17BII - Calculatrice HP - Notice d'utilisation et mode d'emploi gratuit

Retrouvez gratuitement la notice de l'appareil 17BII HP au format PDF.

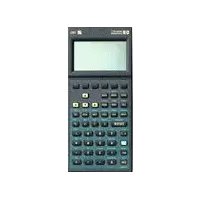

| Type de produit | Calculatrice financière programmable |

| Marque et modèle | HP 17BII |

| Alimentation | 2 piles CR2032 (3V) |

| Affichage | 2 lignes, 12 caractères alphanumériques, menus et messages |

| Mémoire | 6,5 Ko (environ 6 750 octets) pour données, listes et équations |

| Fonctions principales | Valeur temps de l'argent (TVM), flux de trésorerie (CFLO), obligations, amortissement, dépréciation, intérêts composés, pourcentages, statistiques, date et rendez-vous, solveur d'équations |

| Modes de calcul | Algébrique (ALG) ou Notation Polonaise Inverse (RPN) |

| Impression | Compatible avec l'imprimante infrarouge HP 82240 (optionnelle) |

| Dimensions (approx.) | 15 × 8 × 1,5 cm |

| Poids (approx.) | 120 g (sans piles) |

| Entretien et nettoyage | Chiffon doux sec ; ne pas utiliser de produits abrasifs |

| Sécurité | Mise hors tension automatique après 10 minutes d'inactivité |

| Pièces détachées et réparabilité | Piles remplaçables par l'utilisateur ; service après-vente HP |

| Informations générales | Manuel d'utilisation de 296 pages ; langues multiples |

FOIRE AUX QUESTIONS - 17BII HP

Questions des utilisateurs sur 17BII HP

0 question sur cet appareil. Repondez a celles que vous connaissez ou posez la votre.

Poser une nouvelle question sur cet appareil

Téléchargez la notice de votre Calculatrice au format PDF gratuitement ! Retrouvez votre notice 17BII - HP et reprennez votre appareil électronique en main. Sur cette page sont publiés tous les documents nécessaires à l'utilisation de votre appareil 17BII de la marque HP.

MODE D'EMPLOI 17BII HP

HP 17BII

Financial Calculator

Owner's Manual

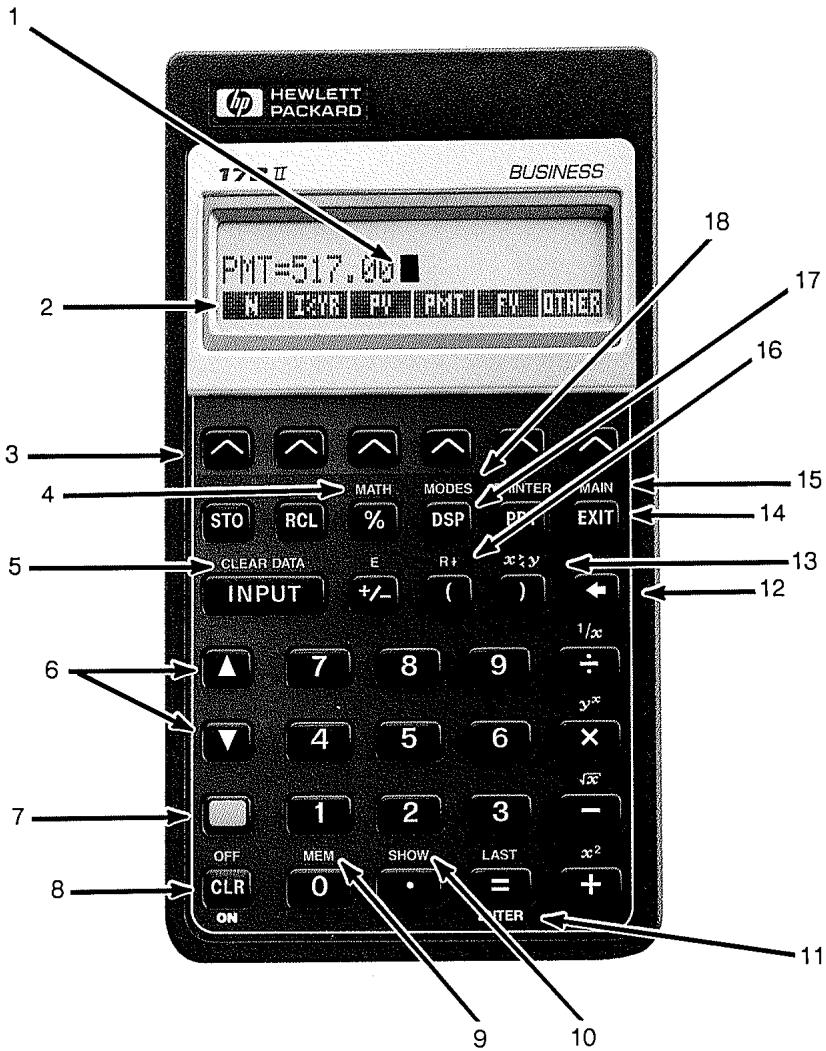

- Cursor

- Menu labels

- Menu keys

- More math

- Clearing stored data

- Moving through lists

- Shift key (for colored functions)

- On or display clear

-

User memory available

-

All decimal places

- [ENTER] (RPN mode)

- Backspace

- Exchange RPN registers

- Previous menu

- Main menu

- Roll down RPN stack

- Display formats

- Modes key

HP-17B II Business Calculator

Owner's Manual

Notice

For warranty and regulatory information for this calculator, see the owner's manual.

This manual and any examples contained herein are provided "as is" and are subject to change without notice. Hewlett-Packard Company makes no warranty of any kind with regard to this manual, including, but not limited to, the implied warranties of merchantability and fitness for a particular purpose. Hewlett-Packard Co. shall not be liable for any errors or for incidental or consequential damages in connection with the furnishing, performance, or use of this manual or the examples contained herein.

irc Hewlett-Packard Co. 1989. All rights reserved. Reproduction, adaptation, or translation of this manual is prohibited without prior written permission of Hewlett-Packard Company, except as allowed under the copyright laws.

The programs that control your calculator are copyrighted and all rights are reserved. Reproduction, adaptation, or translation of those programs without prior written permission of Hewlett-Packard Co. is also prohibited.

Corvallis Division

1000 N.E. Circle Blvd.

Corvallis, OR 97330, U.S.A.

Printing History

Edition 1

Edition 2

Edition 3

December 1989

April 1991

November 1994

9

110

Running Total and Statistics

111

The SUM Menu

112

Creating a SUM List

112

Entering Numbers and Viewing the TOTAL

113

Viewing and Correcting the List

115

Copying a Number from a List to the Calculator Line

115

Naming and Renaming a SUM List

116

Starting or GETting Another List

116

Clearing a SUM List and Its Name

116

Doing Statistical Calculations (CALC)

117

Calculations with One Variable

119

Calculations with Two Variables (FRCST)

122

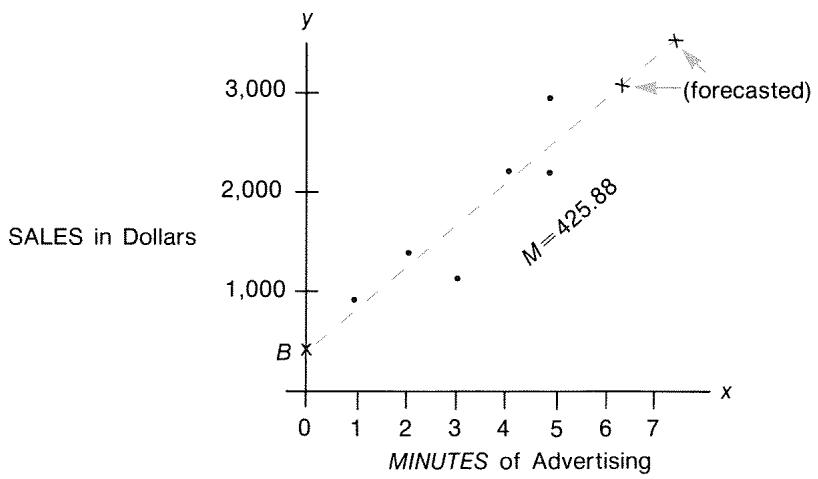

Curve Fitting and Forecasting

126

Weighted Mean and Grouped Standard Deviation

129

129

Summation Statistics

129

Doing Other Calculations with SUM Data

10

130

Time, Appointments, and Date Arithmetic

130

Viewing the Time and Date

131

The Time Menu

132

Setting the Time and Date (SET)

133

Changing the Time and Date Formats (SET)

133

Adjusting the Clock Setting (ADJST)

133

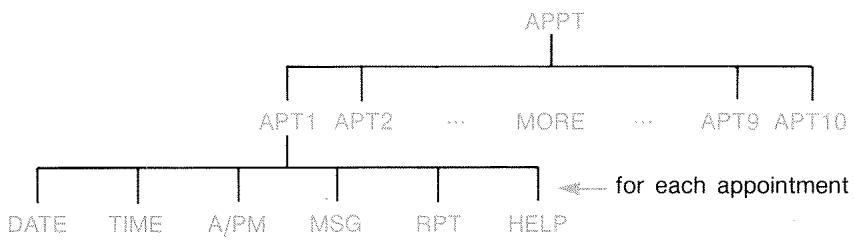

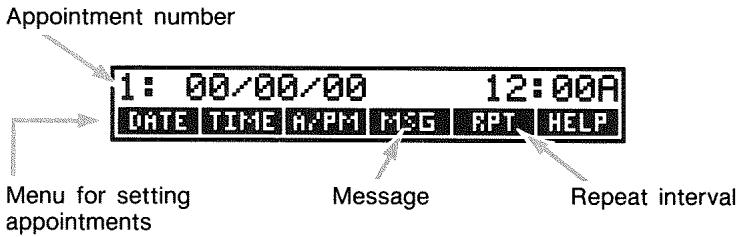

Appointments (APPT)

134

Viewing or Setting an Appointment (APT1-APT10)

136

Acknowledging an Appointment

136

Unacknowledged Appointments

137

Clearing Appointments

138

Date Arithmetic (CALC)

139

Determining the Day of the Week for Any Date

139

Calculating the Number of Days between Dates

140

Calculating Past or Future Dates

11 141 The Equation Solver

141 An Example Using the Solver: Sales Forecasts

144 The SOLVE Menu

145 Entering Equations

146 Calculating Using Solver Menus (CALC)

149 Editing an Equation (EDIT)

149 Naming an Equation

150 Finding an Equation in the Solver List

150 Shared Variables

151 Clearing Variables

151 Deleting Variables and Equations

152 Deleting One Equation or Its Variables (DELET)

152 Deleting All Equations or All Variables in the Solver (CLEAR DATA)

153 Writing Equations

154 What Can Appear in an Equation

157 Solver Functions

161 Conditional Expressions with IF

163 The Summation Function ()

164 Accessing CFLO and SUM Lists from the Solver

165 Creating Menus for Multiple Equations (S Function)

166 How the Solver Works

168 Halting and Restarting the Numerical Search

168 Entering Guesses

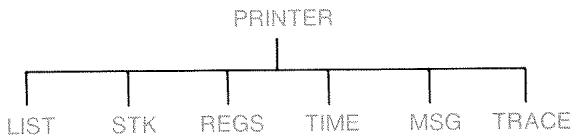

12 171 Printing

172 The Printer's Power Source

172 Double-Space Printing

172 Printing the Display (PRT)

173 Printing Other Information (PRINTER)

174 Printing Variables, Lists, and Appointments (LIST)

175 Printing Descriptive Messages (MSG)

176 Trace Printing (TRACE)

177 How to Interrupt the Printer

| 13 | 178 | Additional Examples |

| 178 | Loans | |

| 178 | Simple Annual Interest | |

| 179 | Yield of a Discounted (or Premium) Mortgage | |

| 181 | Annual Percentage Rate for a Loan with Fees | |

| 183 | Loan with an Odd (Partial) First Period | |

| 185 | Canadian Mortgages | |

| 187 | Advance Payments (Leasing) | |

| 189 | Savings | |

| 189 | Value of a Fund with Regular Withdrawals | |

| 191 | Deposits Needed for a Child's College Account | |

| 195 | Value of a Tax-Free Account | |

| 197 | Value of a Taxable Retirement Account | |

| 198 | Modified Internal Rate of Return | |

| 201 | Price of an Insurance Policy | |

| 203 | Bonds | |

| 205 | Discounted Notes | |

| 206 | Statistics | |

| 206 | Moving Average | |

| 208 | Chi-Squared (x²) Statistics |

| A | 211 | Assistance, Batteries, Memory, and Service |

| 211 | Obtaining Help in Operating the Calculator | |

| 211 | Answers to Common Questions | |

| 213 | Power and Batteries | |

| 214 | Low-Power Indications | |

| 214 | Installing Batteries | |

| 216 | Managing Calculator Memory | |

| 217 | Resetting the Calculator | |

| 218 | Erasing Continuous Memory | |

| 218 | Clock Accuracy | |

| 219 | Environmental Limits | |

| 219 | Determining If the Calculator Requires Service | |

| 220 | Confirming Calculator Operation: Self-Test |

Limited One-Year Warranty

What is Covered

What Is Not Covered

Consumer Transactions in the United Kingdom

If the Calculator Requires Service

Obtaining Service

Service Charge

Shipping Instructions

Warranty on Service

Service Agreements

Regulatory Information

Radio Frequency Interference

Air Safety Notice (U.S.A.)

More About Calculations

IRR% Calculations

Possible Outcomes of Calculating IRR%

Halting and Restarting the IRR% Calculation

Storing a Guess for IRR%

Dolver Calculations

Direct Solutions

Iterative Solutions

Equations Used by Built-in Menus

Actuarial Functions

Percentage Calculations in Business (BUS)

Time Value of Money (TVM)

Amortization

Interest Rate Conversions

Cash-Flow Calculations

Bond Calculations

Depreciation Calculations

Sum and Statistics

Forecasting

Equations Used in (Chapter 13)

Canadian Mortgages

Odd-Period Calculations

Advance Payments

Modified Internal Rate of Return

Welcome to the HP-17B II

The HP-17B is part of Hewlett-Packard's new generation of calculators:

The two-line display has space for messages, prompts, and labels.

- Menu and messages show you options and guide you through problems.

Built-in applications solve these business and financial tasks:

Time Value of Money. For loans, savings, leasing, and amortization.

■ Interest Conversions. Between nominal and effective rates.

Cash Flows. Discounted cash flows for calculating net present value and internal rate of return.

Bonds. Price or yield on any date. Annual or semi-annual coupons; 30/360 or actual/actual calendar.

Depreciation. Using methods of straight line, declining balance, sum-of-the-years' digits, and accelerated cost recovery system.

Business Percentages. Percent change, percent total, markup.

Statistics. Mean, correlation coefficient, linear estimates, and other statistical calculations.

Clock. Time, date, and appointments.

Use the Solver for problems that aren't built in: type an equation and then solve for any unknown value. It's easier than programming!

There are 6.5K bytes of memory to store data, lists, and equations.

You can print information using the HP 82240 Infrared Printer.

■ You can choose either ALG (Algebraic) or RPN (Reverse Polish Notation) entry logic for your calculations.

Contents

12 List of Examples

15 Important Information

1 16 Getting Started

16 Power On and Off; Continuous Memory

16 Adjusting the Display Contrast

17 What You See in the Display

17 The Shift Key (■)

18 Backspacing and Clearing

19 Doing Arithmetic

20 Keying in Negative Numbers (+ - )

20 Using the Menu Keys

21 The MAIN Menu

22 Choosing Menus and Reading Menu Maps

23 Calculations Using Menus

25 Exiting Menus ( XIT)

25 Clearing Values in Menus

26 Solving Your Own Equations (SOLVE)

27 Typing Words and Characters: the ALPHAbetic Menu

28 Editing ALPHAbetic Text

29 Calculating the Answer (CALC)

30 Controlling the Display Format

31 Decimal Places

31 Internal Precision

31 Temporarily SHOWing ALL

31 Rounding a Number

32 Exchanging Periods and Commas in Numbers

33 Error Messages

33 Modes

34 Calculator Memory ( MEMI)

2

35 Arithmetic

35 The Calculator Line

35 Doing Calculations

36 Using Parentheses in Calculations

37 The Percent Key

38 The Mathematical Operations

38 The Power Function (Exponentiation)

39 The MATH Menu

40 Saving and Reusing Numbers

40 The History Stack of Numbers

41 Reusing the Last Result (LAST)

42 Storing and Recalling Numbers

43 Doing Arithmetic Inside Registers and Variables

44 Scientific Notation

44 Range of Numbers

3

45 Percentage Calculations in Business

46 Using the BUS Menus

46 Examples Using the BUS Menus

46 Percent Change (%CHG)

47 Percent of Total (%TOTL)

47 Markup as a Percent of Cost (MU%C)

48 Markup as a Percent of Price (MU%P)

48 Sharing Variables Between Menus

4

50 Time Value of Money

50 The TVM Menu

53 Cash Flow Diagrams and Signs of Numbers

55 Using the TVM Menu

56 Loan Calculations

60 Savings Calculations

63 Leasing Calculations

67 Amortization (AMRT)

68 Displaying an Amortization Table

71 Printing an Amortization Table

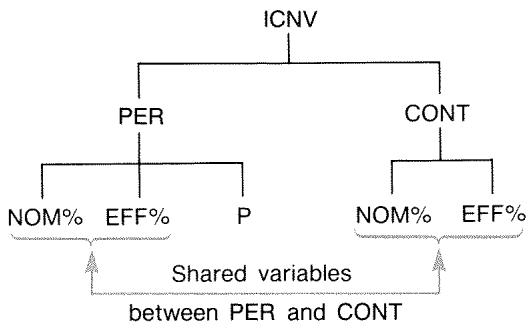

| 5 | 73 | Interest Rate Conversions |

| 74 | The ICNV Menu | |

| 74 | Converting Interest Rates | |

| 77 | Compounding Periods Different from Payment Periods. | |

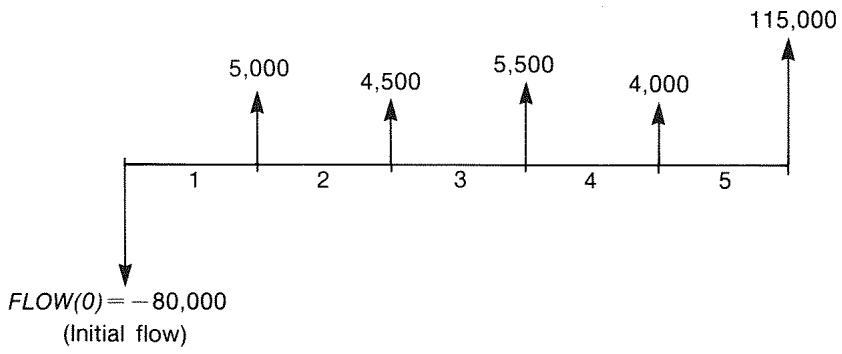

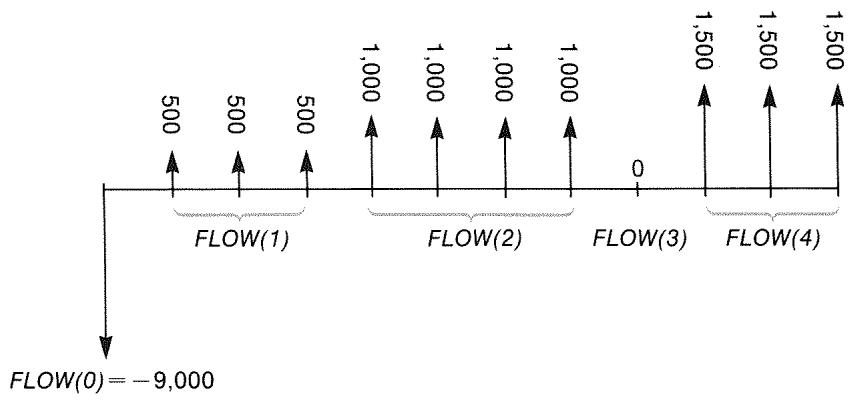

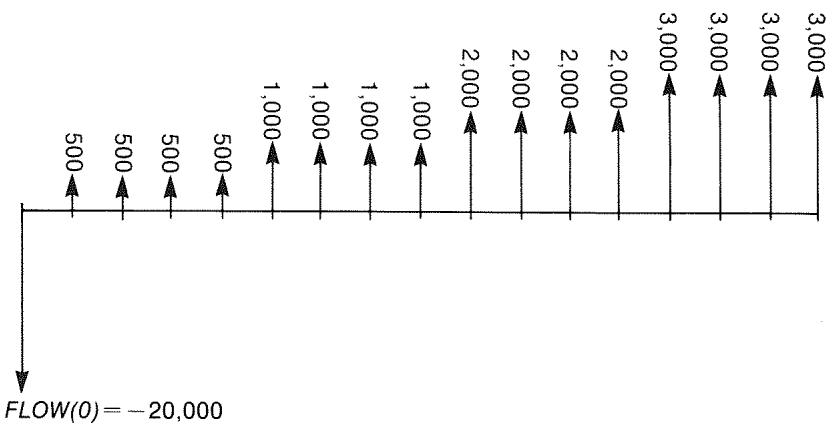

| 6 | 80 | Cash Flow Calculations |

| 81 | The CFLO Menu | |

| 82 | Cash Flow Diagrams and Signs of Numbers | |

| 83 | Creating a Cash-Flow List | |

| 84 | Entering Cash Flows | |

| 87 | Viewing and Correcting the List | |

| 87 | Copying a Number from a List to the Calculator Line | |

| 87 | Naming and Renaming a Cash-Flow List | |

| 88 | Starting or GETting Another List | |

| 89 | Clearing a Cash-Flow List and Its Name | |

| 89 | Cash-Flow Calculations: IRR, NPV, NUS, NFV | |

| 96 | Doing Other Calculations with CFLO Data |

| 7 | 97 | Bonds |

| 97 | The BOND Menu | |

| 98 | Doing Bond Calculations |

| 8 | 103 | Depreciation |

| 103 | The DEPRC Menu | |

| 105 | Doing Depreciation Calculations | |

| 105 | DB, SOYD, and SL Methods | |

| 107 | The ACRS Method | |

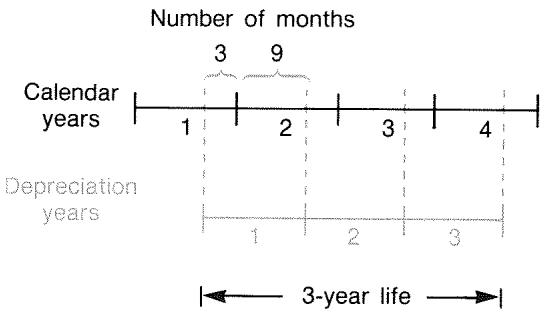

| 108 | Partial-Year Depreciation |

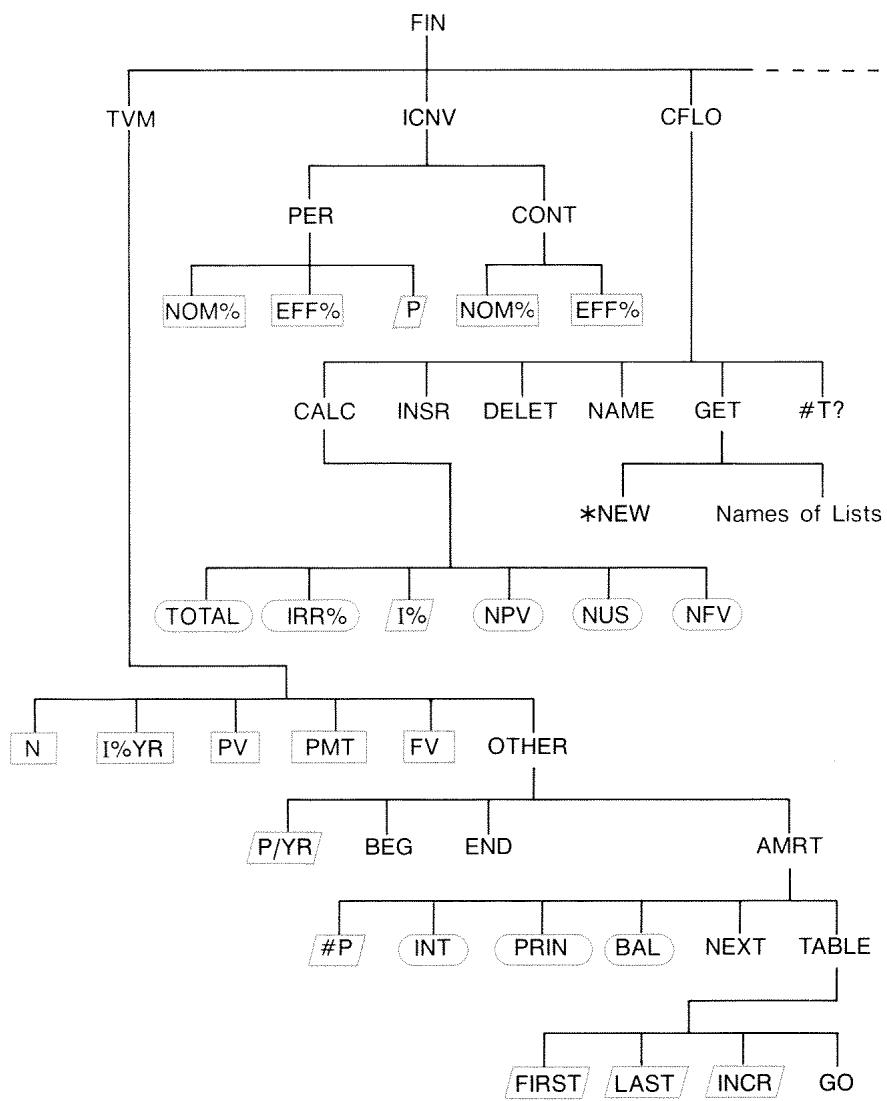

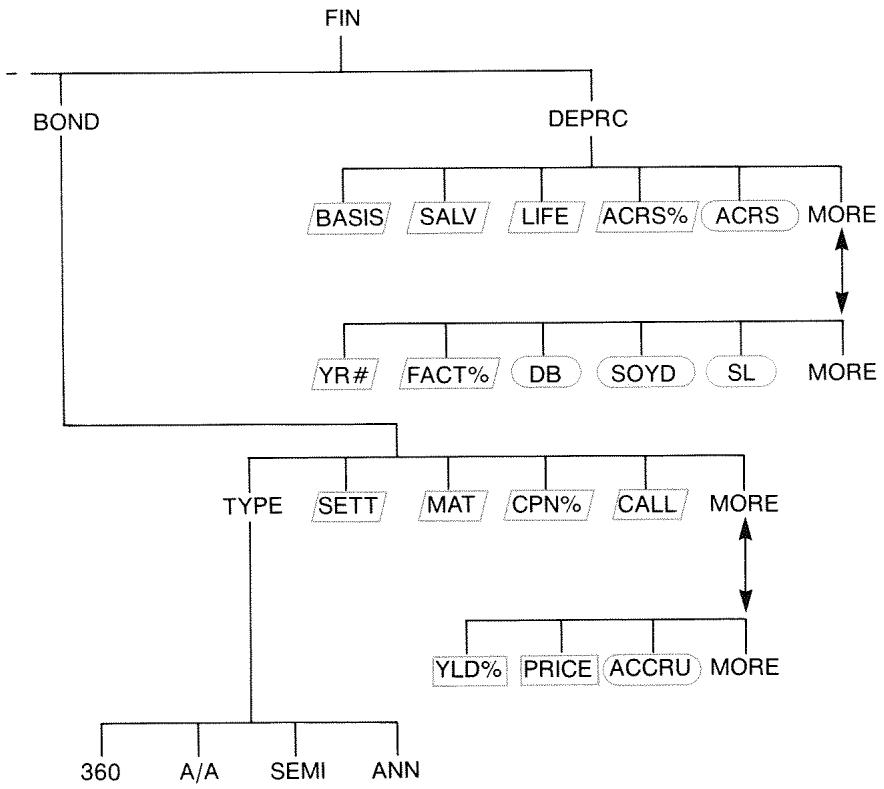

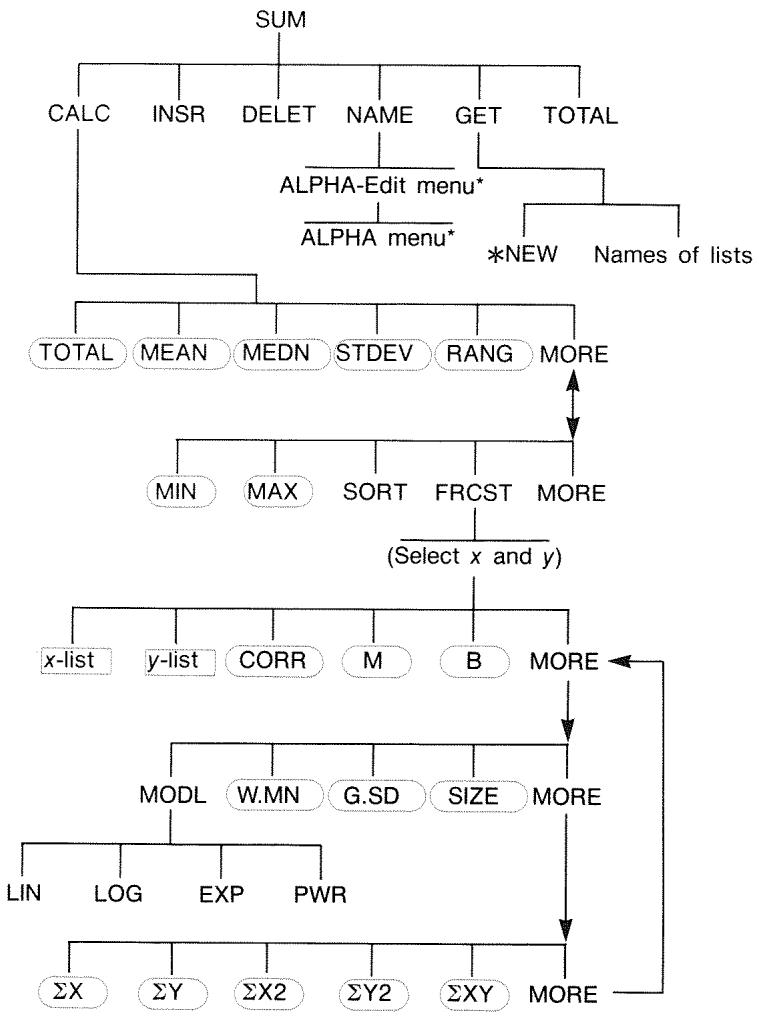

C 243 Menu Maps

D 249 RPN: Summary

249 About RPN

249 About RPN on the HP-17B II

250 Setting RPN Mode

251 Where the RPN Functions Are

252 Doing Calculations in RPN

252 Arithmetic Topics Affected by RPN Mode

252 Simple Arithmetic

254 Calculations With STO and RCL

255 Chain Calculations-No Parentheses!

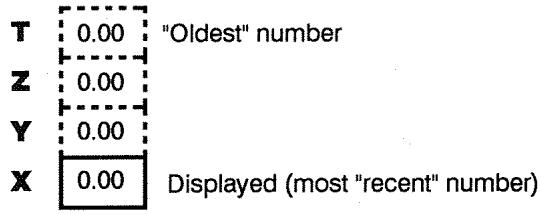

E 256 RPN: The Stack

256 What the Stack Is

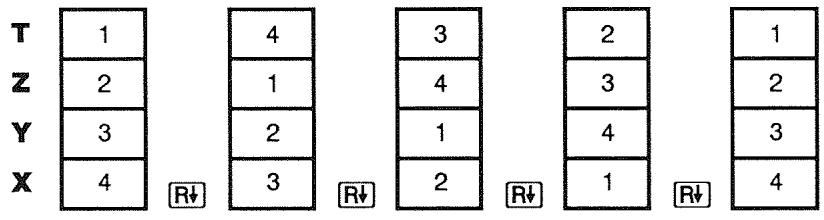

257 Reviewing the Stack (Roll Down)

257 Exchanging the X- and Y-Registers in the Stack

258 Arithmetic-How the Stack Does It

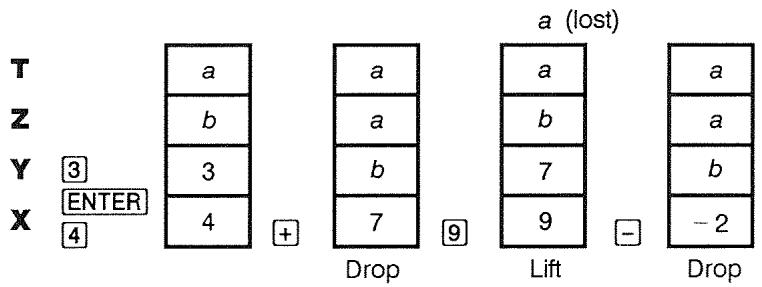

259 How ENTER Works

260 Clearing Numbers

261 The LAST X Register

261 Retrieving Numbers From LAST X

261 Reusing Numbers

262 Chain Calculations

263 Exercises

F 264 RPN: Selected Examples

271 Error Messages

276 Index

List of Examples

The following list groups the examples by category.

Getting Started

22 Using Menus

26 Using the Solver

Arithmetic

37 Calculating Simple Interest

166 Unit Conversions

178 Simple Interest at an Annual Rate (RPN example on page 264)

General Business Calculations

46 Percent Change

47 Percent of Total

47 Markup as a Percent of Cost

48 Markup as a Percent of Price

49 Using Shared Variables

147 Return on Equity

Time Value of Money

56 A Car Loan

57 A Home Mortgage

59 A Mortgage with a Balloon Payment

60 A Savings Account

62 An Individual Retirement Account

63 Calculating a Lease Payment

64 Present Value of a Lease with Advanced Payments and Option to Buy

69 Displaying an Amortization Schedule for a Home Mortgage

71 Printing an Amortization Schedule

160 Calculations for a Loan with an Odd First Period

179 Discounted Mortgage

181 APR for a Loan with Fees

(RPN example on page 264)

182 Loan from the Lender's Point of View

(RPN example on page 265)

184 Loan with an Odd First Period

185 Loan with an Odd First Period Plus Balloon

186 Canadian Mortgage

188 Leasing with Advance Payments

189 A Fund with Regular Withdrawals

191 Savings for College (RPN example on page 266)

195 Tax-Free Account (RPN example on page 268)

197 Taxable Retirement Account

(RPN example on page 269)

202 Insurance Policy

Interest Rate Conversions

75 Converting from a Nominal to an Effective Interest Rate

78 Balance of a Savings Account

Cash Flow Calculations

86 Entering Cash Flows

90 Calculating IRR and NPV of an Investment

93 An Investment with Grouped Cash Flows

95 An Investment with Quarterly Returns

199 Modified IRR

Bonds and Notes

100 Price and Yield of a Bond

101 A Bond with a Call Feature

102 A Zero-Coupon Bond

203 Yield to Maturity and Yield to Call

205 Price and Yield of a Discounted Note

Depreciation

105 Declining-Balance Depreciation

107 ACRS Deductions

109 Partial-Year Depreciation

Running Total and Statistical Calculations

114 Updating a Checkbook

118 Mean, Median, and Standard Deviation

124 Curve Fitting

127 Weighted Mean

207 A Moving Average in Manufacturing

209 Expected Throws of a Die (x2)

Time, Alarms, and Date Arithmetic

132 Setting the Date and Time

137 Clearing and Setting an Appointment

139 Calculating the Number of Days between Two Dates

140 Determining a Future Date

How to Use the Equation Solver

142 Return on Equity

154 Sales Forecasts

160 Using a Solver Function (USPV)

163 Nested IF Functions

169 Using Guesses to Find a Solution Iteratively

Printing

176 Trace-Printing an Arithmetic Calculation

Important Information

Take the time to read chapter 1. It gives you an overview of how the calculator works, and introduces terms and concepts that are used throughout the manual. After reading chapter 1, you'll be ready to start using all of the calculator's features.

- You can choose either ALG (Algebraic) or RPN (Reverse Polish Notation) mode for your calculations. Throughout the manual, the "√" in the margin indicates that the examples or keystrokes must be performed differently in RPN. Appendixes D, E, and F explain how to use your calculator in RPN mode.

- Match the problem you need to solve with the calculator's capabilities and read the related topic. You can locate information about the calculator's features using the table of contents, the subject index, the list of examples, and the menu maps in appendix C (the gold-edged pages).

Before doing any time-value-of-money or cash-flow problems, refer to pages 53 and 82 to learn how the calculator uses positive and negative numbers in financial calculations.

■ For a deeper treatment of specific types of calculations, refer to chapter 13, "Additional Examples." If you especially like learning by example, this is a good reference spot for you.

Getting Started

Watch for this symbol in the margin. It identifies examples or keystrokes that are shown in ALG mode and must be performed differently in RPN mode. Appendixes D, E, and F explain how to use your calculator in RPN mode.

The mode affects only arithmetic calculations—all other operations, including the Solver, work the same in RPN and ALG modes.

Power On and Off; Continuous Memory

To turn on the calculator, press (clear) (note ON printed below the key). To turn it off, press and then . This shifted function is called (note OFF printed above the key). Since the calculator has Continuous Memory, turning it off does not affect the information you've stored there.

To conserve energy, the calculator turns itself off after 10 minutes of no use.

If you see the low battery symbol (□) at the top of the display, you should replace the batteries as soon as possible. Follow the instructions on page 214.

Adjusting the Display Contrast

The display's brightness depends on lighting, your viewing angle, and the display contrast setting. To change the display contrast, hold down the key and press + or - .

What You See in the Display

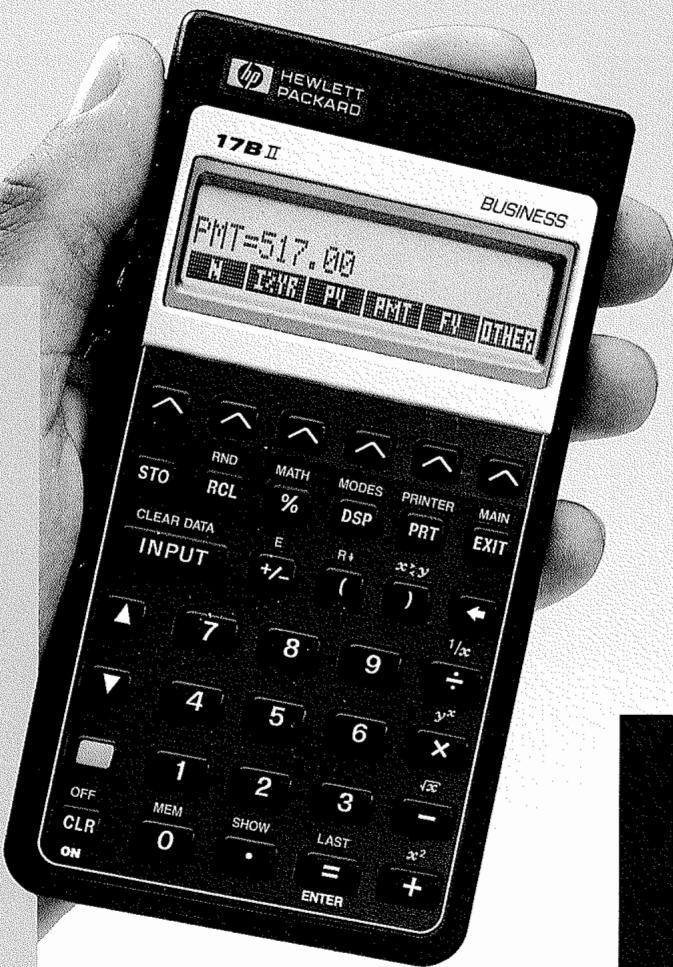

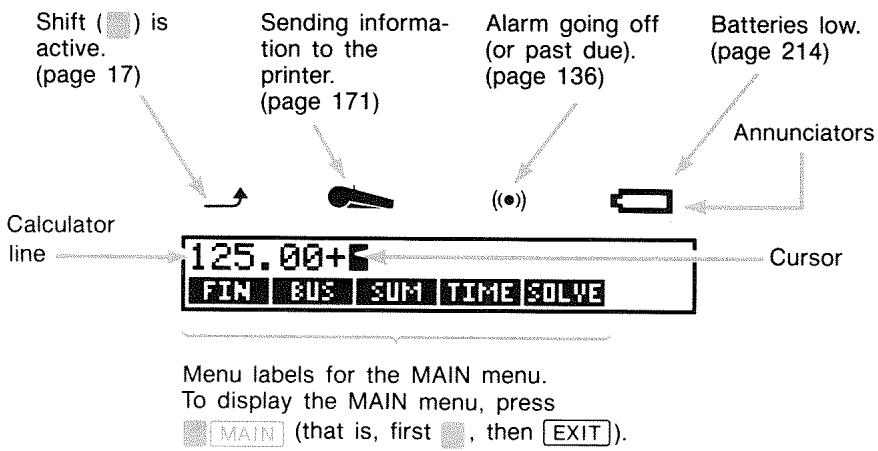

Menu Labels. The bottom line of the display shows the menu labels for each of the five major menus (work areas) in the calculator. More about these later in this chapter.

The Calculator Line. The calculator line is where you see numbers (or letters) that you enter, and the results of calculations.

Annunciators. The symbols shown here are called annihilators. Each one has a special significance.

The Shift Key (

Some keys have a second, shifted function printed in color above the key. The colored shift key accesses these operations. For example, pressing and releasing , then pressing turns the calculator off. This is written OFF.

Pressing turns on the shift annunciator (→) . This symbol stays on until you press the next key. If you ever press by mistake, just press again to turn off the → .

Backspacing and Clearing

The following keys erase typing mistakes, entire numbers, or even lists or sets of data.

Table 1-1. Keys for Clearing

| Key | Description |

| CLR | Backspace; erases the character before the cursor. Clear; clears the calculator line. (When the calculator is off, this key turns the calculator on, but without clearing anything.) |

| CLEAR DATA | This clears all information in the current work area (menu). For example, it will erase all the numbers in a list if you are currently viewing a list (SUM or CFLO). In other menus (like TVM), CLEAR DATA clears all of the values that have been stored. In SOLVE, it can delete all equations. |

The cursor () is visible while you are keying in a number or doing a calculation. When the cursor is visible, pressing lubsuit deletes the last character you keyed in. When the cursor is not visible, pressing lubsuit erases the last number.

| Keys: | Display: | Description: |

| 12345 | Backspacing removes the 4 and 5. | |

| .66 | 123.66 | Calculates 1/123.66. |

| i/x | 0.01 | |

| 0.00 | C clears the calculator line. |

In addition, there are more drastic clearing operations that erase more information at once. Refer to "Resetting the Calculator" on page 217 in appendix A.

Doing Arithmetic

The “ ” in the margin is a reminder that the example keystrokes are for ALG mode.

This is a brief introduction to doing arithmetic. More information on arithmetic is in chapter 2. Remember that you can erase errors by pressing or .

To calculate 21.1 + 23.8:

| Keys: | Display: | Description: |

| 21.1 + | 21, 10+ | |

| 23.8 | 21, 10+23, 8 | |

| = | 44, 90 | = completes calculation. |

Once a calculation has been completed, pressing another digit key starts a new calculation. On the other hand, pressing an operator key continues the calculation:

| 77.35 | 77.35- | Calculates |

| 77.35 - 90.89. |

| 90.89 | -13.54 |

| 65 √x × 12 | New calculation: |

| = | √65 × 12. |

| ÷ 3.5 | = | 27.64 | Calculates 96.75 ÷ 3.5. |

You can also do long calculations without pressing = after each intermediate calculation—just press it at the end. The operators perform from left to right, in the order you enter them. Compare:

6 5 + 1 23 . 5 and 6 5 + 1 23 . 5

| 65 + 12 ÷ | Operations occur in the order you see them. | |

| 3.5 = | 22.00 | |

| 65 | 12 | 12 |

| 3.5 | 68.43 |

Keying in Negative Numbers (+/-)

The + key changes the sign of a number.

To key in a negative number, type that number, then press 7 .

To change the sign of an already displayed number (it must be the rightmost number), press +/- .

| Keys: | Display: | Description: |

| 75 +/- | -75 | Changes the sign of 75. |

| × 7.1 = | -532.50 | Multiplies -75 by 7.1. |

Using the Menu Keys

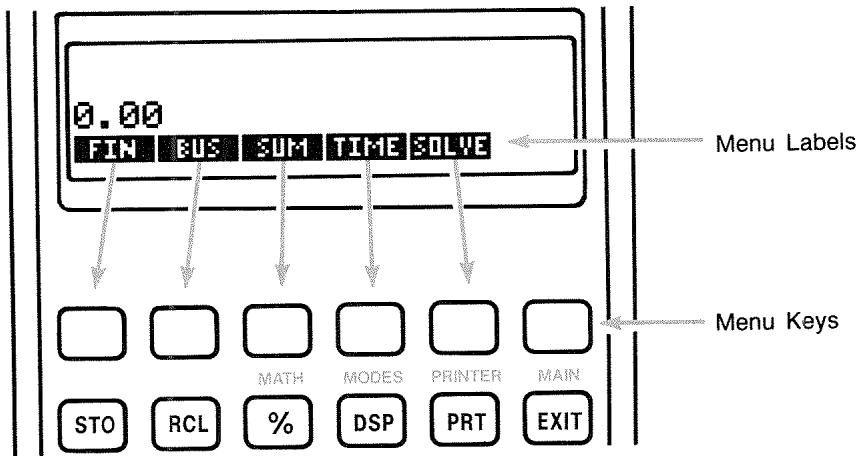

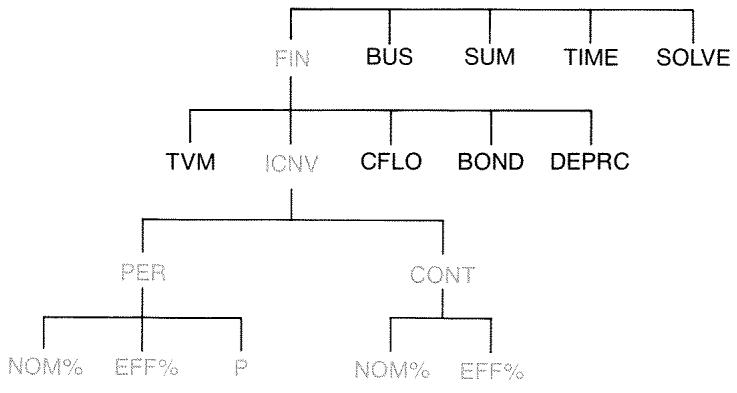

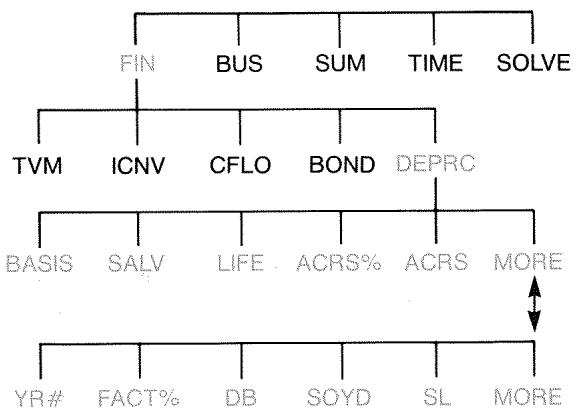

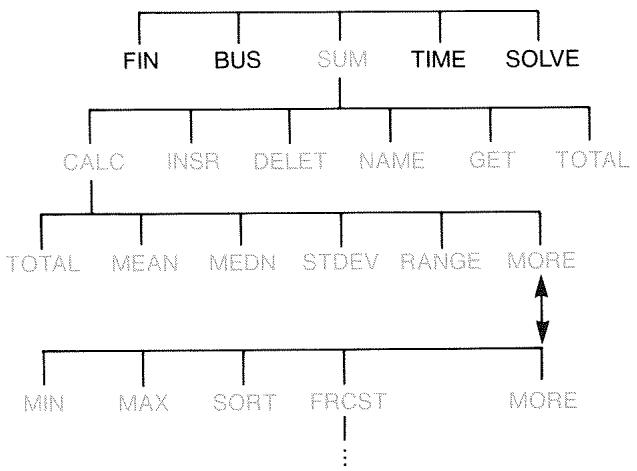

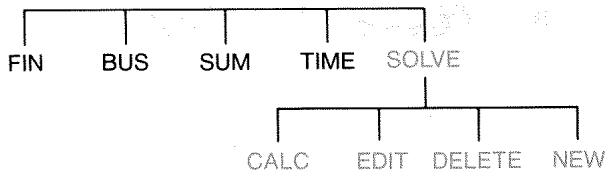

The calculator usually displays a set of labels across the bottom of the display. The set is called a menu because it presents you with choices. The MAIN menu is the starting point for all other menus.

The top row of keys is related to the labels along the bottom of the display. The labels tell you what the keys do. The six keys are called menu keys; the labels are called menu labels.

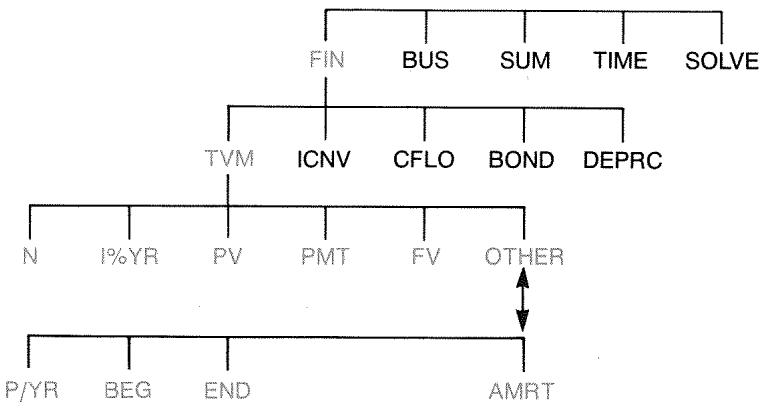

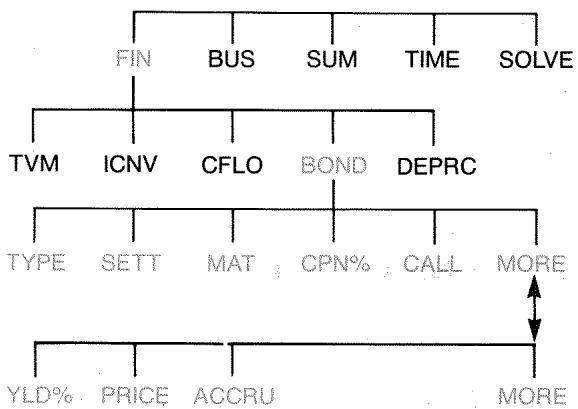

The MAIN Menu

The MAIN menu is a set of primary choices leading to other menu options. No matter which menu you currently see, pressing main redistributes the MAIN menu. The menu structure is hierarchical.

Table 1-2. The MAIN Menu

| Menu Label | Operations Done in This Category | Covered in: |

| FIN (Finance) | TVM: Time value of money: loans, savings, leasing, amortization. | Chapter 4 |

| ICNV: Interest conversions. | Chapter 5 | |

| CFLO: Lists of cash flows for internal rate of return and net present value. | Chapter 6 | |

| BOND: Yields and prices for bonds. | Chapter 7 | |

| DEPRC: Depreciation using SL, DB, and SOYD methods, or ACRS. | Chapter 8 | |

| BUS (Business Percentages) | Percent of total, percent change, markup on cost, markup on price. | Chapter 3 |

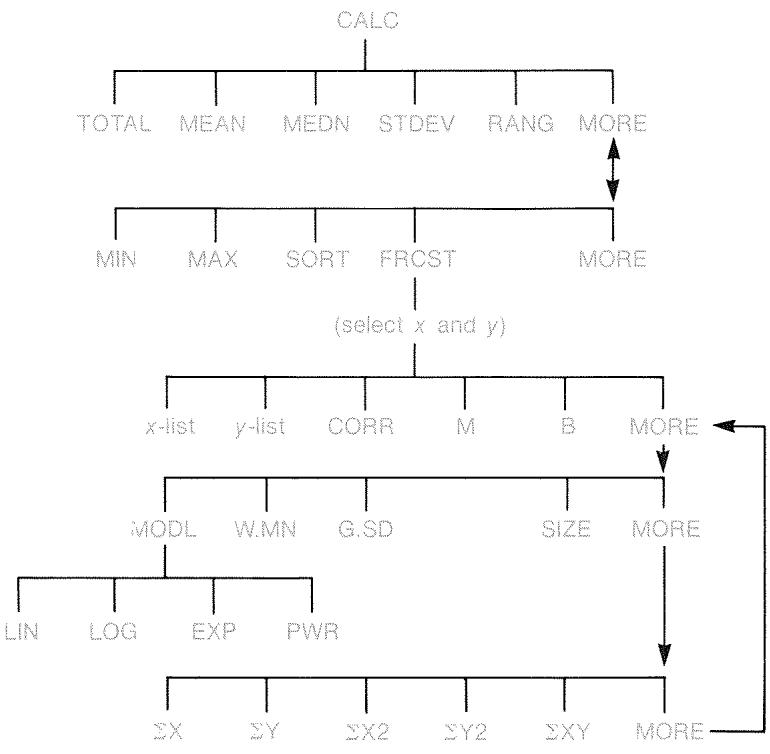

| SUM (Statistics) | Lists of numbers, running total, mean, weighted statistics, forecasting, summation statistics, and more. | Chapter 9 |

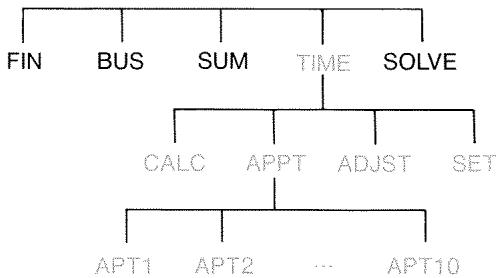

| TIME (Time Manager) | Clock, calendar, appointments, date arithmetic. | Chapter 10 |

| SOLVE (Equation Solver) | Creates customized menus from your own equations for calculations you do often. | Chapter 11 |

Choosing Menus and Reading Menu Maps

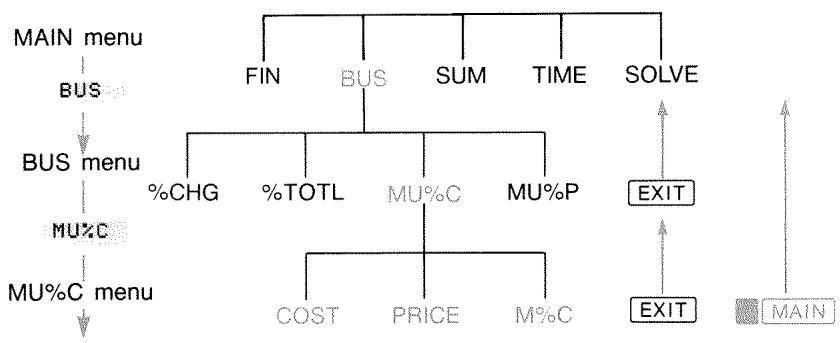

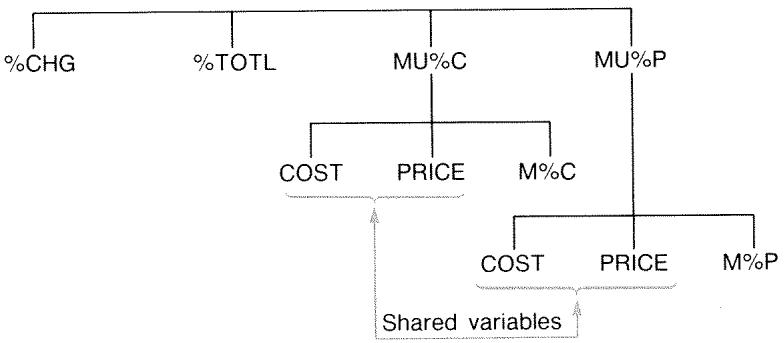

Below is a menu map illustrating one possible path through three levels of menus: from the MAIN menu to the BUS menu to the MU%C (markup as a percent of cost) menu. There are no menus that branch from the MU%C menu because the MU%C menu is a final destination—you use it to do calculations, rather than to choose another menu.

Press BUS to choose the BUS menu. Then press MU%C to choose the MU%C menu.

Press XIT to return to the previous menu. Pressing XIT enough times returns you to the MAIN menu.

Press MAIN to return to the MAIN menu directly.

When a menu has more than six labels, the label MORE appears at the far right. Use it to switch between sets of menu labels on the same "level".

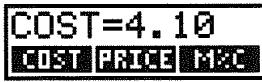

Example: Using Menus. Refer to the menu map for MU%C (above) along with this example. The example calculates the percent markup on cost of a crate of oranges that a grocer buys for 4.10 and sells for 4.60.

Step 1. Decide which menu you want to use. The MU%C (markup as a percent of cost) menu is our destination. If it's not obvious to you which menu you need, look up the topic in the subject index and examine the menu maps in appendix C.

Displaying the MU%C menu:

Step 2. To display the MAIN menu, press MAIN. This step lets you start from a known location on the menu map.

Step 3. Press BUS to display the BUS menu.

Step 4. Press Muzo to display the MU%C menu.

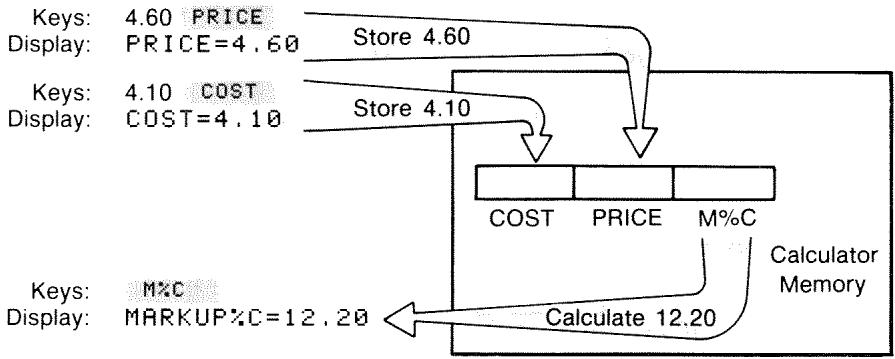

Using the MU%C menu:

Step 5. Key in the cost and press COST to store 4.10 as the COST.

Step 6. Key in the price and press PRICE to store 4.60 as the PRICE.

Step 7. Press MTC to calculate the markup as a percent of cost. The answer: MARKUP%C = 12.20 .

Step 8. To leave the MU%C menu, press EXIT twice (once to get back to the BUS menu, and again to get to the MAIN menu) or MAIN (to go directly to the MAIN menu).

Calculations Using Menus

Using menus to do calculations is easy. You don't have to remember in what order to enter numbers and in what order results come back. Instead, the menus guide you, as in the previous example. All the keys you need are together in the top row. The menu keys both store numbers for the calculations and start the calculations.

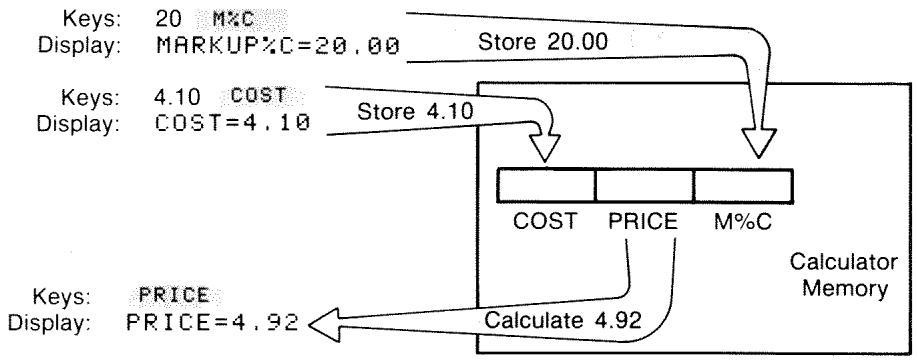

The MU%C menu can calculate M% C , the percent markup on cost, given COST and PRICE.

Then the same menu can calculate PRICE given COST and M% C

Notice that the two calculations use the same three variables; each variable can be used both to store and calculate values. These are called built-in variables, because they are permanently built into the calculator.

Many menus in this calculator work like the example above. The rules for using variables are:

To store a value, key in the number and press the menu key.* Arithmetic calculations, as well as single values, can be stored.

To calculate a value, press the menu key without first keying in a number. The calculator displays CALCULATING when a value is being calculated.

To verify a stored value, press RCL (recall) followed by the menu key. For example, RCL COST displays the value stored in COST.

To transfer a value to another menu, do nothing if it is displayed (that is, it is in the calculator line). A number in the calculator line remains there when you switch menus. To transfer more than one value from a menu, use storage registers. See page 42, "Storing and Recalling Numbers."

Exiting Menus (EXIT)

The key is used to leave the current menu and go back to the previously displayed menu (as shown in the previous example). This is true for menus you might pick by accident, too: gets you out.

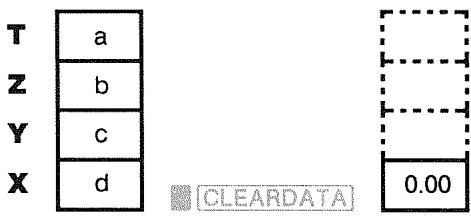

Clearing Values in Menus

The Clear Data key is a powerful feature to clear all the data in the currently displayed menu, giving you a clean slate for new calculations.

If the current menu has variables (that is, if the display shows menu labels for variables, such as COST, PRICE, and M% C in the MU % C menu), pressing CLEAR DATA clears the values of those variables to zero.

If the current menu has a list (SUM, CFLO, or Solver), pressing CLEAR DATA clears the values in the list.

To see what value is currently stored in a variable, press RCL menu label.

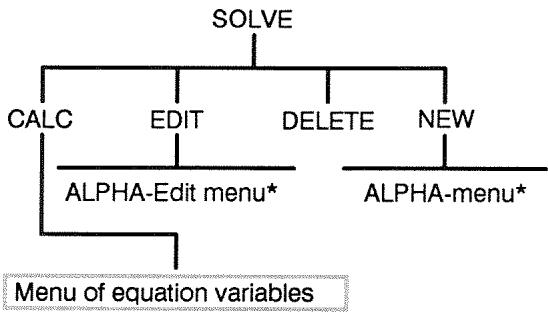

Solving Your Own Equations (SOLVE)

This chapter has introduced some of the built-in menus the calculator offers. But if the solution to a problem is not built into HP-17B, you can turn to the most versatile feature of all: the Equation Solver. Here you define your own solution in terms of an equation. The Solver then creates a menu to go with your equation, which you can use over and over again, just like the other menus in the calculator.

The Solver is covered in chapter 11, but here is an introductory example. Because equations usually use letters of the alphabet, this section also explains how to type and edit letters and other characters that aren't on the keyboard.

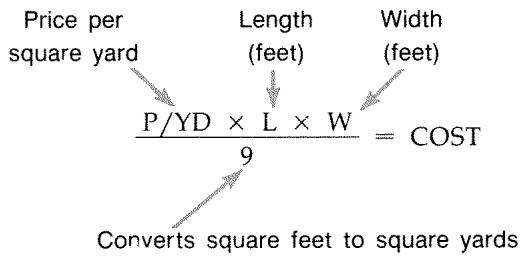

Example: Using the Solver. Suppose you frequently buy carpet and must calculate how much it will cost. The price is quoted to you per square yard. Regardless of how you do the calculation (even if you do it longhand), you are using an equation.

To type this equation into the Solver, use the ALPHA menu.

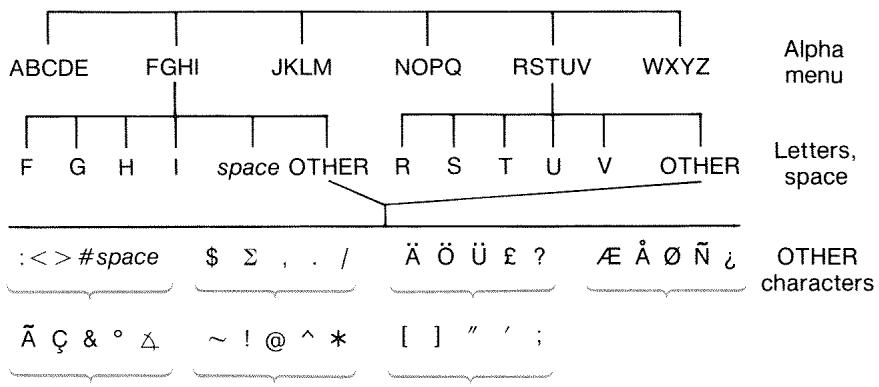

Typing Words and Characters: the ALPHAbetic Menu

The ALPHAbetic menu is automatically displayed when you need it to type letters and characters. The ALPHA menu also includes characters not found on the keyboard:

Uppercase letters.

Space.

■ Punctuation and special characters.

Non-English letters.

To type a letter you need to press two keys; for example, is produced by the keystrokes ABCDE R

Each letter menu has anOTHERkey for accessing punctuation and non-English characters. The letter menus with just four letters (for example, FGHI) include a space character (

To familiarize yourself with the ALPHA menu, type in the equation for the cost of carpeting. The necessary keystrokes are shown below. (Note the access to the special character, "/".) Use , if necessary, to make corrections. If you need to do further editing, refer to the next section, "Editing ALPHAbetic Text." When you're satisfied that the equation is correct, press INPUT to enter the equation into memory.

Keys

Characters

MAIN

SOLVE NEW

NOPQ

P

MORE

P

WXYZ

OTHER

MORE

P

WXYZ

Y

ABCOE

P/YD

JKLM

藻

图

P,YD×L×

WXYZ

H

P/YD×L×W÷9=

ABCDE

C

NOPQ

0

P/YD×L×W=9=CO

RSTUV

5

RSTUV

T

P/YD×L×W÷9=COST

INPUT

P,YD×L×W÷9=COST

Note that the is just a character, part of the variable's name. It is not an operator, which ÷ is.

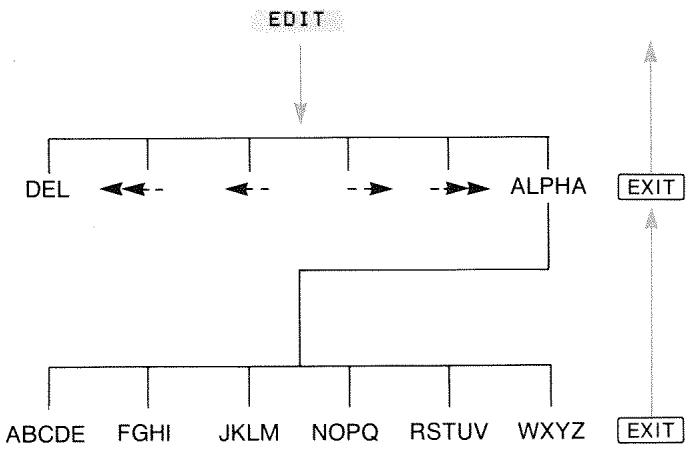

Editing ALPHAbetic Text

The companion to the ALPHA menu is the ALPHA-Edit menu. To display the ALPHA-Edit menu, press EDIT in the SOLVE menu (or press EXIT in the ALPHA menu).

Table 1-3. Alphabetic Editing

| Operation | Label or Key to Press |

| ALPHA-Edit Menu | |

| Inserts character before the cursor. | Any character. |

| Deletes character at the cursor. | DEL |

| Moves the cursor far left, one display-width. | <<-- |

| Moves the cursor left. | <-- |

| Moves the cursor right. | --> |

| Moves the cursor far right, one display-width. | ---> |

| Displays the ALPHA menu again. | ALPHA |

| Keyboard | |

| Backspaces and erases the character before the cursor. | # |

| Clears the calculator line. | CLR |

Calculating the Answer (CALC)

After an equation is input, pressing calc verifies it and creates a new, customized menu to go with the equation.

Menu labels for your variables

Each of the variables you typed into the equation now appears as a menu label. You can store and calculate values in this menu the same way you do in other menus.

Calculate the cost of carpet needed to cover a 9' by 12' room. The carpet costs $22.50 per square yard.

Starting from the MAIN menu (press MAIN):

| Keys: | Display: | Description: |

| SOLVE | P/YD×L×W÷9=COST | Displays the SOLVE menu and the current equation.* |

| CALC | Displays the customized menu for carpeting. | |

| 22.5 P/YD | P/YD=22.50 | Stores the price per square yard in P/YD. |

| 12 L | L=12.00 | Stores the length in L. |

| 9 W | W=9.00 | Stores the width in W. |

| COST | COST=270.00 | Calculates the cost to cover a 9' × 12' room. |

Now determine the most expensive carpet you can buy if the maximum amount you can pay is $300. Notice that all you need to do is enter the one value you are changing—there is no need to re-enter the other values.

300 COST COST=300.00 Stores $300 in COST.

P/YD P/YD=25.00 Calculate the maximum price per square yard you can pay.

EXIT EXIT Exits Solver.

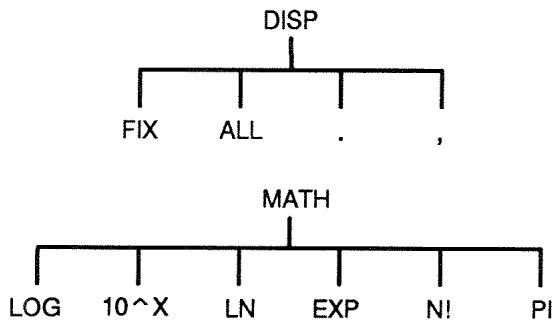

Controlling the Display Format

The DSP menu (press DSP) gives you options for formatting numbers. You can pick the number of decimal places to be displayed, and whether to use a comma or a period to "punctuate" your numbers.

- If you entered this equation but don't see it now, press or until you do.

Decimal Places

To change the number of displayed decimal places, first press the DSP key. Then either:

Press FIX, type the number of decimal places you want (from 0 to 11), and press INPUT; or

Press ALL to see a number as precisely as possible at any time (12 digits maximum).

Internal Precision

Changing the number of displayed decimal places affects what you see, but does not affect the internal representation of numbers. The number inside the calculator always has 12 digits.

Temporarily SHOWing ALL

To temporarily see a number with full precision, press SHOW. This shows you the ALL format for as long as you hold down SHOW.

Rounding a Number

The RND function rounds the number in the calculator line to the number of displayed decimal places. Subsequent calculations use the rounded value.

Starting with two displayed decimal places:

| Keys: | Display: | Description: |

| 5.787 | 5.787■ | |

| DSP FIX4 [INPUT] | 5.7870 | Four decimal places are displayed. |

| DSP ALL | 5.787 | All significant digits; trailing zeros dropped. |

| DSP FIX2 [INPUT] | 5.79 | Two decimal places are displayed. |

| SHOW(hold) | FULL PRECISION IS:5.787 | Temporarily shows full precision. |

| RNDSHOW (hold) | 5.79 | Rounds the number to two decimal places. |

Exchanging Periods and Commas in Numbers

To exchange the periods and commas used for the decimal point and digit separators in a number:

- Press DSP to access the DSP (display) menu.

- Specify the decimal point by pressing or . Pressing sets a period as the decimal point and comma as the digit separator (U.S. mode). (For example, 1,000,000.00.) Pressing sets a comma as the decimal point and period as the digit separator (non-U.S. mode). (For example, 1.000.000.00.)

Error Messages

Sometimes the calculator cannot do what you "ask", such as when you press the wrong key or forget a number for a calculation. To help you correct the situation, the calculator beeps and displays a message.

Press CLR or to clear the error message.

Press any other key to clear the message and perform that key's function.

For more explanations, refer to the list of error messages just before the subject index.

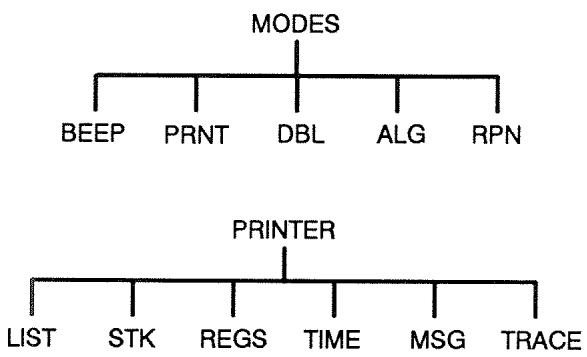

Modes

Beeper. Beeping occurs when a wrong key is pressed, when an error occurs, and during alarms for appointments. You can suppress and re-activate the beeper in the MODES menu as follows:

- Press MODES

- Pressing BEEP will simultaneously change and display the current setting for the beeper:

BEEPER ON beeps for errors and appointments.

BEEPER ON: APPTS ONLY beeps only for appointments.

BEBPER OFF silences the beeper completely.

- Press EXIT when done.

Print. Press MODES PRINT to specify whether or not the printer ac adapter is in use. Then press EXIT.

Double Space. Press MODES DEL to turn double-spaced printing on or off. Then press EXIT.

Algebraic. Press MODES FLG to select algebraic entry logic.

RPN. Press [MODES] RPH to select Reverse Polish Notation entry logic.

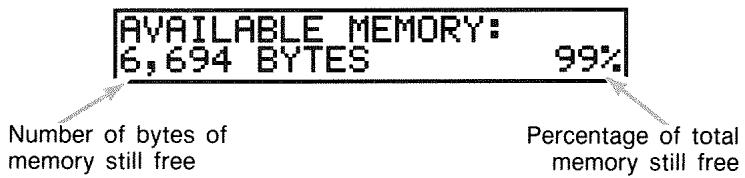

Calculator Memory (MEM)

The calculator stores many different types of information in its memory. Each piece of information requires a certain amount of storage space.* You can monitor the amount of available memory by pressing

The amount of memory available for storing information and working problems is about 6,750 bytes. (Units of memory space are called bytes.) The calculator gives you complete flexibility in how you use that available memory (such as for lists of numbers or equations). Use as much of the memory as you want for any task you want.

If you use nearly all of the calculator's memory, you'll encounter the message INSUFFICIENT MEMORY. To remedy this situation, you must erase some previously stored information. Refer to "Managing Calculator Memory" on page 216 in appendix A.

The calculator also allows you to erase at once all the information stored inside it. This procedure is covered in "Erasing Continuous Memory" on page 218.

- Storing numbers in menus like TVM (non-Solver menus) does not use any of your memory space.

† There are 8,000 bytes total in RAM (random access memory): 6,750 bytes plus 1,250 bytes reserved by the system to store your values in built-in variables.

Arithmetic

If you prefer RPN to algebraic logic, please read appendix D before you read this chapter. The “ heckmark ” in the margin is a reminder that the example keystrokes are for ALG mode.

The Calculator Line

The calculator line is the part of the display where numbers appear and calculations take place. Sometimes this line includes labels for results, such as TOTAL = 124.60 . Even in this case you can use the number for a calculation. For example, pressing + 2 would calculate 124.60 plus 2, and the calculator would display the answer, 126.60.

There is always a number in the calculator line, even though sometimes the calculator line is hidden by a message (such as SELECT COMPOUNDING). To see the number in the calculator line, press 4 , which removes the message.

heckmark Doing Calculations

Simple calculating was introduced in chapter 1, page 19. Often longer calculations involve more than one operation. These are called chain calculations because several operations are "chained" together. To do a chain calculation, you don't need to press = after each operation, but only at the very end.

For instance, to calculate 750 × 12360 you can type either:

750 12 = 360

or

750 × 12 ÷ 360 =

In the second case, the ÷ key acts like the = key by displaying the result of 750 × 12 .

Here's a longer chain calculation.

4 5 6 - 7 51 8 . 5 × 6 81 . 9

This calculation can be written as: 456 - 75 ÷ 18.5 × 68 ÷ 1.9 .

Watch what happens in the display as you key it in:

Keys: Display:

456 75 381.00÷

18.5 20.59x

68 1,400,43÷

1.9 737.07

Using Parentheses in Calculations

Use parentheses when you want to postpone calculating an intermediate result until you've entered more numbers. For example, suppose you want to calculate:

3 08 5 - 1 2 × 9

If you were to key in 30 ÷ 85 , the calculator would calculate the intermediate result, 0.35. However, that's not what you want. To delay the division until you've subtracted 12 from 85, use parentheses:

| Keys: | Display: | Description: |

| 30÷85 | 30.00÷(85.00- | No calculation is done. |

| 12 | 30.00÷73.00 | Calculates 85 - 12. |

| ×9 | 0.41×9 | Calculates 30 / 73. |

| = | 3.70 | Calculates 0.41 × 9. |

Note that you must include a for multiplication; parentheses do not imply multiplication.

The Percent Key

The % key has two functions:

Finding a Percentage. In most cases, % divides a number by 100. The one exception is when a plus or minus sign precedes the number. (See "Adding or Subtracting a Percentage," below.)

For instance, 25 % results in 0.25.

To find 25% of 200, press: 200 × 25 % . (Result is 50.00.)

Adding or Subtracting a Percentage. You can do this all in one calculation:

For instance, to decrease 200 by 25% , just enter 200 - 25% = 150.00 . (Result is 150.00 .)

Example: Calculating Simple Interest. You borrow $1,250 from a relative, and agree to repay the loan in a year with 7% simple interest. How much money will you owe?

| Keys: | Display: | Description: |

| 1250 + 7 % | 1,250.00+87.50 | Interest on the loan is $87.50. |

| 1,337.50 | You must repay this amount at the end of one year. |

The Mathematical Functions

Some of the math functions appear on the keyboard; others are in the MATH menu. Math functions act on the last number in the display.

Table 2-1. Shifted Math Functions

| Key | Description |

| 1/x | reciprocal |

| √x | square root |

| 2/x | square |

| Keys: | Display: | Description: |

| 4 1/x | 0.25 | Reciprocal of 4. |

| 20 √x | 4.47 | Calculates √20. |

| + 47.2 x | 51.67x | Calculates 4.47 + 47.20. |

| 1.1 x² | 51.67x1.21 | Calculates 1.1². |

| = | 62.52 | Completes calculation of (4.47 + 47.2) × 1.1². |

The Power Function (Exponentiation)

The power function, x , raises the preceding number to the power of the following number.

| Keys: | Display: | Description: |

| 125 yx 3 = | 1,953,125.00 | Calculates 1253. |

| 125 yx 3 | 5.00 | Calculates the cube root of 125, which is the same as (125)1/3. |

The MATH Menu

To display the MATH menu, press MATH (the shifted % key). Like the other mathematics functions, these functions operate on only the last number in the display.

Table 2-2. The MATH Menu Labels

| Menu Label | Description |

| LOG | Common (base 10) logarithm of a positive number. |

| 10^X | Common (base 10) antilogarithm; calculates 10^x. |

| LN | Natural (base e) logarithm of a positive number. |

| EXP | Natural antilogarithm; calculates ex. |

| N! | Factorial. |

| PI | Inserts the value for π into the display. |

| Keys: | Display: | Description: |

| 2.5 | MATH | Calculates 10^2.5. |

| 10^X | 316.23 | |

| 4 | N! | 24.00 |

| EXIT | Calculates the factorial of 4. | |

| Exits MATH menu. |

You can access the MATH menu when another menu is displayed. For instance, while using SUM you might want to use a MATH function. Just press , then perform the calculation. Pressing returns you to SUM. The MATH result remains in the calculator line. Remember, however, that you must exit MATH before you resume using SUM.

Saving and Reusing Numbers

Sometimes you might want to include the result of a previous calculation in a new calculation. There are several ways to reuse numbers.

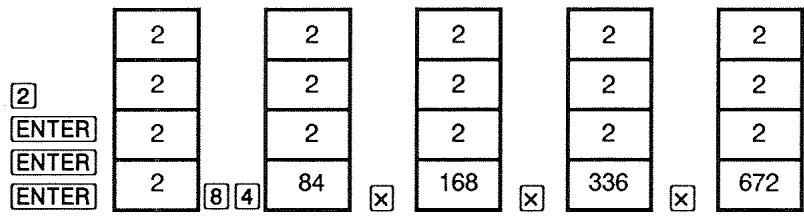

The History Stack of Numbers

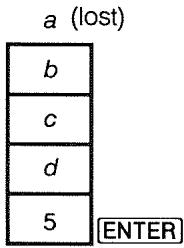

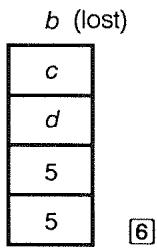

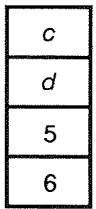

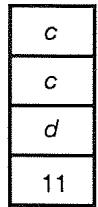

When you start a new operation, the previous result moves out of the display but is still accessible. Up to four lines of numbers are saved: one in the display and three hidden. These lines make up the history stack.

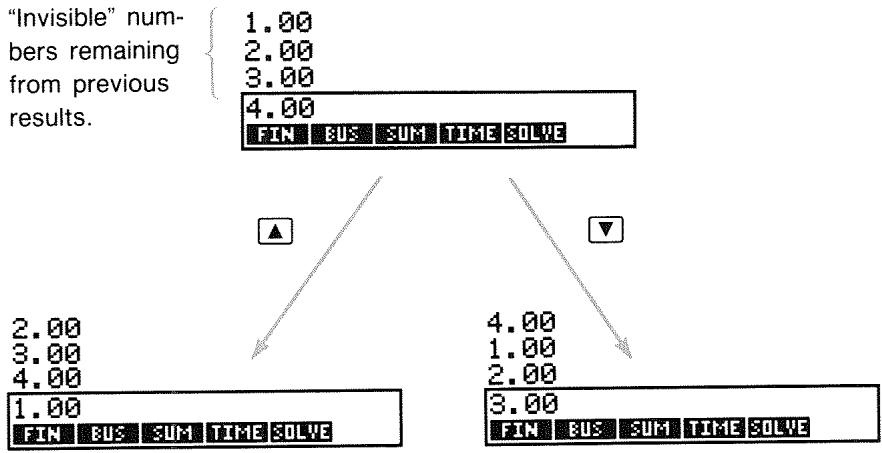

The , , and keys "roll" the history stack down or up one line, bringing the hidden results back into the display. If you hold down or , the history stack wraps around on itself. However, you cannot roll the history stack when an incomplete calculation is in the display. Also, you cannot gain access to the stack while using lists (SUM, CFLO) in ALG mode, or SOLVE in either ALG or RPN mode. All numbers in the history stack are retained when you switch menus.

Pressing exchanges the contents of the bottom two lines of the display.

Pressing CLEAR DATA clears the history stack. Be careful if a menu is active, because then CLEAR DATA also erases the data associated with that menu.

Keys:

Display:

Description:

75.55 32.63

42.92

150

21.43

42.92 moves out of display.

Now, suppose you want to multiply 42.92 × 11 . Using the history stack saves you time.

42.92

Moves 42.92 back to calculator line.

472.12

Reusing the Last Result (LAST)

The LAST key copies the last result—that is, the number just above the calculator line in the history stack—into a current calculation. This lets you reuse a number without retyping it and also lets you break up a complicated calculation.

3 9 + 8 1 2 3 + 1 7

Keys:

Display:

Description:

123 + 17 =

140.00

Calculates 123 + 17

11.83

Calculates 140 .

39 + 8 = ÷

47.00÷11.83

Copies 11.83 to the calculator line.

3.97

Completes the calculation.

An equivalent keystroke sequence for this problem would be:

39+8÷123+17

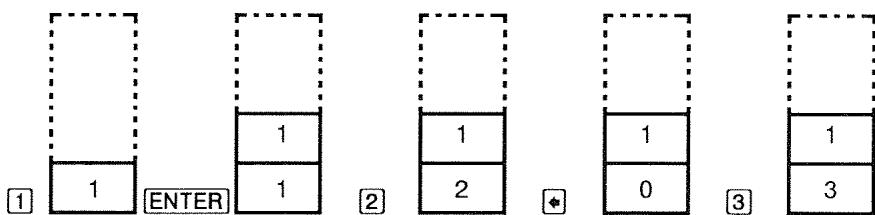

Storing and Recalling Numbers

The key copies a number from the calculator line into a designated storage area, called a storage register. There are ten storage registers in calculator memory, numbered 0 through 9. The key recalls stored numbers back to the calculator line.

√ If there is more than one number on the calculator line, STO stores only the last number in the display.

To store or recall a number:

- Press STO or RCL. (To cancel this step, press lubsuit .)

- Key in the register number.

The following example uses two storage registers to do two calculations that use some of the same numbers.

4 7 5 . 63 9 . 1 5

5 6 0 . 1 + 4 7 5 . 63 9 . 1 5

| ✓ Keys: | Display: | Description: |

| 475.6 STO 1 | 475.60 | Stores 475.6 into register 1. |

| ÷ 39.15 STO 2 | 475.60÷39.15 | Stores 39.15 (rightmost number) into register 2. |

| = | 12.15 | Completes calculation. |

| 560.1 + RCL 1 | 560.10+475.60 | Recalls contents of regis-ter 1. |

| ÷ RCL 2 | 1,035.70÷39.15 | Recalls register 2. |

| = | 26.45 | Completes calculation. |

The STO and RCL keys can also be used with variables. For example, STO MxC (in the MU%C menu) stores the rightmost number from the display into the variable M% C . RCL MxC copies the contents of M% C into the calculator line. If there is an expression in the display (such as 2 + 4 ), then the recalled number replaces only the last number.

You do not need to clear storage registers before using them. By storing a number into a register, you overwrite whatever existed there before.

Doing Arithmetic Inside Registers and Variables

You can also do arithmetic inside storage registers.

| Keys: | Display: | Description: |

| 45.7 STO 3 | 45.70 | Stores 45.7 in reg. 3. |

| 2.5 STO × 3 | 2.50 | Multiplies contents of register 3 by 2.5 and stores result (114.25) back in register 3. |

| RCL 3 | 114.25 | Displays register 3. |

Table 2-3. Arithmetic in Registers

| Keys | New Register Contents |

| STO + | old register contents + displayed number |

| STO - | old register contents - displayed number |

| STO × | old register contents × displayed number |

| STO ÷ | old register contents ÷ displayed number |

| STO ↕ | old register contents ^ displayed number |

You can also do arithmetic with the values stored in variables. For example, 2 × 2C (in the MU%C menu) multiplies the current contents of M% C by 2 and stores the product in M% C .

Scientific Notation

Scientific notation is useful when working with very large or very small numbers. Scientific notation shows a small number (less than 10) times 10 raised to a power. For example, the 1984 Gross National Product of the United States was 3,662,800,000,000 . In scientific notation, this is 3.6628 × 1012 . For very small numbers the decimal point is moved to the right and 10 is raised to a negative power. For example, 0.00000752 can be written as 7.52 × 10-6 .

When a calculation produces a result with more than 12 digits, the number is automatically displayed in scientific notation, using a capital E in place of “ × 10^".

Remember that + / - changes the sign of the entire number, and not of the exponent. Use - to make a negative exponent.

Type in the numbers 4.78 × 1013 and -2.36 × 10-15 .

| Keys: | Display: | Description: |

| 4.78 E 13 | 4.78E13 | Pressing E starts the exponent. |

| CLEAR DATA | 0.00 | Clears number. |

| 2.36 E - 15 | 2.36E-15 | Pressing - before an exponent makes it negative. |

| +/- | -2.36E-15 | Pressing +/− makes the entire number negative. |

| CLEAR DATA | C clears number. |

Range of Numbers

The largest positive and negative numbers available on the calculator are ± 9.99999999999 × 10499 ; the smallest positive and negative numbers available are ± 1 × 10-499 .

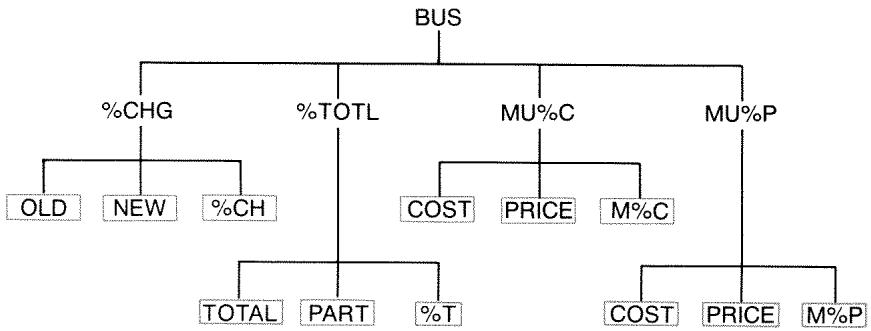

Percentage Calculations in Business

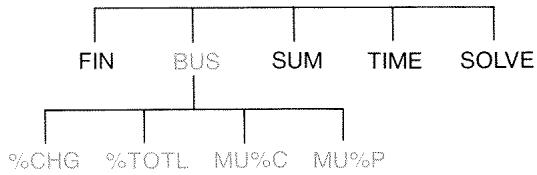

The business percentages (BUS) menu is used to solve four types of problems. Each type of problem has its own menu.

Table 3-1. The Business Percentages (BUS) Menus

| Menu | Description |

| Percent change ( %CHG ) | The difference between two numbers (OLD and NEW), expressed as a percentage (%CH) of OLD. |

| Percent of total ( %TOTAL ) | The portion that one number (PART) is of another (TO-TAL), expressed as a percentage (%T). |

| Markup on cost ( MU×C ) | The difference between price (PRICE) and cost (COST), expressed as a percentage of the cost (M%C). |

| Markup on price ( MU×P ) | The difference between price (PRICE) and cost (COST), expressed as a percentage of the price (M%P). |

The calculator retains the values of the BUS variables until you clear them by pressing CLEAR DATA. For example, pressing CLEAR DATA while in the %CHG menu clears OLD, NEW, and %CH.

To see what value is currently stored in a variable, press RCL menu label. This shows you the value without recalculating it.

Using the BUS Menus

Each of the four BUS menus has three variables. You can calculate any one of the three variables if you know the other two.

- To display the %CHG, %TOTL, MU%C, or MU%P menu from the MAIN menu, press BUS, then the appropriate menu label. Pressing xchg, for example, displays:

- Store each value you know by keying in the number and pressing the appropriate menu key.

- Press the menu key for the value you want to calculate.

Examples Using the BUS Menus

Percent Change (%CHG)

Example. Total sales last year were 90,000. This year, sales were 95,000. What is the percent change between last year's sales and this year's?

| Keys: | Display: | Description: |

| BUS | Displays %CHG menu. | |

| %CHG | ||

| 90000 OLD | OLD=90,000.00 | Stores 90,000 in OLD. |

| 95000 NEW | NEW=95,000.00 | Stores 95,000 in NEW. |

| %CH | %CHANGE=5.56 | Calculates percent change. |

What would this year's sales have to be to show a 12% increase from last year? OLD remains 90,000, so you don't have to key it in again. Just enter % CH and ask for NEW.

12 :CH

% CHANGE = 12.00

Stores 12 in % CH

NEW

NEW=100,800.00

Calculates the value 12% greater than 90,000.

Percent of Total (%TOTL)

Example. Total assets for your company are 67,584. The firm has inventories of23,457. What percentage of total assets is inventory?

You will be supplying values for TOTAL and PART and calculating % T . This takes care of all three variables, so there is no need to use CLEAR DATA to remove old data.

| Keys: | Display: | Description: | ||

| BUS | %TOTAL | Displays %TOTAL menu. | ||

| 67584 | TOTAL | TOTAL=67,584.00 | Stores 67,584 in TOTAL. | |

| 23457 | PART | PART=23,457.00 | Stores23,457 in PART. | |

| %T | %TOTAL=34.71 | Calculates percent of total. | ||

Markup as a Percent of Cost (MU%C)

Example. The standard markup on costume jewelry at Balkis's Boutique is 60% . The boutique just received a shipment of chokers costing $19.00 each. What is the retail price per choker?

| Keys: | Display: | Description: |

| BUS | Displays MU%C menu. | |

| MU%C | ||

| 19 COST | COST=19.00 | Stores cost in COST. |

| 60 M%C | MARKUP%C=60.00 | Stores 60% in M%C. |

| PRICE | PRICE=30.40 | Calculates price. |

Markup as a Percent of Price (MU%P)

Example. Kilowatt Electronics purchases televisions for 225, with a discount of 4%. The televisions are sold for300. What is the markup of the net cost as a percent of the selling price?

What is the markup as percent of price without the 4% discount?

| Keys: | Display: | Description: |

| BUS | Displays MU%P menu. | |

| MU%P | ||

| 225 - 4 % | Calculates and stores net cost in COST. | |

| COST | COST=216.00 | |

| 300 PRICE | PRICE=300.00 | Stores 300 in PRICE. |

| M%P | MARKUP%P=28.00 | Calculates markup as a percent of price. |

Use $225 for COST and leave PRICE alone.

225 COST COST = 225.00 Stores 225 in COST.

MARKUP: P = 25.00 Calculate markup.

Sharing Variables Between Menus

If you compare the MU%C menu and the MU%P menus, you'll see that they have two menu labels in common—cost and PRICE.

The calculator keeps track of the values you key in according to those labels. For example, if you key in COST and PRICE in the MU%C menu, exit to the BUS menu, and then display the MU%P menu, the calculator retains those values. In other words, the variables are shared between the two menus.

Example: Using Shared Variables. A food cooperative buys cases of canned soup with an invoice cost of (9.60 per case. If the co-op routinely uses a (15\%) markup on cost, for what price should it sell a case of soup?

| Keys: | Display: | Description: |

| BUS | Displays MU%C menu. | |

| MU%C | ||

| 9.6 COST | COST=9.60 | Stores 9.60 in COST. |

| 15 M/C | MARKUP%C=15.00 | Stores 15% in M%C. |

| PRICE | PRICE=11.04 | Calculates retail price. |

What is the markup on price? Switch menus but keep the same COST and PRICE.

EXIT MU.P

Exits MU%C menu and displays MU%P menu.

MARKUP%P=13.04

Calculates markup as a percent of price.

Time Value of Money

The phrase time value of money describes calculations based on money earning interest over a period of time. The TVM menu performs compound-interest calculations and calculates (and prints) amortization schedules.

In compound interest calculations, interest is added to the principal at specified compounding periods, thereby also earning interest. Savings accounts, mortgages, and leases are compound-interest calculations.

In simple interest calculations, the interest is a percent of the principal and is repaid in one lump sum. Simple interest calculations can be done using the % key (page 37). For an example that calculates simple interest using an annual interest rate, see page 178.

The TVM Menu

The time value of money (TVM) menu does many compound-interest calculations. Specifically, you can use the TVM menu for a series of cash flows (money received or money paid) when:

The dollar amount is the same for each payment.*

The payments occur at regular intervals.

The payment periods coincide with the compounding periods.

12 payments (or periods) per year

Payment mode: the end of each period

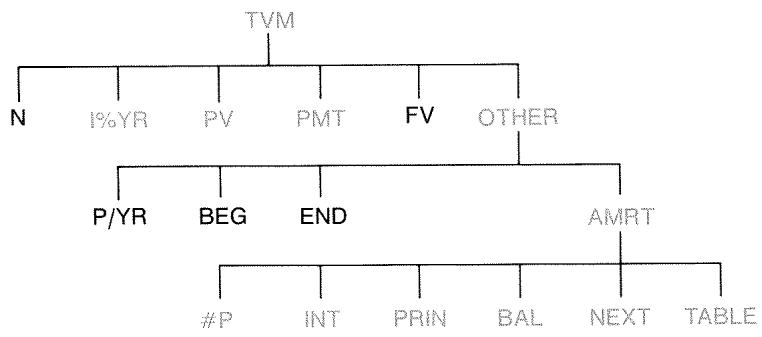

Figure 4-1. The First Level of TVM

To second level of TVM

The first level of the TVM menu has five menu labels for variables plus OTHER. The OTHER key accesses a second-level menu used to specify payment conditions (the payment mode) and to call up the AMRT (amortization) menu.

Figure 4-2. The Second Level of TVM

Table 4-1. TVM Menu Labels

| Menu Label | Description |

| N | First Level Stores (or calculates) the total number of payments or compounding periods.*† (For a 30-year loan with monthly payments, N=12×30=360.) |

| N | Shortcut for N: Multiplies the number in the display by P/YR, and stores the result in N. (If P/YR were 12, then 30 would set N=360.) |

| I*YR | Stores (or calculates) the nominal annual interest rate as a percentage. |

| PV | Stores (or calculates) the present value—an initial cash flow or a discounted value of a series of future cash flows (PMTs + FV). To a lender or borrower, PV is the amount of the loan; to an investor, PV is the initial investment. If PV paid out, it is negative. PV always occurs at the beginning of the first period. |

| PMT | Stores (or calculates) the dollar amount of each periodic payment. All payments are equal, and no payments are skipped. (If the payments are unequal, use CFLO, not TVM.) Payments can occur at the beginning or end of each period. If PMT represents money paid out, it is negative. |

| FV | Stores (or calculates) the future value—a final cash flow or a compounded value of a series of previous cash flows (PV + PMTs). FV always occurs at the end of the last period. If FV is paid out, it is negative. |

| P/YR | specifies the number of payments or compounding periods per year.† (It must be an integer, 1 through 999.) |

| * When a non-integer N (an "odd period") is calculated, the answer must be interpreted carefully. See the savings account example on page 60. Calculations using a stored, non-integer N produce a mathematically correct result, but this result has no simple interpretation. The example on page 160 uses the Solver to do a partial-period (non-integer) calculation in which interest begins to accrue prior to the beginning of the first regular payment period. † The number of payment periods must equal the number of compounding periods. If this is not true, see page 77. For Canadian mortgages, see page 185. | |

| BEG | Second Level (Continued) |

| Sets Begin mode: payments occur at the beginning of each period. Typical for savings plans and leasing. (The Begin and End modes do not matter if PMT=0.) | |

| END | Sets End mode: payments occur at the end of each period. Typical for loans and investments. |

| AMRT | Accesses the amortization menu. See page 67. |

The calculator retains the values of the TVM variables until you clear them by pressing CLEAR DATA. When you see the first-level TVM menu, pressing CLEAR DATA clears N , I% YR, PV, PMT, and FV. When the second-level menu (OTHER) is displayed, pressing CLEAR DATA resets the payment conditions to 12 P/YR END MODE.

To see what value is currently stored in a variable, press RCL menu label. This shows you the value without recalculating it.

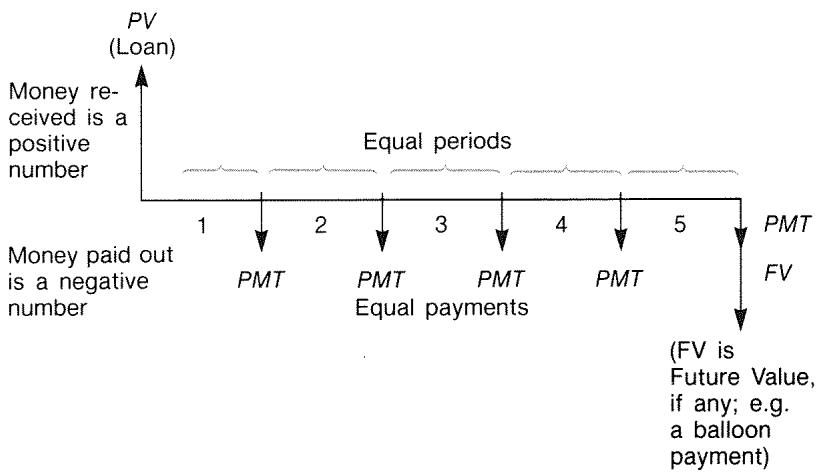

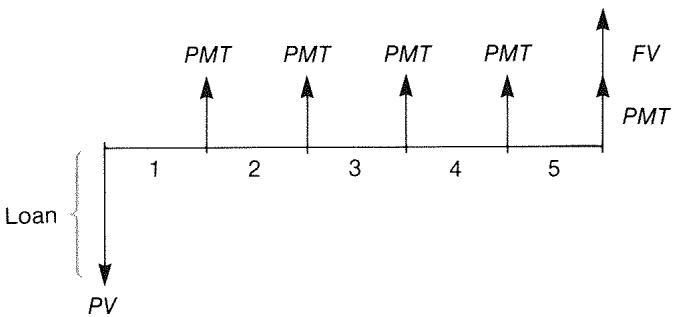

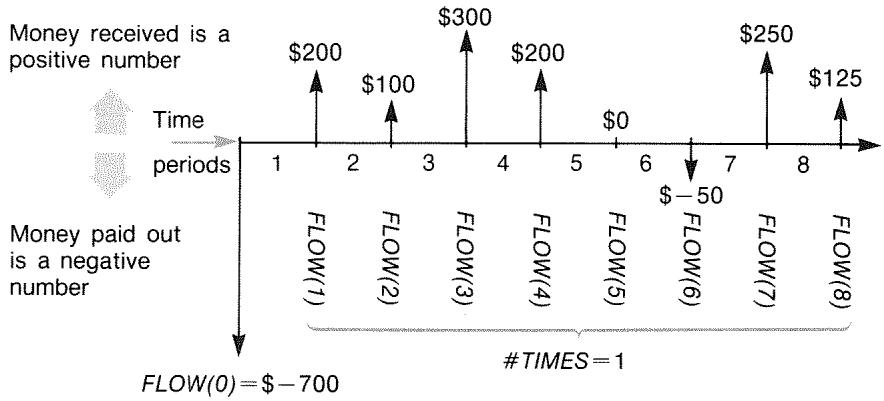

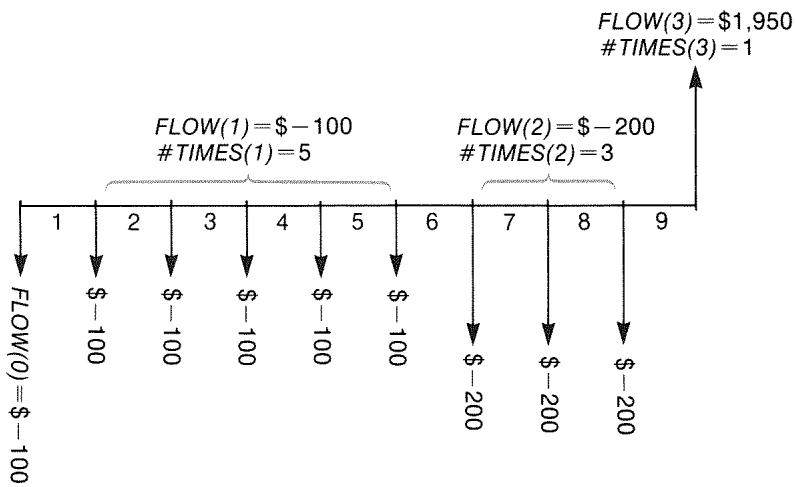

Cash Flow Diagrams and Signs of Numbers

It is helpful to illustrate TVM calculations with cash-flow diagrams. Cash-flow diagrams are time lines divided into equal segments called compounding (or payment) periods. Arrows show the occurrence of cash flows (payments in or out). Money received is a positive number (arrow up) and money paid out is a negative number (arrow down).

Note

The correct sign (positive or negative) for TVM numbers is essential. The calculations will make sense only if you consistently show payments out as negative and payments in (receipts) as positive. Perform a calculation from the

point of view of either the lender (investor) or the borrower, but not both!

Figure 4-3. A Cash Flow Diagram for a Loan from Borrower's Point of View (End Mode)

Figure 4-4. A Cash Flow Diagram for a Loan from Lender's Point of View (End Mode)

Payments occur at either the beginning of each period or the end of each period. End mode is shown in the last two figures; Begin mode is shown in the next figure.

Figure 4-5. Lease Payments Made at the Beginning of Each Period (Begin Mode)

Using the TVM Menu

First draw a cash-flow diagram to match your problem. Then:

1.From the MAIN menu, press FIN TVM

2. To clear previous TVM values, press CLEAR DATA. (Note: You don't need to clear data if you enter new values for all five variables, or if you want to retain previous values.)

3. Read the message that describes the number of payments per year and the payment mode (Begin, End). If you need to change either of these settings, press OTHER.

To change the number of payments per year, key in the new value and press P/YR. (If the number of payments is different from the number of compounding periods, see "Compounding Periods Different from Payment Periods," page 77.)

To change the Begin/End mode, press BEG or END.

Press to return to the primary TVM menu.

- Store the values you know. (Enter each number and press its menu key.)

- To calculate a value, press the appropriate menu key.

You must give every variable—except the one you will calculate—a value, even if that value is zero. For example, FV must be set to zero when you are calculating the periodic payment (PMT) required to fully pay back a loan. There are two ways to set values to zero:

Before storing any TVM values, press CLEAR DATA to clear the previous TVM values.

Store zero; for example, pressing 0 FV sets FV to zero.

Loan Calculations

Three examples illustrate common loan calculations. (For amortization of loan payments, see page 67.) Loan calculations typically use End mode for payments.

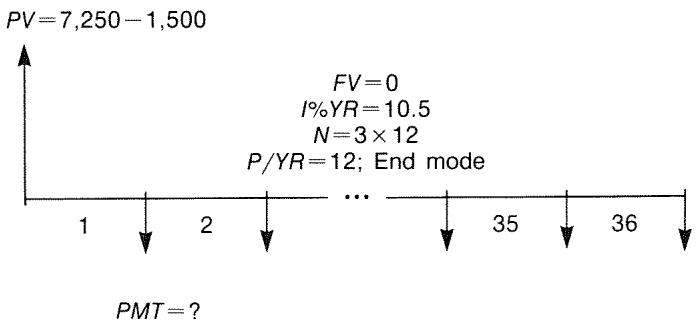

Example: A Car Loan. You are financing the purchase of a new car with a 3-year loan at 10.5% annual interest, compounded monthly. The purchase price of the car is 7,250. Your down payment is1,500. What are your monthly payments? (Assume payments start one month after purchase—in other words, at the end of the first period.) What interest rate would reduce your monthly payment by $10?

| Keys: | Display: | Description: |

| FIN | Displays TVM menu. | |

| TVM | ||

| CLEAR DATA | 0.00 | Cleared history stack and TVM variables. |

| OTHER | If needed: sets 12 pay-ment periods per year;End mode. | |

| CLEAR DATA | 12 P/YR END MODE | |

| EXIT | ||

| 3 × 12 | Figures and stores num ber of payments. | |

| N | N=36.00 | |

| 10.5 I&YR | I%YR=10.50 | Stores annual interest rate. |

| 7250 - 1500 | Stores amount of the loan. | |

| PV | PV=5,750.00 | |

| PMT | PMT=-186.89 | Calculates payment.Negative value means money to be paid out. |

To calculate the interest rate that reduces the payment by (10, add 10 to reduce the negative PMT value.

| + 10 PMT | PMT=-176.89 | Stores the reduced pay- ment amount. |

| I2YR | I2YR=6.75 | Calculates the annual in- terest rate. |

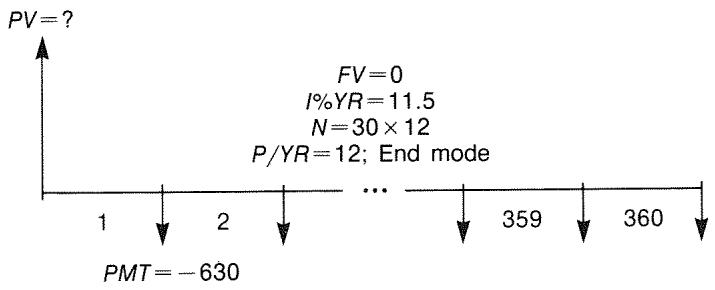

Example: A Home Mortgage. After careful consideration of your personal finances, you've decided that the maximum monthly mortgage payment you can afford is 630. You can make a12,000 down payment, and annual interest rates are currently 11.5%. If you take out a 30-year mortgage, what is the maximum purchase price you can afford?

| Keys: | Display: | Description: |

| FIN | Displays TVM menu. | |

| TVM | ||

| CLEAR DATA | 0.00 | Cleared history stack and TVM variables. |

| OTHER | If needed: sets 12 pay-ment periods per year; | |

| CLEAR DATA | End mode. | |

| EXIT | 12 P/YR END MODE | |

| 30 N | N=360.00 | Pressing first multiplies 30 by 12, then stores this number of payments in N. |

| 11.5 IZYR | IZYR=11.50 | Stores annual interest rate. |

| 630+/- | Stores a negative monthly payment. | |

| PMT | PMT=-630.00 | |

| PV | PV=63,617.64 | Calculates loan amount. |

| +12000= | 75,617.64 | Calculates total price of the house (loan plus down payment). |

Example: A Mortgage with a Balloon Payment. You've taken out a 25-year, 75,250 mortgage at13.8\%$ annual interest. You anticipate that you will own the house for four years and then sell it, repaying the loan in a "balloon payment." What will be the size of your balloon payment?

The problem is done in two steps:

- Calculate the monthly payment without the balloon (FV = 0) .

- Calculate the balloon payment after 4 years.

| Keys: | Display: | Description: |

| FIN | Displays TVM menu. | |

| TVM | ||

| CLEAR DATA | 0.00 | Cleared history stack and TVM variables. |

| OTHER | If needed: sets 12 pay-ment periods per year; | |

| CLEAR DATA | ||

| EXIT | 12 P/YR END MODE | End mode. |

Step 1. Calculate PMT for the mortgage.

| 25 | N | N=300.00 | Figures and stores the number of monthly payments in 25 years. |

| 13.8 | IXYR | IXYR=13.80 | Stores annual interest rate. |

| 75250 | PV | PV=75,250.00 | Stores amount of the loan. |

| PMT | PMT=-894.33 | Calculates monthly payment. | |

Step 2. Calculate the balloon payment after 4 years.

| 894.33 +/− PMT | PMT=-894.33 | Stores rounded PMT value for exact payment amount (no fractional cents).* |

| 4 N | N=48.00 | Figures and stores number of payments in 4 years. |

| FV | FV=-73,408.81 | Calculates balloon payment after four years. This amount plus last monthly payment repays the loan. |

Savings Calculations

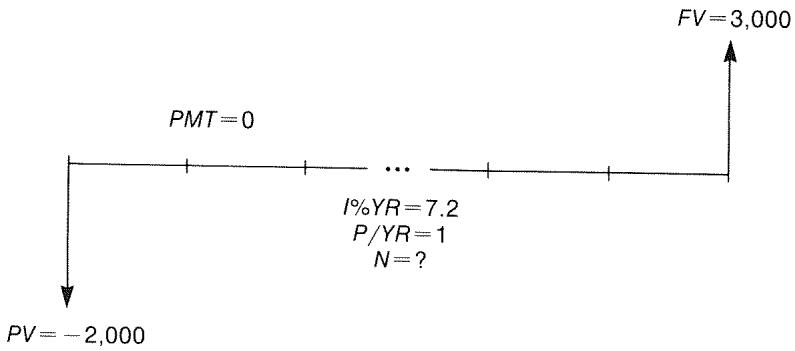

Example: A Savings Account. You deposit 2,000 into a savings account that pays 7.2% annual interest, compounded annually. If you make no other deposits into the account, how long will it take for the account to grow to3,000? Since this account has no regular payments (PMT=0), the payment mode (End or Begin) is irrelevant.

| Keys: | Display: | Description |

| FIN | Displays TVM menu. | |

| TVM | ||

| CLEAR DATA | 0.00 | Cleared history stack and TVM variables. |

| OTHER | Sets one compounding per./yr. (one interest pmt./yr). Payment mode does not matter. | |

| 1 P/YR | ||

| EXIT | 1 P/YR | |

| 7.2 IXYR | IXYR=7.20 | Stores annual interest rate. |

| 2000 +/− PV | PV=-2,000.00 | Stores amount of deposit. |

| 3000 FV | FV=3,000.00 | Stores future account balance in FV. |

| N | N=5.83 | Calculates number of compounding periods (years) for the account to reach $3,000. |

There is no conventional way to interpret results based on a non-integer value (5.83) of N . Since the calculated value of N is between 5 and 6, it will take 6 years of annual compounding to achieve a balance of at least $3,000. The actual balance at the end of 6 years can be calculated as follows:

6 N N = 6,00

Stores a whole number of years in N .

FV FV=3,035.28

Calculates account balance after six years.

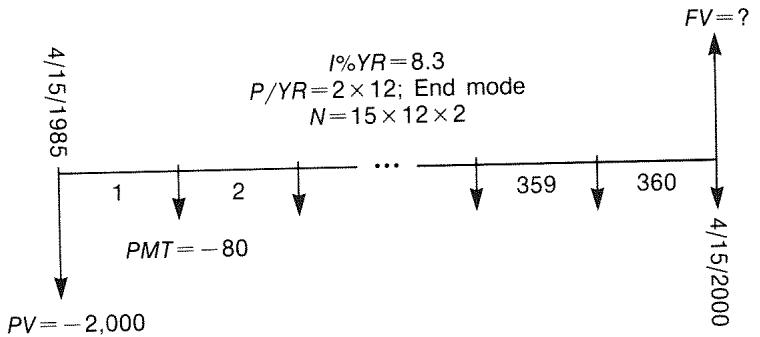

Example: An Individual Retirement Account (IRA). You opened an IRA on April 15, 1985, with a deposit of 2,000. Thereafter, you deposit 80.00 into the account at the end of each half-month. The account pays 8.3% annual interest, compounded semimonthly. How much money will the account contain on April 15, 2000?

Keys: Display:

FIN

TVM

OTHER

24 P/YR

END

EXIT

Display:

24 P/YR END MODE

Description:

Displays TVM menu. It is not necessary to clear data because you do not need to set any of the values to zero.

Sets 24 payment periods per year, End mode.

15 N N = 360,00

Figures and stores number of deposits in N

8.3 IXYR IXYR=8.30

Stores annual interest rate.

2000 + PV = -2,000.00

Stores initial deposit.

80 + PMT PMT=-80.00

Stores semimonthly payment.

FV FV=63,963.84

Calculates balance in IRA after 15 years.

Leasing Calculations

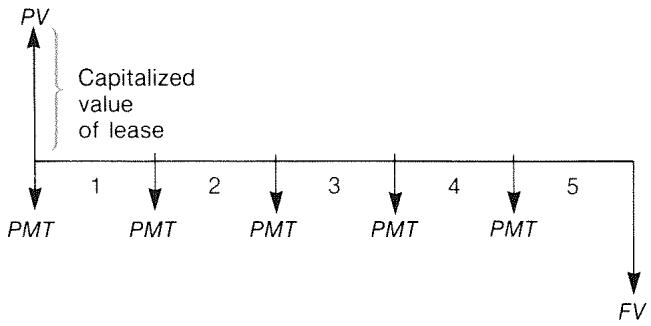

Two common leasing calculations are 1) finding the lease payment necessary to achieve a specified yield, and 2) finding the present value (capitalized value) of a lease. Leasing calculations typically use "advance payments". For the calculator, this means Begin mode because all payments will be made at the beginning of the period. If there are two payments in advance, then one payment must be combined with the present value. For examples with two or more advance payments, see pages 64 and 187.

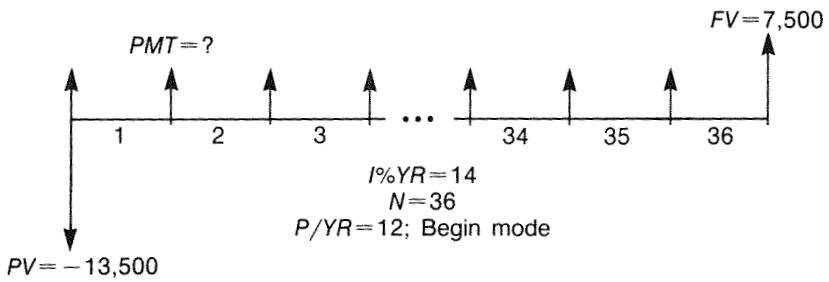

Example: Calculating a Lease Payment. A new car valued at 13,500 is to be leased for 3 years. The lessee has the option to purchase the car for 7,500 at the end of the leasing period. What monthly payments, with one payment in advance, are necessary to yield the lessor 14% annually? Calculate the payments from the lessor's point of view. Use Begin payment mode because the first payment is due at the inception of the lease.

| Keys: | Display: | Description: |

| FIN | Displays TVM menu. | |

| TVM | ||

| OTHER | Sets 12 payment periods per year, Begin mode. | |

| 12 P/YR | ||

| BEG | 12 P/YR BEGIN MODE | |

| EXIT | ||

| 36 N | N=36.00 | Stores number of payments. |

| 14 I.YR | I.YR=14.00 | Stores annual interest rate. |

| 13500+/- | Stores car's value in PV. (Money paid out by lessor.) | |

| PV | PV=-13,500.00 | |

| 7500 FV | FV=7,500.00 | Stores purchase option value in FV. (Money received by lessor.) |

| PMT | PMT=289.19 | Calculates monthly payment received. |

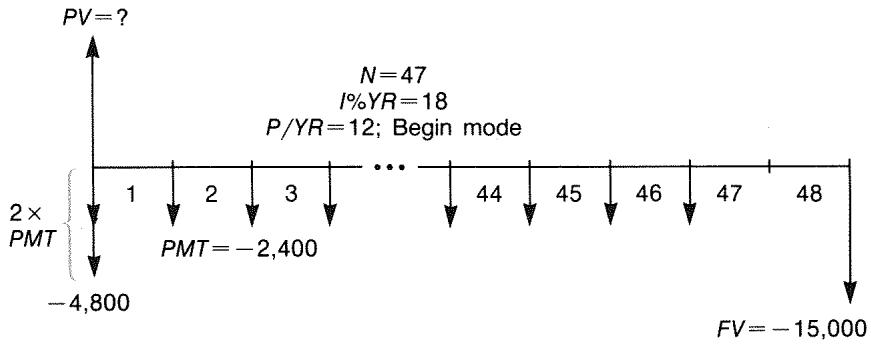

Example: Present Value of a Lease with Advance Payments and Option to Buy. Your company is leasing a machine for 4 years. Monthly payments are 2,400 with two payments in advance. You have an option to buy the machine for 15,000 at the end of the leasing period. What is the capitalized value of the lease? The interest rate you pay to borrow funds is 18%, compounded monthly.

The problem is done in four steps:

- Calculate the present value of 47 monthly payments in Begin mode. (Begin mode makes the first payment an advance payment.)

- Add one additional payment to the calculated present value. This adds a second advance payment to the beginning of the leasing period, replacing what would have been the final (48th) payment.

- Find the present value of the buy option.

- Add the present values calculated in steps 2 and 3.

| Keys: | Display: | Description: |

| FIN TVM | Displays TVM menu. | |

| CLEAR DATA | 0.00 | Cleared history stack and TVM variables. |

| OTHER | Sets 12 payment periods per year; Begin mode. | |

| 12 P/YR | ||

| BEG | ||

| EXIT | 12 P/YR BEGIN MODE |

Step 1: Find the present value of the monthly payments.

47 N N = 47,00

Stores number of payments.

18 IxYR IxYR=18.00

Stores annual interest rate.

2400 + Stores monthly payment. PMT PMT=-2,400.00

PV PV=81,735.58

Calculates present (capitalized) value of the 47 monthly payments.

Step 2: Add the additional advance payment to PV . Store the answer.

2400 84,135.58

Calculates present value of all payments.

STO 0 84,135.58

Stores result in register 0.

Step 3: Find the present value of the buy option.

48 N N = 48,00

Stores number of payment periods.

15000 FV FV=-15,000.00

Stores amount of the buy option (money paid out).

0 PMT PMT=0.00

There are no payments.

PV PV=7,340.43

Calculates present value of the buy option.

Step 4: Add the results of step 2 and 3.

+0= 91,476.00

Calculates present, capitalized value of lease.

Amortization (AMRT)

The AMRT menu (press TVM OTHER AMRT) displays or prints the following values:

The loan balance after the payment(s) are made.

The amount of the payment(s) applied toward interest.

The amount of the payment(s) applied toward principal.

Table 4-2. AMRT Menu Labels

| Menu Label | Description |

| #P | Stores the number of payments to be amortized, and calculates an amortization schedule for that many payments. Successive schedules start where the last schedule left off. #P can be an integer from 1 through 1,200. |

| INT | Displays the amount of the payments applied toward interest. |

| PRIN | Displays the amount of the payments applied toward principal. |

| BAL | Displays the balance of the loan. |

| NEXT | Calculates the next amortization schedule, which contains #P payments. The next set of payments starts where the previous set left off. |

| TABLE | Displays a menu for printing an amortization table (schedule). |

Displaying an Amortization Schedule

For amortization calculations, you need to know PV , I% YR , and PMT . If you have just finished doing these calculations with the TVM menu, then skip to step 3.

To calculate and display an amortization schedule:\*

- Press FIN TVM to display the TVM menu.

- Store the values for I% YR , PV , and PMT . (Press +/- to make PMT a negative number.) If you need to calculate one of these values, follow the instructions under "Using the TVM Menu," on page 55. Then go on to step 3.

- Press OTHER to display the rest of the TVM menu.

- If necessary, change the number of payment periods per year stored in P/YR

- If necessary, change the payment mode by pressing BEG or END. (Most loan calculations use End mode.)

- Press AMRT. (If you want to print the amortization schedule, go to page 71 to continue.)

- Key in the number of payments to be amortized at one time and press #P . For example, to see a year of monthly payments at one time, set #P to 12. To amortize the entire life of a loan at one time, set #P equal to the total number of payments (N). If #P = 12, the display would show:

Number of payments amortized at one time

Current set of payments to be amortized

Press to see results

- To display the results, press INT, PRIN, and BAL (or press to view the results from the stack).

- To continue calculating the schedule for subsequent payments, do a or b. To start the schedule over, do c.

a. To calculate the next successive amortization schedule, with the same number of payments, press NEXT.

Next successive set of payments authorized

b. To calculate a subsequent schedule with a different number of payments, key in that number and press #P

C. To start over from payment #1 (using the same loan information), press CLEAR DATA and proceed from step 7.

Example: Displaying an Amortization Schedule. To purchase your new home, you have taken out a 30-year, 65,000 mortgage at (12.5% annual interest. Your monthly payment is )693.72. Calculate the amount of the first year's and second year's payments that are applied toward principal and interest.

Then calculate the loan balance after 42 payments (31/2 years).

| Keys: | Display: | Description: |

| FIN | Displays TVM menu. | |

| TVM | ||

| 12.5 IZYR | IZYR=12.50 | Stores annual interest rate. |

| 65000 PV | PV=65,000.00 | Stores loan amount. |

| 693.72 +/- | Stores monthly payment. | |

| PMT | PMT=-693.72 | |

| OTHER | If needed: sets 12 pay-ment periods per year;End mode. | |

| CLEAR DATA | 12 P/YR END MODE | |

| AMRT | KEY #PMTS; PRESS (#P) | Displays AMRT menu. |

| 12 #P | #P=12 PMTS: 1-12 | Calculates amortization schedule for first 12 pay- ments, but does not display it. |

| INT | INTEREST=-8,113.16 | Displays interest paid in first year. |

| PRIN | PRINCIPAL=-211.48 | Displays principal paid in first year. |

| BAL | BALANCE=64,788.52 | Displays balance at end of first year. |

| NEXT | #P=12 PMTS: 13-24 | Calculates amortization schedule for next 12 payments. |

| INT | INTEREST=-8,085.15 | Displays results for sec- ond year. |

| PRIN | PRINCIPAL=-239.49 | |

| BAL | BALANCE=64,549.03 |

To calculate the balance after 42 payments (3½ years), amortize 18 additional payments (42 - 24 = 18) :

| 18 | #P | #P=18 PMTS: 25-42 | Calculates amortization schedule for next 18 months. |

| INT | INTEREST= -12,066.98 | Displays results. | |

| PRIN | PRINCIPAL=-419.98 | ||

| BAL | BALANCE=64,129.05 |

Printing an Amortization Table (TABLE)

To print an amortization schedule (or "table") do steps 1 through 5 for displaying an amortization schedule (see page 68).

- Press AMRT. Ignore the message KEY #PMTS; PRESS (#P).

- Press TABLE .

- Key in the payment number of the first payment in the schedule and press FIRST. (For instance, for the very first payment, FIRST = 1 .)

- Key in the payment number of the last payment in the schedule and press LAST.

- Key in the increment—the number of payments shown at one time—and press INCR. (For instance, for one year of monthly payments at a time, INCR=12.)

- Press Go

Values are retained until you exit the TABLE menu, so you can print successive amortization schedules by re-entering only those TABLE values that change.

Example: Printing an Amortization Schedule. For the loan described in the previous example (page 69), print an amortization table with entries for the fifth and sixth years. You can continue from the AMRT menu in the previous example (step 7, above) or repeat steps 1 through 6.

Starting from the AMRT menu:

Keys:

TABLE

Display:

PRINT AMORT TABLE

Description:

Displays menu for printing amortization table.

4 12 + 1 FIRST

FIRST=49.00

The 49th is the first payment in year 5.

6 12 LAST

LAST=72.00

The 72nd is the last payment in year 6.

Each table entry represents 12 payments (1 year).

GO

Calculates and prints amortization schedule shown below.

| I%YR= | 12.50 |

| PV= | 65,000.00 |

| PMT= | -693.72 |

| P/YR= | 12.00 |

| END MODE | |

| PMTS:49-60 | |

| INTEREST= | -7,976.87 |

| PRINCIPAL= | -347.77 |

| BALANCE= | 63,622.94 |

| PMTS:61-72 | |

| INTEREST= | -7,930.82 |

| PRINCIPAL= | -393.82 |

| BALANCE= | 63,229.12 |

Interest Rate Conversions