 month at 1/2% ( 6% ÷ 12 ). At the end of the first month the balance of the account is )1,005.00 (5 is 1/2% of 1,000).

The second month, the same process takes place on the new balance of 1,005.00. The amount of interest paid at the end of the second month is (1/2% of )1,005.00, or $5.03. The compounding process continues for the third, fourth, and fifth months. The intermediate results in this illustration are rounded to dollars and cents.

The word compound in compound interest comes from the idea that interest previously earned or owed is added to the principal. Thus, it can earn more interest. The financial calculation capabilities of the HP 10BII are based on compound interest.

Interest Rates

When you approach a financial problem, it is important to recognize that the interest rate or rate of return can be described in at least three different ways:

- As a periodic rate. This is the rate that is applied to your money from period to period.

- As an annual nominal rate. This is the periodic rate multiplied by the number of periods in a year.

- As an annual effective rate. This is an annual rate that considers compounding.

In the previous example of a 1,000.00 savings account, the periodic rate is 12% (per month), quoted as an annual nominal rate of 6% (12 × 12). This same periodic rate could be quoted as an annual effective rate, which considers compounding. The balance after 12 months of compounding is 1,061.68, which means the annual effective interest rate is 6.168%.

Examples of converting between nominal and annual effective rates are on pages 72 through 73.

Two Types of Financial Problems

The financial problems in this manual use compound interest unless specifically stated as simple interest calculations. Financial problems are divided into two groups: TVM problems and cash flow problems.

Recognizing a TVM Problem

If uniform cash flows occur between the first and last periods on the cash flow diagram, the financial problem is a TVM (time value of money) problem. There are five main keys used to solve a TVM problem.

N Number of periods or payments.

UYR Annual percentage interest rate (usually the annual nominal rate).

PV Present value (the cash flow at the beginning of the time line).

PMT Periodic payment.

FV Future value (the cash flow at the end of the cash flow diagram, in addition to any regular periodic payment).

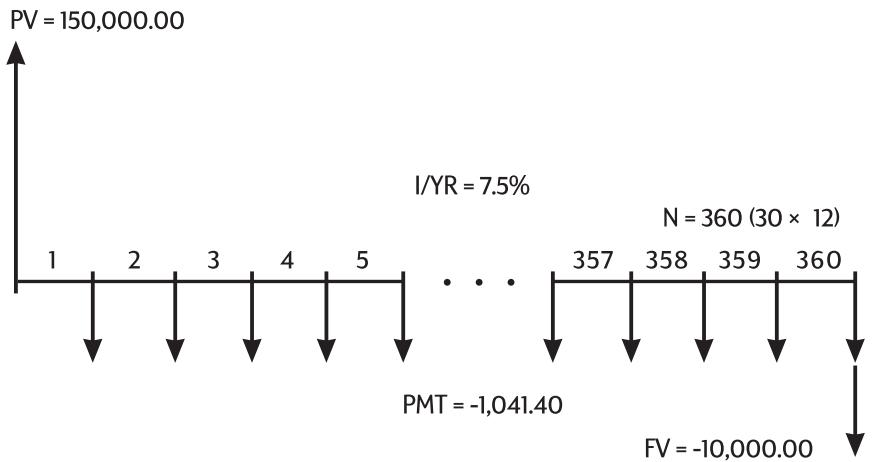

You can calculate any value after entering the other four. Cash flow diagrams for loans, mortgages, leases, savings accounts, or any contract with regular cash flows of the same amount are normally treated as TVM problems. For example, following is a cash flow diagram, from the borrower's perspective, for a 30-year, 150,000.00 mortgage, with a payment of 1,041.40, at 7.5% annual interest, with a $10,000 balloon payment.

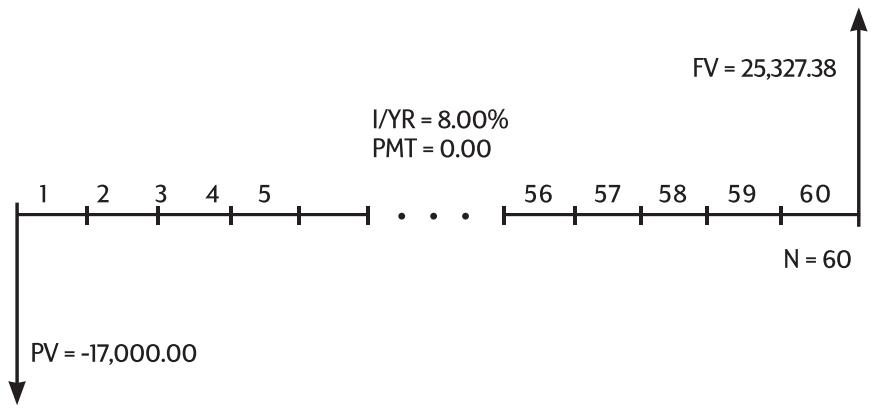

One of the values for PV , PMT , FV can be zero. For example, following is a cash flow diagram (from the saver's perspective) for a savings account with a single deposit and a single withdrawal five years later. Interest compounds monthly. In this example, PMT is zero.

Time value of money calculations are described in the next chapter.

Recognizing a Cash Flow Problem

A financial problem that does not have regular, uniform payments (sometimes called uneven cash flows) is a cash flow problem rather than a TVM problem.

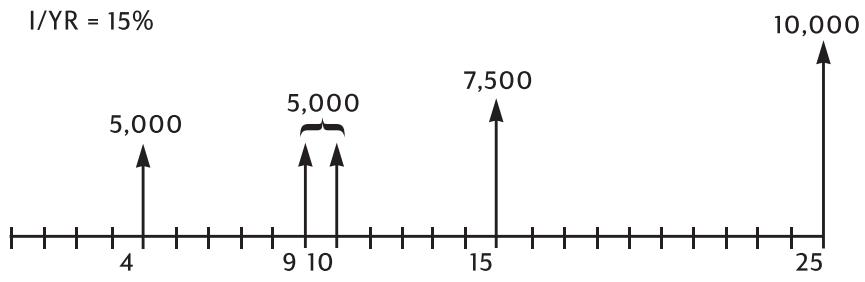

A cash flow diagram for an investment in a mutual fund follows. This is an example of a problem that is solved using either NPV (Net Present Value) or (RRY) (Internal Rate of Return per Year).

Cash flow problems are described in chapter 6.

Time Value of Money Calculations

Using the TVM Application

The time value of money (TVM) application is used for compound interest calculations that involve regular, uniform cash flows - called payments. Once the values are entered you can vary one value at a time, without entering all the values again.

To use TVM, several prerequisites must be met:

The amount of each payment must be the same. If the payment amounts vary, use the procedures described in chapter 6, "Cash Flow Calculations".

- Payments must occur at regular intervals.

The payment period must coincide with the interest compounding period. (If it does not, convert the interest rate using the NOM%, EFF%, and PYR keys described on page 72.)

There must be at least one positive and one negative cash flow.

| Key | Stores or Calculates |

| N | The number of payments or compounding periods. |

| I/YR | The annual nominal interest rate. |

| PV | The present value of future cash flows. PVis usually an initial investment or loan amount and always occurs at the beginning of the first period. |

| PMT | The amount of periodic payments. All payments are equal, and none are skipped; payments can occur at the beginning or end of each period. |

| FV | The future value. FVis either a final cash flow or compounded value of a series of previous cash flows. FVoccurs at the end of the last period. |

| PYR | Stores the number of periods per year. The default is 12. Reset only when you wish to change it. (This key is located below the PMTkey.) |

| K/P/YR | Optional shortcut for storing N: Number in display is multiplied by the value in P/YR and stores result in N. (This key is located below the Kkey.) |

| RES/END | Switches between Begin and End mode. In Begin mode, the BEGIN annunciator is displayed. |

| AMORT | Calculates an amortization table. |

To verify values, press RCL N, RCL I/YR, RCL PV, RCL PMT, and RCL FV. Pressing RCL P/YR recalls the total number of payments in years and RCL P/YR shows you the number of payments per year. Recalling these numbers does not change the content of the registers.

Clearing TVM

Press _ALL to clear the TVM registers. This sets N , I / YR , PV , PMT , and FV to zero and briefly displays the current value in P / YR .

Begin and End Modes

Before you start a TVM calculation, identify whether the first periodic payment occurs at the beginning or end of the first period. If the first payment occurs at the end of the first period, set your HP 10BII to End mode; if it occurs at the beginning of the first period, set your calculator to Begin mode.

To switch between modes, press BEGEND. The BEGIN annunciator is displayed when your calculator is in Begin mode. No annunciator is displayed when you are in End mode.

Mortgages and loans typically use End mode. Leases and savings plans typically use Begin mode.

Loan Calculations

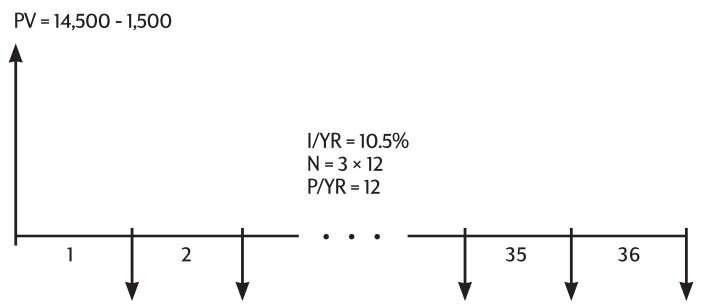

Example: A Car Loan. You are financing a new car with a three year loan at 10.5% annual nominal interest, compounded monthly. The price of the car is 14,500. Your down payment is1,500.

Part 1. What are your monthly payments at 10.5% interest? (Assume your payments start one month after the purchase or at the end of the first period.)

PMT = ? End Mode

Set to End mode. Press REGEN if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets periods per year. |

| 3×12N | 36.00 | Stores number of periods in loan. |

| 10·5/yr | 10.50 | Stores annual nominal interest rate. |

| 14500- | 13,000.00 | Stores amount borrowed. |

| 1500PV | ||

| 0FV | 0.00 | Stores the amount left to pay after 3 years. |

| PMT | -422.53 | Calculates the monthly payment. The negative sign indicates money paid out. |

Part 2. At a price of 14,500, what interest rate is necessary to lower your payment by 50.00, to $372.53?

| ⊕ 5 0 PMT | -372.53 | Decreases payment from $422.53. |

| I/YR | 2.03 | Calculates annual interest rate for the reduced payment. |

Part 3. If interest is 10.5 % , what is the maximum you can spend on the car to lower your car payment to $375.00?

| 10·5/yr | 10.50 | Stores original interest rate. |

| 37+/-PMT | -375.00 | Stores desired payment. |

| PV | 11,537.59 | Calculates amount of money to finance. |

| 100= | 13,037.59 | Adds the down pay-ment to the amount financed for total price of the car. |

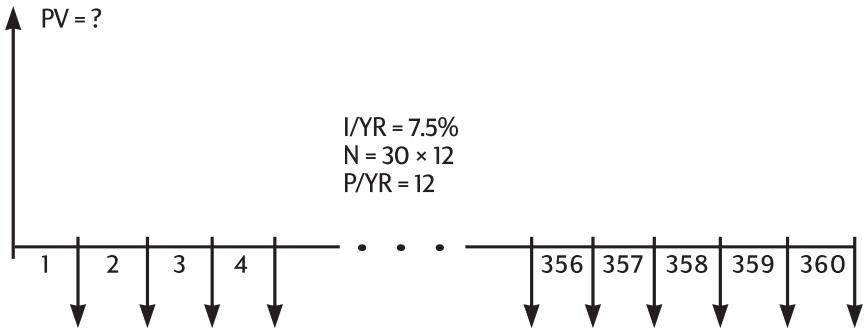

Example: A Home Mortgage. You decide that the maximum monthly mortgage payment you can afford is 930.00. You can make a12,000 down payment, and annual interest rates are currently 7.5%. If you obtain a 30 year mortgage, what is the maximum purchase price you can afford?

PMT = -930.00

End Mode

Set to End mode. Press BEGIND if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets periods per year. |

| 30xP/YR | 360.00 | Stores the length of the mortgage (30 × 12). |

| 0FV | 0.00 | Pays mortgage off in 30 years. |

| 75I/YR | 7.50 | Stores interest rate. |

| 930+/-PMT | -930.00 | Stores desired payment (money paid out is negative). |

| PV | 133,006.39 | Calculates the loan you can afford with a 930 payment. |

| +12000= | 145,006.39 | Adds12,000 down payment for the total purchase price. |

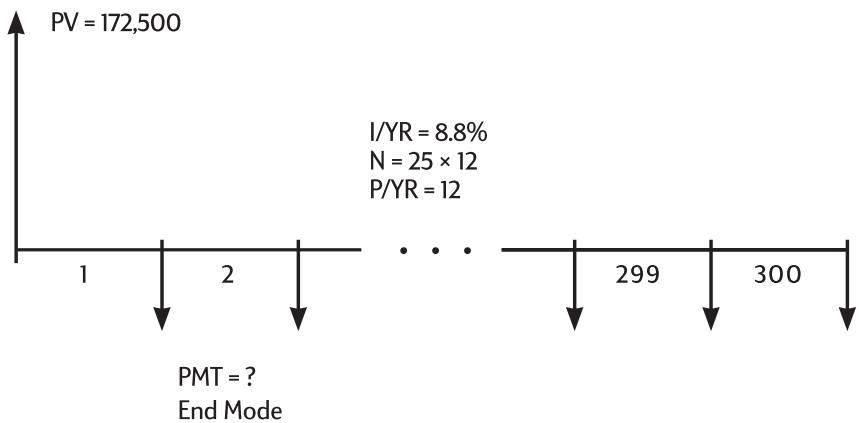

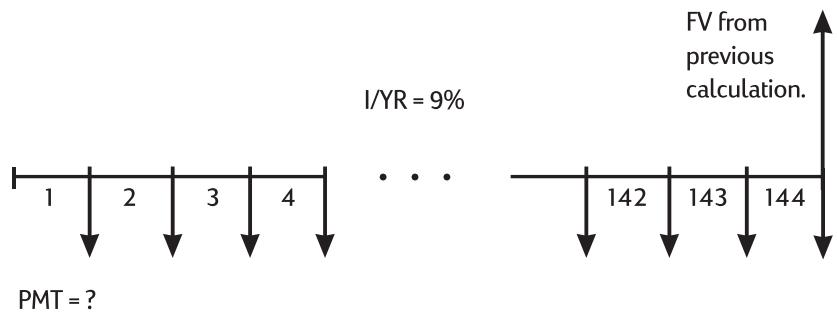

Example: A Mortgage With a Balloon Payment. You've obtained a 25 year, $172,500 mortgage at 8.8% annual interest. You anticipate that you will own the house for four years and then sell it, repaying the loan with a balloon payment. What will your balloon payment be?

Solve this problem using two steps:

- Calculate the loan payment using a 25 year term.

- Calculate the remaining balance after 4 years.

Step 1. First calculate the loan payment using a 25 year term.

Set to End mode. Press & BEGIN & BEGIN if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 12 | 12.00 | Sets periods per year. |

| 25 | 300.00 | Stores length of mortgage (25 × 12 = 300 months). |

| 0 | 0.00 | Stores loan balance after 25 years. |

| 17 | 172,500.00 | Stores original loan balance. |

| 8 | 8.80 | Stores annual interest rate. |

| PMT | -1,424.06 | Calculates monthly payment. |

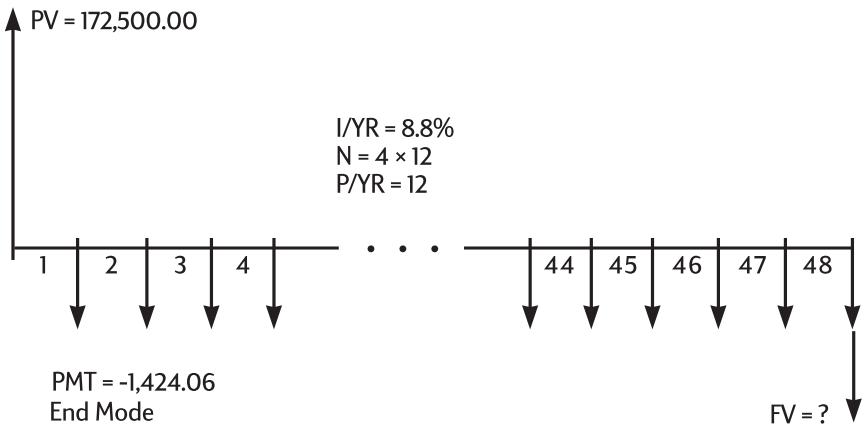

Step 2. Since the payment is at the end of the month, the past payment and the balloon payment occur at the same time. The final payment is the sum of PMT and FV .

The value in PMT should always be rounded to two decimal places when calculating FV or PV to avoid small, accumulative discrepancies between non-rounded numbers and actual (dollars and cents) payments. If the display is not set to two decimal places, press DISP 2.

Keys:

RND PMT

Display:

-1,424.06

Description:

Rounds payment to two decimal places, then stores.

48N

48.00

Stores 4 year term (12 × 4 ) that you expect to own house.

FV

-163,388.39

Calculates loan balance after 4 years.

+(RCL PMT)三

-164,812.45

Calculates total 48^th payment (PMT and FV ) to pay off loan (money paid out is negative).

Savings Calculations

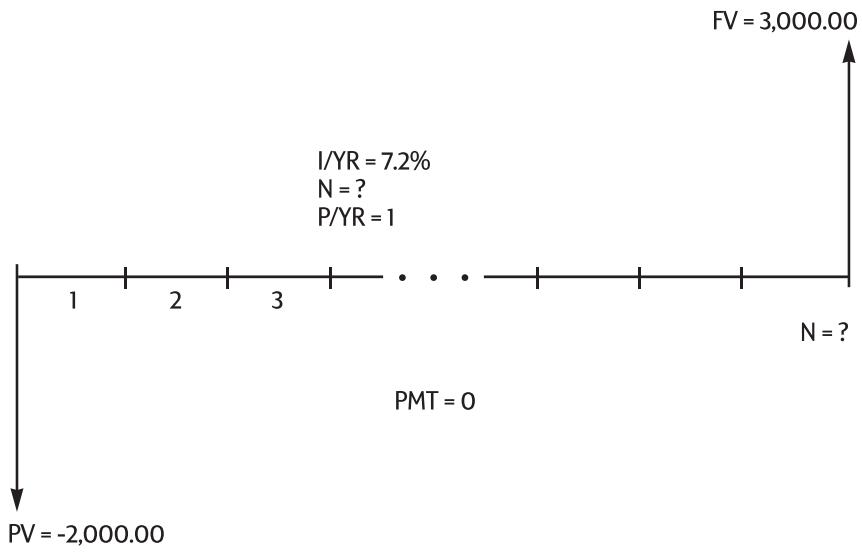

Example: A Savings Account. If you deposit 2,000 in a savings account that pays 7.2% annual interest compounded annually, and make no other deposits to the account, how long will it take for the account to grow to3,000?

Since this account has no regular payments (PMT = 0) , the payment mode (End or Begin) is irrelevant.

| Keys: | Display: | Description: |

| C ALL | 0.00 | Clears all registers. |

| 1 PYR | 1.00 | Sets P/YR to 1 since interest is compounded annually. |

| 2000+PV | -2,000.00 | Stores amount paid out for first deposit. |

| 3000FV | 3,000.00 | Stores the amount you wish to accumulate. |

| 72/1YR | 7.20 | Stores annual interest rate. |

| N | 5.83 | Calculates number of years it takes to reach $3,000. |

Since the calculated value of (N) is between 5 and 6, it will take six years of annual compounding to achieve a balance of at least \(3,000. Calculate the actual balance at the end of six years.

6N

6.00

Sets to 6 years.

FV

3,035.28

Calculates amount you can withdraw after 6 years.

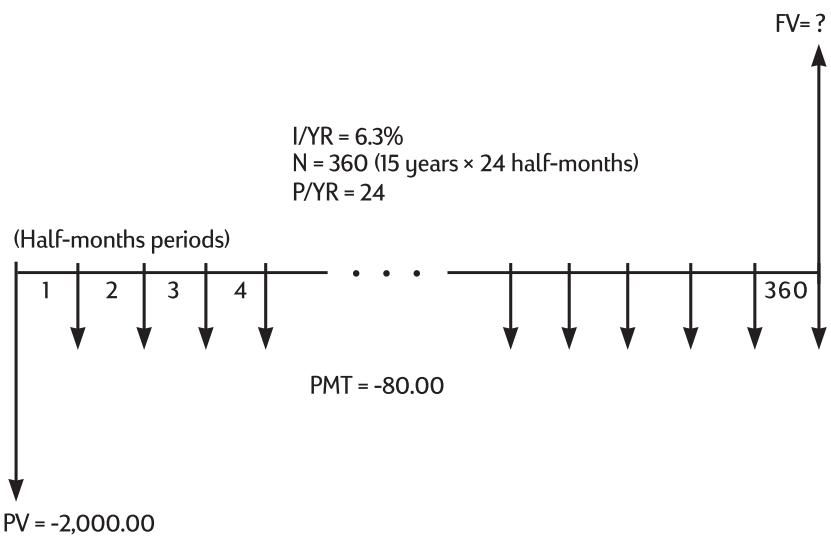

Example: An Individual Retirement Account. You opened an individual retirement account on April 14, 1995, with a deposit of 2,000.80.00 is deducted from your paycheck and you are paid twice a month. The account pays 6.3% annual interest compounded semimonthly. How much will be in the account on April 14, 2010?

Set to End mode. Press BEGUND if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 24PYR | 24.00 | Sets number of periods per year. |

| 200+PV | -2,000.00 | Stores initial deposit. |

| 8+PMT | -80.00 | Stores regular semimonthly deposits. |

| 63I/YR | 6.30 | Stores interest rate. |

| 15VP/YR | 360.00 | Stores number of deposits. |

| FV | 52,975.60 | Calculates balance. |

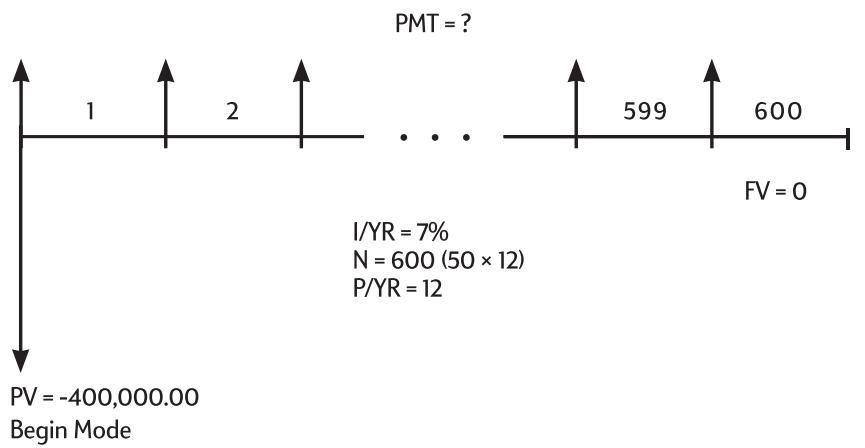

Example: An Annuity Account. You opt for an early retirement after a successful business career. You have accumulated a savings of $400,000 that earns an average of 7% annual interest, compounded monthly. What annuity (repetitive, uniform, withdrawal of funds) will you receive at the beginning of each month if you wish that savings account to support you for the next 50 years?

Set to Begin mode. Press REGEND if annunciator is not displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 400000+/- PV | -400,000.00 | Stores your nest egg as an outgoing deposit. |

| 7IYR | 7.00 | Stores annual interest rate you expect to earn. |

| 50+kPYR | 600.00 | Stores number of withdrawals. |

| 0FV | 0.00 | Stores balance of account after 50 years. |

| PMT | 2,392.80 | Calculates amount that you can withdraw at the beginning of each month. |

Lease Calculations

A lease is a loan of valuable property (like real estate, automobiles, or equipment) for a specific amount of time, in exchange for regular payments. Some leases are written as purchase agreements, with an option to buy at the end of the lease (sometimes for as little as $1.00). The defined future value (FV) of the property at the end of a lease is sometimes called the "residual value" or "buy out value."

All five TVM application keys can be used in lease calculations. There are two common lease calculations.

Finding the lease payment necessary to achieve a specified yield.

Finding the present value (capitalized value) of a lease.

The first payment on a lease usually occurs at the beginning of the first period. Thus, most lease calculations use Begin mode.

Example: Calculating a Lease Payment. A customer wishes to lease a 13,500 car for three years. The lease includes an option to buy the car for7,500 at the end of the lease. The first monthly payment is due the day the customer drives the car off the lot. If you want to yield 10% annually, compounded monthly, what will the payments be? Calculate the payments from your (the dealer's) point of view.

Set to Begin mode. Press if annunciator is not displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 10I/YR | 10.00 | Stores desired annual yield. |

| 13500+PV | -13,500.00 | Stores lease price. |

| 7500FV | 7,500.00 | Stores residual (buy out value). |

| 36N | 36.00 | Stores length of lease, in months. |

| PMT | 253.99 | Calculates monthly lease payment. |

Notice that even if the customer chooses not to buy the car, the lessor still includes a cash flow coming in at the end of the lease equal to the residual value of the car. Whether the customer buys the car or it is sold on the open market, the lessor expects to recover (7,500.

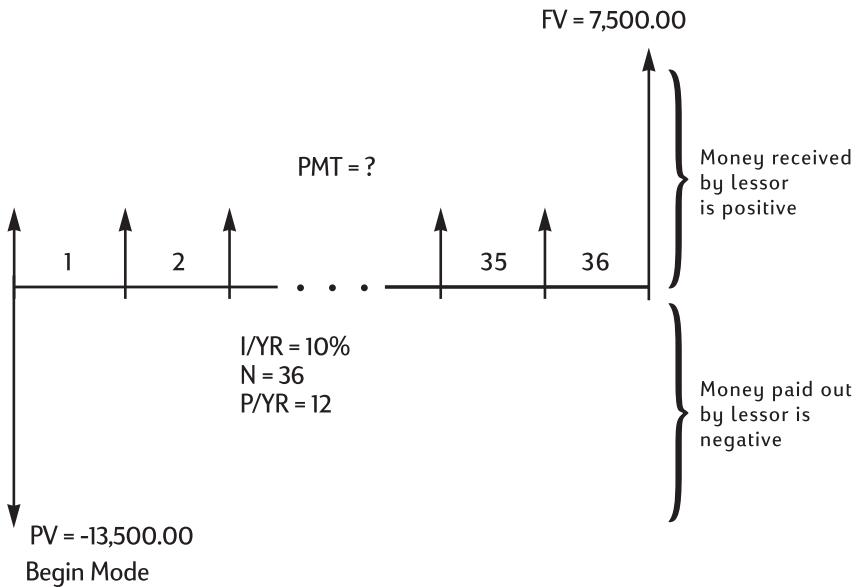

Example: Lease With Advance Payments. Your company, Quick-Kit Pole Barns, plans to lease a forklift for the warehouse. The lease is written for a term of 4 years with monthly payments of 2,400. Payments are due at the beginning of the month with the first and last payments due at the onset of the lease. You have an option to buy the forklift for15,000 at the end of the leasing period.

If the annual interest rate is 9% , what is the capitalized value of the lease?

This solution requires four steps.

- Calculate the present value of the 47 monthly payments: (4× 12) - 1 = 47

- Add the value of the additional advance payment.

- Find the present value of the buy option.

- Sum the values calculated in steps 2 and 3.

Step 1. Find the present value of the monthly payments.

Set to Begin mode. Press if annunciator is not displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 47N | 47.00 | Stores number of payments. |

| 2400+/-PMT | -2,400.00 | Stores monthly payment. |

| 0FV | 0.00 | Stores FV for step 1. |

| 9I/YR | 9.00 | Stores interest rate. |

| PV | 95,477.55 | Calculates present value of 47 monthly payments. |

Step 2. Add the additional advance payment to PV. Store the answer.

| ⊕RCL PMT +/− = | 97,877.55 | Adds additional advance payment. |

| -M | 97,877.55 | Stores result in M register. |

Step 3. Find the present value of the buy option.

| 48N | 48.00 | Stores month when buy option occurs. |

| 0 PMT | 0.00 | Stores zero payment for this step of solution. |

| 15000+/-FV | -15,000.00 | Stores value to discount. |

| PV | 10,479.21 | Calculates present value of last cash flow. |

Step 4. Add the results of steps 2 and 3.

| Keys: | Display: | Description: |

| ⊕RM= | 108,356.77 | Calculates present (capitalized) value of lease. (Rounding discrepancies are explained on page 59.) |

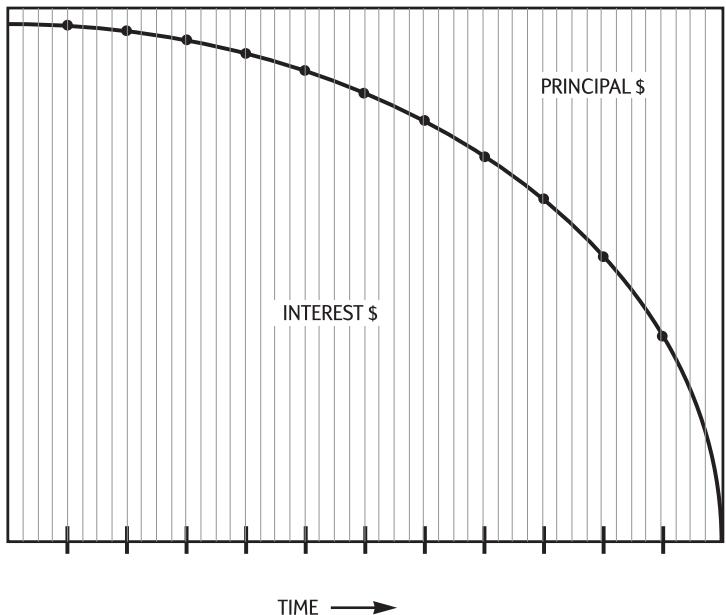

Amortization

Amortization is the process of dividing a payment into the amount that applies to interest and the amount that applies to principal. Payments near the beginning of a loan contribute more interest, and less principal, than payments near the end of a loan.

PAYMENT $

The AMORT key on the HP 10BII allows you to calculate.

The amount applied to interest in a range of payments.

The amount applied to principal in a range of payments.

The loan balance after a specified number of payments are made.

The AMORT function assumes you have just calculated a payment or you have stored the appropriate amortization values in I / YR , PV , FV , PMT , and P / YR .

Annual nominal interest rate.

Starting balance.

Ending balance.

Payment amount (rounded to the display format).

Number of payments per year.

The numbers displayed for interest, principal, and balance are rounded to the current display setting.

To Amortize. To amortize a single payment, enter the period number and press AMORT. The HP 10BII displays the annunciator PER followed by the starting and ending payments that will be amortized.

Press to see interest (INT). Press again to see the principal (PRIN) and again to see the balance (BAL). Continue pressing to cycle through the same values again.

To amortize a range of payments, enter starting period number (NPUT) ending period number; then press AMORT. The HP 10BII displays the annunciator PER followed by the starting and ending payments that will be amortized. Then press repeatedly to cycle through interest, principal, and balance.

Press AMORT again to move to the next set of periods. This autoincrement feature saves you the keystrokes of entering the new starting and ending periods.

If you store, recall, or perform any other calculations during amortization, pressing 三 will no longer cycle through interest, principal, and balance. To resume amortization with the same set of periods, press RCL AMORT.

Example: Amortizing a Range of Payments. Calculate the first two years of the annual amortization schedule for a 30 year, ( \( {180},{000} ) mortgage, at 7.75% annual interest with monthly payments.

Set to End mode. Press if BEGIN annunciator is displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 30xP/YR | 360.00 | Stores total number of payments. |

| 775 | 7.75 | Stores interest per year. |

| 180,000.00PV | 180,000.00 | Stores present value. |

| 0FV | 0.00 | Stores future value. |

| PMT | -1,289.54 | Calculates monthly payment. |

If you already know the mortgage payment, you can enter and store it just like you store the other four values. Next, amortize the first year.

| 1INPUT 12 | 12_ | Enters starting and ending periods. |

| AMORT | 1-12 | Displays the PER annunciator and range. |

| = | -1,579.82 | Displays the PRIN annunciator and the principal paid in the first year. |

| = | -13,894.66 | Displays the INT annunciator and the interest paid in the first year. |

| = | 178,420.18 | Displays the BAL annunciator and the loan balance after one year. |

The amount paid toward interest and principal (13,894.67 + 1,579.84 = 15,474.51) equals the total of 12 monthly payments (12 × 1,289.54 = 15,474.51) . The remaining balance equals the initial mortgage, less the amount applied toward principal (180,000 - 1,579.84 = 178,420.16) .

Amortize the second year:

| AMORT | 13-24 | Displays PER and the next range of periods. |

| € | -1,706.69 | Displays PRIN and the principal paid in the second year. |

| € | -13,767.79 | Displays INT and the interest paid in the second year. |

| € | 176,713.49 | Displays BAL and the loan balance after 24 payments. |

The amount paid toward interest and principal (13,767.79 + 1,706.69 = 15,474.51) equals the total of 12 monthly payments (12 × 1,289.54 = 15,474.51) . The remaining balance equals the initial mortgage less the amount applied toward principal (180,000 - 1,579.84 - 1,706.69 = 176,713.49) . More money is applied to principal during the second rather than the first year. The succeeding years continue in the same fashion.

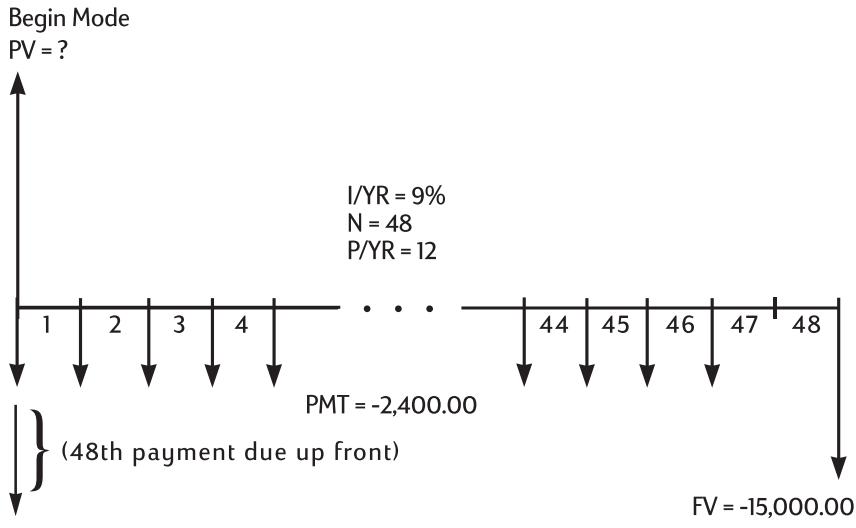

Example: Amortizing a Single Payment. Amortize the 1^st , 25^th , and 54^th payments of a five year car lease. The lease amount is $14,250 and the interest rate is 11.5%. Payments are monthly and begin immediately.

Set to Begin mode. Press if annunciator is not displayed.

| Keys: | Display: | Description: |

| 12PYR | 12.00 | Sets payments per year. |

| 5xP/YR | 60.00 | Stores number of payments. |

| 1150 | 11.50 | Stores interest per year. |

| 14,250.00 | 14,250.00 | Stores present value. |

| 0.00 | 0.00 | Stores the future value. |

| -310.42 | -310.42 | Calculates monthly payment. |

Amortize the 1^st , 25^th , and 54^th payments.

| 1INPUT | 1.00 | Enters first payment. |

| AMORT | 1-1 | Displays PER and the amortized payment period. |

| € | -310.42 | Displays PRIN and the first principal payment. |

| € | 0.00 | Displays INT and the interest. |

| € | 13,939.58 | Displays BAL and the loan balance after one payment. |

| 25INPUT | 25.00 | Enters payment to amortize. |

| AMORT | 25-25 | Displays PER and the amortized payment period. |

| € | -220.21 | Displays PRIN and the principal paid on the 25th payment. |

| € | -90.21 | Displays INT and the interest paid on the 25th payment. |

| € | 9,193.28 | Displays BAL and the balance after the 25th payment. |

| 54INPUT | 54.00 | Enters payment to amortize. |

| AMORT | 54-54 | Displays PER and the amortized payment period. |

| € | -290.37 | Displays PRIN and the principal paid on the 54th payment. |

| € | -20.05 | Displays INT and the interest paid on the 54th payment. |

| € | 1,801.57 | Displays BAL and the balance after the 54th payment. |

Interest Rate Conversions

The Interest Conversion application uses three keys:

NOM%, EFF%, and PYR. They convert between nominal and annual effective interest rates. Nominal and effective interest rates are described on page 49.

If you know an annual nominal interest rate and you wish to solve for the corresponding annual effective rate:

- Enter the nominal rate and press (NOM%)

- Enter the number of compounding periods and press

- Calculate the effective rate by pressing % .

To calculate a nominal rate from a known effective rate:

- Enter the effective rate and press % .

- Enter the number of compounding periods and press

- Calculate the nominal rate by pressing NOM%

In the TVM application, ^NOMPS and ^LYR share the same register.

Interest conversions are used primarily for two types of problems:

Comparing investments with different compounding periods.

- Solving TVM problems where the payment period and the interest period differ.

Investments With Different Compounding Periods

Example: Comparing Investments. You are considering opening a savings account in one of three banks. Which bank has the most favorable interest rate?

First Bank 6.70% annual interest, compounded quarterly.

Second Bank 6.65% annual interest, compounded monthly.

Third Bank 6.63% annual interest, compounded 360 times per year.

First Bank

| Keys: | Display: | Description: |

| 6·7·NOM% | 6.70 | Stores nominal rate. |

| 4·PYR | 4.00 | Stores quarterly compounding periods. |

| EFF% | 6.87 | Calculates annual effective rate. |

| Second Bank | ||

| 6·65·NOM% | 6.65 | Stores nominal rate. |

| 12·PYR | 12.00 | Stores monthly compounding periods. |

| EFF% | 6.86 | Calculates annual effective rate. |

| Third Bank | ||

| 6·63·NOM% | 6.63 | Stores nominal rate. |

| 360·PYR | 360.00 | Stores compounding periods. |

| EFF% | 6.85 | Calculates annual effective rate. |

First Bank offers a slightly better deal since 6.87 is greater than 6.86 and 6.85.

Compounding and Payment Periods Differ

The TVM application assumes that the compounding periods and the payment periods are the same. Some loan installments or savings deposits and withdrawals do not coincide with the bank's compounding periods. If the payment period differs from the compounding period, adjust the interest rate to match the payment period before solving the problem.

To adjust an interest rate when the compounding period differs from the payment period complete the following steps:

- Enter the nominal rate and press NOM%. Enter the number of compounding periods in a year and press FyR. Solve for the effective rate by pressing EFF%

- Enter the number of payment periods in a year and press FYR. Solve for the adjusted nominal rate by pressing NOM%.

Example: Monthly Payments, Daily Compounding. Starting today, you make monthly deposits of (25 to an account paying (5 \%)interest, compounded daily (using a 365 day year). What will the balance be in seven years?

Step 1. Calculate the equivalent rate with monthly compounding.

| Keys: | Display: | Description: |

| 5 NOM% | 5.00 | Stores nominal percentage rate. |

| 365PYR | 365.00 | Stores bank's compounding periods per year. |

| EFF% | 5.13 | Calculates annual effective rate. |

| 120PYR | 12.00 | Stores monthly periods. |

| NOM% | 5.01 | Calculates equivalent nominal percentage rate for monthly compounding. |

Since NOM% and I / YR share the same register, this value is ready for use in the rest of the problem.

Step 2. Calculate the future value.

Set to Begin mode. Press SEGEND if annunciator is not displayed.

| 0 PV | 0.00 | Stores present value. |

| 2 5 +/- PMT | -25.00 | Stores payment. |

| 7 P/yr | 84.00 | Stores total number of payments. |

| FV | 2,519.61 | Calculates balance after 7 years. |

Cash Flow Calculations

How to Use the Cash Flow Application

The cash flow application is used to solve problems where cash flows occur over regular intervals but are of varying amounts. You can also use cash flow calculations to solve problems with regular, equal, periodic cash flows, but these situations are handled more easily using TVM.

In general, these are the steps for cash flow calculations on the HP 10BII.

- Organize your cash flows on paper. A cash flow diagram is useful.

- Clear the registers.

- Enter the number of periods per year.

- Enter the amount of the initial investment.

- Enter the amount of the next cash flow.

- If the amount entered in step 5 occurs more than once consecutively, enter the number of times it occurs.

- Repeat steps 5 and 6 for each cash flow and group.

- To calculate net present value, enter the annual interest rate and press 1 / YR ; then press . Or, to calculate annual internal rate of return, press / YR .

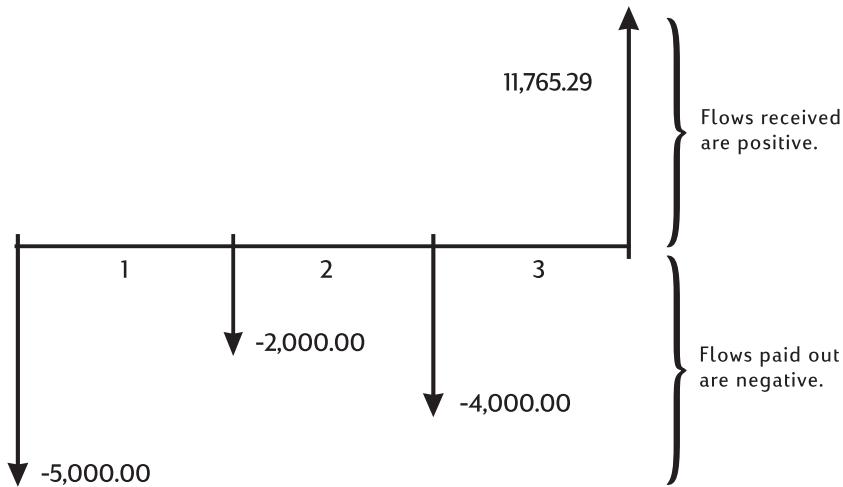

Example: A Short Term Investment. The following cash flow diagram represents an investment in stock over three months. Purchases were made at the beginning of each month, and the stock was sold at the end of the third month. Calculate the annual internal rate of return and the monthly rate of return.

Keys:

Display:

0.00

12.00

-5,000.00

Description:

Clears all registers.

Stores periods per year.

Enters initial cash flow. Displays cash flow group number while you hold down _j

Enters next cash flow.

Enters next cash flow.

Enters final cash flow.

Calculates annual nominal yield.

Monthly yield.

-2,000.00

-4,000.00

11,765.29

38.98

3.25

NPV and IRR/YR: Discontinuing Cash Flows

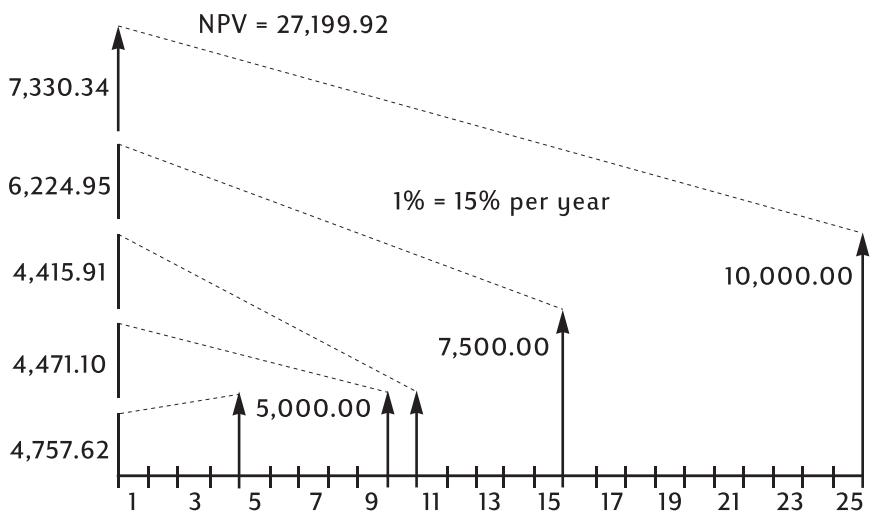

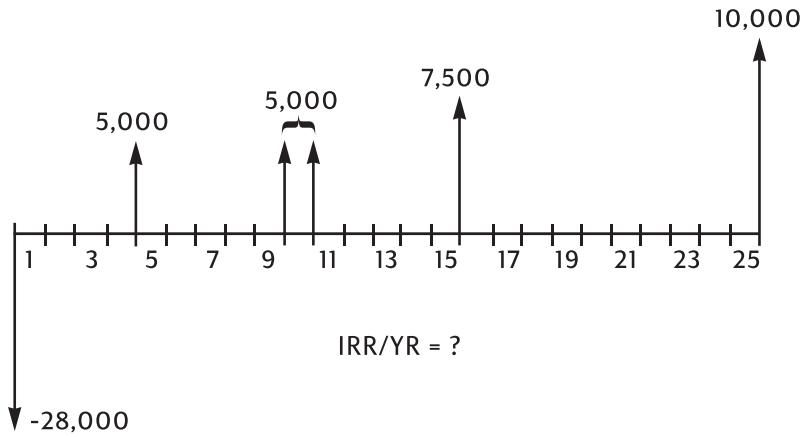

Chapter 4 demonstrates the use of cash flow diagrams to clarify financial problems. This section describes discounted cash flows. The NPV and IRR / YR functions are frequently referred to as discounted cash flow functions.

When a cash flow is discounted, you calculate its present value. When multiple cash flows are discounted, you calculate the present values and add them together.

The net present value (NPV) function finds the present value of a series of cash flows. The annual nominal interest rate must be known to calculate NPV.

The internal rate of return (IRR/YR) function calculates the annual nominal interest rate that is required to give a net present value of zero.

The utility of these two financial tools becomes clear after working a few examples. The next two sections describe organizing and entering your cash flows. Examples of NPV and IRR / YR calculations follow.

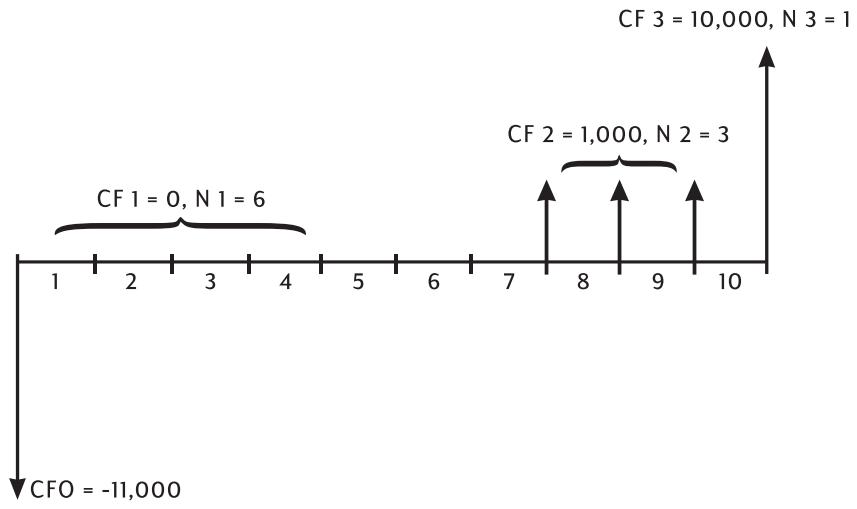

Organizing Cash Flows

The cash flow series is organized into an initial cash flow (CF 0) and succeeding cash flow groups (up to 14 cash flows). CF 0 occurs at the beginning of the first period. A cash flow group consists of a cash flow amount and the number of times it repeats.

For example, in the following cash flow diagram, the initial cash flow is -\ 11,000. The next group of cash flows consists of six flows of zero each, followed by a group of three \ 1,000 cash flows. The final group consists of one \$10,000 cash flow.

Whenever you enter a series of cash flows, it is important to account for every period on the cash flow diagram, even periods with cash flows of zero.

Entering Cash Flows

The HP 10BII can store an initial cash flow plus 14 additional cash flow groups. Each cash flow group can have up to 99 cash flows. Enter cash flows using the following steps:

- Press to clear the resisters.

- Enter the number of periods per year and press FYR

- Enter the amount of the initial investment, then press CF. (The "j" stands for the cash flow "number," 0 through 14.)

- Enter the amount of the next cash flow and press CF

- If the amount entered in step 4 occurs more than once consecutively, enter the number of times it occurs, and press .

- Repeat steps 4 and 5 for each CF_j and N_j until all cash flows have been entered.

Example. Enter the cash flows from the preceding diagram and calculate the IRR / YR . Then calculate the effective interest rate. Assume there are 12 periods per year.

| Keys: | Display: | Description: |

| C ALL | 0.00 | Clears all registers. |

| 12 PYR | 12.00 | Sets PYR to 12. |

| 11000+CFi | -11,000.00 | Enters initial cash flow. Displays cash flow group number for as long as you hold down CFi. |

| 0 CFi | 0.00 | Enters first cash flow group amount. |

| 6 Nj | 6.00 | Enters number of repetitions. |

| 10000CFi | 1,000.00 | Enters second cash flow group amount. |

| 3 Nj | 3.00 | Enters number of repetitions. |

| 100000CFi | 10,000.00 | Enters final cash flow. |

| RRYR | 21.22 | Calculates annual nominal yield. |

Viewing and Replacing Cash Flows

To view a cash flow, press:

RCL CF to 9 to display cash flows 0 to 9, or

RCL CF to 4 to display cash flows 10 to 14

RCL CF_j+ to display the next cash flow

RCL CF to display the previous cash flow

RCL CF to display the current cash flow.

To replace a cash flow amount, press:

STO CF to 9 to store the new amount in cash flows 0 to 9

STO CF to 4 to store the new amount in cash flows 10 to 14

- (_) + to store the amount in the next cash flow

- (CF) to store the amount in the previous cash flow

STO CF_j CFj to store the amount in the current cash flow.

To replace the number of times a particular cash flow occurs, the cash flow whose number of occurrences will change. Then enter the number of times it occurs and press .

Since cash flows cannot be deleted or inserted, use to start over.

Calculating Net Present Value

The net present value (NPV) function is used to discount all cash flows to the front of the time line using an annual nominal interest rate that you supply.

These steps describe how to calculate NPV:

- Press C ALL and store the number of periods per year in P / YR .