12C - Calculator HP - Free user manual and instructions

Find the device manual for free 12C HP in PDF.

Download the instructions for your Calculator in PDF format for free! Find your manual 12C - HP and take your electronic device back in hand. On this page are published all the documents necessary for the use of your device. 12C by HP.

USER MANUAL 12C HP

This Solutions Handbook has been designed to supplement the HP-12C Owner's Handbook by providing a variety of applications in the financial area. Programs and/or step-by-step keystroke procedures with corresponding examples in each specific topic are explained. We hope that this book will serve as a reference guide to many of your problems and will show you how to redesign our examples to fit your specific needs.

Real Estate

Refinancing

It can be mutually advantageous to both borrower and lender to refinance an existing mortgage which has an interest rate substantially below the current market rate, with a loan at a below-market rate. The borrower has the immediate use of tax-free cash, while the lender has substantially increased debt service on a relatively small cash outlay.

To find the benefits to both borrower and lender:

- Calculate the monthly payment on the existing mortgage.

- Calculate the monthly payment on the new mortgage.

- Calculate the net monthly payment received by the lender (and paid by the borrower) by adding the figure found in Step 1 to the figure found in Step 2.

- Calculate the Net Present Value (NPV) to the lender of the net cash advanced.

- Calculate the yield to the lender as an IRR.

- Calculate the NPV to the borrower of the net cash received.

Example 1: An investment property has an existing mortgage which originated 8 years ago with an original term of 25 years, fully amortized in level monthly payments at 6.5% interest. The current balance is $133,190.

Although the going current market interest rate is 11.5% , the lender has agreed to refinance the property with a 200,000, 17 year, level-monthly-payment loan at9.5\%$ interest.

What are the NPV and effective yield to the lender on the net amount of cash actually advanced?

What is the NPV to the borrower on this amount if he can earn a 15.25% equity yield rate on the net proceeds of the loan?

| Keystrokes | Display | |

| g ENDf CLEAR FIN17 g 12x6.5 g 12÷133190 PVPMT STO 0 | -1,080.33 | Monthly payment on existing mortgage received by lender. |

| 9.5 g 12÷ 200000 CHS PV PMT | 1,979.56 | Monthly payment on new mortgage. |

| RCL 0 + PMT | 899.23 | Net monthly payment (to lender). |

| RCL PV 133190 + STO 0 | -66,810.00 | Net amount of cash advanced (by lender). |

| 11.5 g 12÷ PV | -80,425.02 | Present value of net |

| RCL 0 - | -13,615.02 | NPV to lender of net cash advanced |

| RCL 0 PV i 12 x | 14.83 | % nominal yield (IRR). |

| 15.25 g 12÷ PV | -65,376.72 | Present value of net monthly payment at 15.25%. |

| RCL 0 - | 1,433.28 | NPV to borrower. |

Wrap-Around Mortgage

A wrap-around mortgage is essentially the same as a refinancing mortgage, except that the new mortgage is granted by a different lender, who assumes the payments on the existing mortgage, which remains in full force. The new (second) mortgage is thus "wrapped around" the existing mortgage. The "wrap-around" lender advances the net difference between the new (second) mortgage and the existing mortgage in cash to the borrower, and receives as net cash flow, the difference between debt service on the new (second) mortgage and debt service on the existing mortgage.

When the terms of the original mortgage and the wrap-around are the same, the procedures in calculating NPV and IRR to the lender and NPV to the borrower are exactly the same as those presented in the preceding section on refinancing.

Example 1: A mortgage loan on an income property has a remaining balance of 200,132.06 . When the load originated 8 years ago, it had a 20-year term with full amortization in level monthly payments at 6.75% interest.

A lender has agreed to "wrap" a $300,000 second mortgage at 10%, with full amortization in level monthly payments over 12 years. What is the effective yield (IRR) to the lender on the net cash advanced?

| Keystrokes | Display | |

| g END | 144.00 | Total number of months remaining in original load (into n). |

| f CLEAR FIN 20 ENTER 8 - g 12x | ||

| 6.75 g 12÷ | 0.56 | Monthly interest rate (into i). |

| 200132.06 PV | 200,132.06 | Loan amount (into PV). |

| PMT STO 0 | -2,031.55 | Monthly payment on existing mortgage (calculated). |

| 10 g 12÷ | 0.83 | Monthly interest on wrap-around. |

| 300000 CHS PV | -300,000.00 | Amount of wrap-around (into PV). |

| PMT | 3,585.23 | Monthly payment on wrap-around (calculated). |

| RCL 0 + PMT | 1,553.69 | Net monthly payment received (into PMT). |

| RCL PV 200132.06 + PV | -99,867.94 | Net cash advanced (into PV). |

| i 12 x | 15.85 | Nominal yield (IRR) to lender (calculated). |

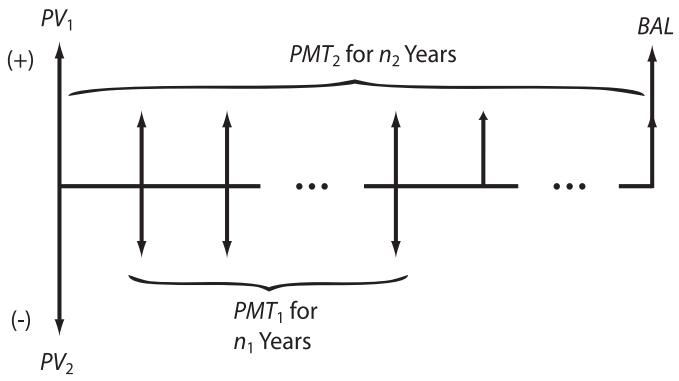

Sometimes the wrap around mortgage will have a longer payback period than the original mortgage, or a balloon payment may exist.

where:

n_1 = number of years remaining in original mortgage

PMT_1 = yearly payment of original mortgage

PV_1 = remaining balance of original mortgage

n_2 = number of years in wrap-around mortgage

PMT_2 = yearly payment of wrap-around mortgage

PV_2 = total amount of wrap-around mortgage

BAL = balloon payment

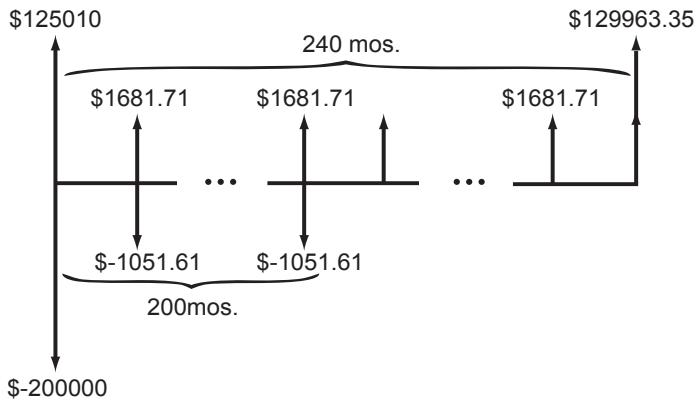

Example 2: A customer has an existing mortgage with a balance of 125.010, a remaining term of 200 months, and a1051.61 monthly payment. He wishes to obtain a 200,000, 9 1/2% wrap-around with 240 monthly payments of1681.71 and a balloon payment at the end of the 240th month of $129,963.35. If you, as a lender, accept the proposal, what is your rate of return?

| Keystrokes | Display | |

| g ENDf CLEAR FIN200000 CHS ENTER125010 + g CF0 | -74,990.00 | Net investment. |

| 1051.61 CHS ENTER1681.71 + | 630.10 | Net cash flow received by lender. |

| g CFj 99 g Njx ≈ y g CFjx ≈ y g NJx ≈ y g CFj2 g Nj | The above cash flow occurs 200 times. | |

| g LSTX g CFj | 1,681.71 | Next cash flow received by lender. |

| 39 g Nj | 39.00 | Cash flow occurs 39 times. |

| x ≈ y 129963.35 + g CFj | 131,645.06 | Final cash flow. |

| f IRR 12 x | 11.84 | Rate of return to lender. |

If you, as a lender, know the yield on the entire transaction, and you wish to obtain the payment amount on the wrap-around mortgage to achieve this yield, use the following procedure. Once the monthly payment is known, the borrower's periodic interest rate may also be determined.

- Press the g END and press f CLEAR FIN

- Key in the remaining periods of the original mortgage and press n

- Key in the desired annual yield and press g 12÷

- Key in the monthly payment to be made by the lender on the original mortgage and press CHS PMT.

- Press PV

- Key in the net amount of cash advanced and press + CHS PV

- Key in the total term of the wrap-around mortgage and press .

- If a balloon payment exists, key it in and press FV

- Press PMT to obtain the payment amount necessary to achieve the desired yield.

- Key in the amount of the wrap-around mortgage and press CHS PV i to obtain the borrower's periodic interest rate.

Example 3: Your firm has determined that the yield on a wrap-around mortgage should be 12% annually. In the previous example, what monthly payment must be received to achieve this yield on a $200,000 wrap-around? What interest rate is the borrower paying?

| Keystrokes | Display | |

| g ENDf CLEAR FIN200 n 12 g 12÷ | Number of periods and monthly interest rate. | |

| 1051.61 CHS PMTfV 74990 +CHS PV | -165,776.92 | Present value of payments plus cash advanced. |

| 240 n129963.35 FV PMT | 1,693.97 | Monthly payment received by lender |

| 2000 CHS PV i | 9.58 | Annual interest rate paid by borrower. |

12

X

Income Property Cash Flow Analysis

Before-Tax Cash Flows

The before-tax cash flows applicable to real estate analysis and problems are:

Potential Gross Income

Effective Gross Income

Net Operating Income (also called Net Income Before Recapture.)

Cash Throw-off to Equity (also called Gross Spendable Cash)

The derivation of these cash flows follows a set sequence:

- Calculate Potential Gross Income by multiplying the rent per unit times the number of units, times the number of rental payments periods per year. This gives the rental income the property would generate if it were fully occupied.

- Deduct Allowance for Vacancy and Rental Loss. This is usually expressed as a percentage. The result is Rent Collections (which is also Effective Gross Income if there is no "Other Income").

- Add "Other Income" such as receipts from concessions (laundry equipment, etc.), produced from sources other than the rental office space. This is Effective Gross Income.

- Deduct Operating Expenses. These are expenditures the landlord-investor must make, by contract or custom, to preserve the property and keep in capable of producing the gross income. The result is the Net Operating Income.

- Deduct Annual Debt Service on the mortgage. This produces Cash Throw-Off to Equity.

Thus:

Effective Gross Income =

Potential Gross Income - Vacancy Loss + Other Income.

Net Operating Income =

Effective Gross Income - Operating Expenses.

Cash Throw-Off =

Net Operating Income - Annual Dept Service.

Example: A 60-unit apartment building has rentals of 250 per unit per month. With a (5% vacancy rate, the annual operating cost is )76,855.

The property has just been financed with a $700,000 mortgage, fully amortized in a level monthly payments at 11.5% over 20 years.

a. What is the Effective Gross Income?

b. What is the Net Operating Income?

c. What is the Cash Throw-Off to Equity?

| Keystrokes | Display | |

| g ENDf CLEAR FIN60 ENTER250 x 12 x | 180,000.00 | Potential Gross Income. |

| 5 % | 9,000.00 | Vacancy Loss. |

| - | 171,000.00 | Effective Gross Income. |

| 76855 - | 94,145.00 | Net Operating Income. |

| 20 g 12x11.5 g 12÷700000 PVPMT 12 x | -89,580.09 | Annual Debt Service. |

| + | 4,564.91 | Cash Throw-Off. |

Before-Tax Reversions (Resale Proceeds)

The reversion receivable at the end of the income projection period is usually based on forecast or anticipated resale of the property at that time. The before tax reversion amount applicable to real estate analysis and problems are:

Sale Price.

Cash Proceeds of Resale.

Outstanding Mortgage Balance.

Net Cash Proceeds of Resale to Equity.

The derivation of these reversions are as follows:

- Forecast or estimate Sales Price. Deduct sales and Transaction Costs. The result is the Proceeds of Resale.

- Calculate the Outstanding Balance of the Mortgage at the end of the Income Projection Period and subtract it from Proceeds of Resale. The result is net Cash Proceeds of Resale.

Thus:

Cash Proceeds of Resale = Sales Price - Transaction Costs.

Net Cash Proceeds of Resale = Cash Proceeds of Resale - Outstanding Mortgage Balance.

Example: The apartment property in the preceding example is expected to be resold in 10 years. The anticipated resale price is (800,000. The

transaction costs are expected to be 7% of the resale price. The mortgage is the same as that indicated in the preceding example.

What will the Mortgage Balance be in 10 years?

- What are the Cash Proceeds of Resale and Net Cash Proceeds of Resale?

| Keystrokes | Display | |

| g ENDf CLEAR FIN20 g 12x | 240.00 | Mortgage term. |

| 11.5 g 12÷ | 0.96 | Mortgage rate. |

| 700000 PV | Property value. | |

| PMT | -7,465.01 | Monthly payment. |

| 10 g 12x | 120.00 | Projection period. |

| FV | -530,956.57 | Mortgage balance in 10 years. |

| 800000 ENTER | Estimated resale. | |

| 7 % | 56,000.00 | Transaction costs. |

| - | 744,000.00 | Cash Proceeds of Resale. |

| + | 213,043.43 | Net Cash Proceeds of Resale. |

After-Tax Cash Flows

The After-Tax Cash Flow (ATCF) is found for the each year by deducting the Income Tax Liability for that year from the Cash Throw Off.

where:

Taxable Income =

Net Operating Income - interest - depreciation.

Tax Liability =

Taxable Income x Marginal Tax Rate.

After Tax Cash Flow =

Cash Throw Off - Tax Liability.

The After-Tax Cash Flow for the initial and successive years may be calculated by the following HP-12C program. This program calculates the Net Operating Income using the Potential Gross Income, operational cost and vacancy rate. The Net Operating Income is readjusted each year from the growth rates in Potential Gross Income and operational costs.

The user is able to change the method of finding the depreciation from declining balance to straight line. To make the change, key in f SL at line 32 of the program in place of f DB.

| KEYSTROKES | DISPLAY |

| f P/R | |

| f CLEAR PRGM | 00- |

| 0 | 01- 0 |

| n | 02- 11 |

| STO 1 | 03- 44 1 |

| RCL 7 | 04- 45 7 |

| EEX | 05- 26 |

| 2 | 06- 2 |

| ÷ | 07- 10 |

| STO 7 | 08- 44 7 |

| 1 | 09- 1 |

| STO + 1 | 10-44 40 1 |

| 1 | 11- 1 |

| 2 | 12- 2 |

| f AMORT | 13- 42 11 |

| STO 0 | 14- 44 0 |

| RCL 5 | 15- 45 5 |

| n | 16- 11 |

| RCL i | 17- 45 12 |

| RCL 6 | 18- 45 6 |

| i | 19- 12 |

| R↓ | 20- 33 |

| STO 6 | 21- 44 6 |

| R↓ | 22- 33 |

| RCL PV | 23- 45 13 |

| RCL 4 | 24- 45 4 |

| PV | 25- 13 |

| R↓ | 26- 33 |

| STO 4 | 27- | 44 | 4 |

| R↓ | 28- | 33 | |

| g x=0 | 29- | 43 | 35 |

| g GTO 36 | 30-43, | 33 | 36 |

| RCL 1 | 31- | 45 | 1 |

| f DB | 32- | 42 | 25 |

| STO - 0 | 33-44 | 30 | 0 |

| 0 | 34- | 0 | |

| g GTO 17 | 35-43, | 33 | 17 |

| n | 36- | 11 | |

| RCL 2 | 37- | 45 | 2 |

| RCL 8 | 38- | 45 | 8 |

| % | 39- | 25 | |

| STO + 2 | 40-44 | 40 | 2 |

| R↓ | 41- | 33 | |

| RCL 0 | 42-45 | 48 | 0 |

| % | 43- | 25 | |

| - | 44- | 30 | |

| RCL 3 | 45- | 45 | 3 |

| RCL 9 | 46- | 45 | 9 |

| % | 47- | 25 | |

| STO + 3 | 48-44 | 40 | 3 |

| R↓ | 49- | 33 | |

| - | 50- | 30 | |

| 1 | 51- | 1 | |

| RCL 7 | 52- | 45 | 7 |

| STO x 0 | 53-44 | 20 | 0 |

| - | 54- | 30 |

| x | 55- | 20 |

| RCL PMT | 56- 45 | 14 |

| 1 | 57- | 1 |

| 2 | 58- | 2 |

| x | 59- | 20 |

| + | 60- | 40 |

| RCL 0 | 61- 45 | 0 |

| - | 62- | 30 |

| RCL 1 | 63- 45 | 1 |

| g PSE | 64- 43 | 31 |

| x≥y | 65- | 34 |

| R/S | 66- | 31 |

| g GTO 09 | 67-43, 33 | 09 |

| f P/R | ||

| REGISTERS | ||

| n: Used | i: Annual % | |

| PV: Used | PMT: Monthly | |

| FV: 0 | R0: Used | |

| R1: Counter | R2: PGI | |

| R3: Oper. cost | R4: Dep. value | |

| R5: Dep. life | R6: Factor (DB) | |

| R7: Tax Rate | R8: % gr. (PGI) | |

| R9: % gr. (op) | R.0: Vacancy rt. | |

- Press g END and press f CLEAR REG

- Key in loan values:

Key in annual interest rate and press 12÷

Key in principal to be paid and press PV

Key in monthly payment and press CHS PMT (If any of the values are not known, they should be solved for.)

- Key in Potential Gross Income (PGI) and press STO 2.

-

Key in Operational cost and press STO 3.

-

Key in depreciable value and press STO 4.

- Key in depreciable life and press STO 5.

- Key in factor (for declining balance only) and press STO 6.

- Key in the Marginal Tax Rate (as a percentage) and press STO 7.

- Key in the growth rate in Potential Gross Income ( 0 for no growth) and pressSTO8.

- Key in the growth rate in operational cost (0 if no growth) and press STO 9.

- Key in the vacancy rate (0 for no vacancy rate) and press STO 0.

- Key in the desired depreciation function at line 32 in the program.

- Press R/S to compute ATCF. The display will pause showing the year and then will stop with the ATCF for that year. The Y-register contains the year.

- Continue pressing R/S to compute successive After-Tax Cash Flows.

Example 1: A triplex was recently purchased for (100,000 with a 30-year loan at (12.25\%) and a (20\%) down payment. Not including a (5\%) annual vacancy rate, the potential gross income is (\9,900) with an annual growth rate of (6%). Operating expenses are (\ 3,291.75) with a (2.5\%) growth rate. The depreciable value is (\75,000) with a projected useful life of (\ 20) years. Assuming a (125\%) declining balance depreciation, what are the After-Tax Cash Flows for the first 10 years if the investors Marginal Tax Rate is (35\%)?

| Keystrokes | Display | |

| g ENDf CLEAR FIN100000 ENTER20 % - PV | 80,000.00 | Mortgage amount. |

| 12.25 g 12÷ | 1.02 | Monthly interest rate. |

| 30 g 12x | 360 | Mortgage term. |

| PMT | -838.32 | Monthly payment. |

| 9900 STO 2 | 9,900.00 | Potential Gross Income. |

| 3291.75 STO 3 | 3,291.75 | 1st year operating cost. |

| 75000 STO 4 | 75,000.00 | Depreciable value. |

| 20 STO 5 | 20.00 | Useful life. |

| 125 STO 6 | 125.00 | Decline in balance factor. |

| 35 STO 7 | 35.00 | Marginal Tax Rate. |

| 6 STO 8 | 6.00 | Potential Gross Income growth rate. |

| 2.5 STO 9 | 2.50 | Operating cost growth. |

| 5 STO .0 | 5.00 | Vacancy rate. |

| R/S | 1.00 | Year 1 |

| -1,020.88 | ATCF1 | |

| R/S | 2.00 | Year 2 |

| -822.59 | ATCF2 | |

| R/S | 3.00 | Year 3 |

| -598.85 | ATCF3 | |

| R/S | 4.00 | Year 4 |

| -72.16 | ATCF4 | |

| R/S | 5.00 | Year 5 |

| 232.35 | ATCF5 | |

| R/S | 6.00 | Year 6 |

| 565.48 | ATCF6 | |

| R/S | 7.00 | Year 7 |

| 928.23 | ATCF7 | |

| R/S | 8.00 | Year 8 |

| 1,321.62 | ATCF8 | |

| R/S | 9.00 | Year 9 |

| 1,746.81 | ATCF9 | |

| R/S | 10.00 | Year 10 |

| -1,020.88 | ATCF10 |

Example 2: An office building was purchased for 1,400,000. The value of depreciable improvements is 1,200,000.00 with a 35 year economic life. Straight line depreciation will be used. The property is financed with a 1,050,000 loan. The terms of the loan are 9.5% interest and9,173.81 monthly payments for 25 years. The office building generates a Potential Gross Income of 175,2000 which grows at a 3.5% annual rate. The operating cost is40,296.00 with a 1.6% annual growth rate. Assuming a Marginal Tax Rate of 50% and a vacancy rate of 7%, what are the After-Tax Cash Flows for the first 5 years?

| Keystrokes | Display | |

| g ENDf CLEAR REG1050000 PV9173.81 CHS PMT9.5 g 12÷ | 175,200.00 | Potential Gross Income. |

| 25 12x 175200 STO 2 | ||

| 40296 STO 3 | 40,296.00 | 1st year operating cost. |

| 1200000 STO 4 | 1,200,000.00 | Depreciable value. |

| 35 STO 5 | 35.00 | Depreciable life. |

| 50 STO 7 | 50.00 | Marginal tax rate. |

| 3.5 STO 8 | 3.50 | Potential Gross Income |

| 1.6 STO 9 | 1.60 | Operating cost growth rate. |

| 7 STO 0 | 7.00 | Vacancy rate. |

| g GTO 31 | 7.00 | Go to dep. step. |

| f P/R f SL | 32-42 23 | Change to SL. |

| f P/R R/S | 1.00 18,021.07 | Year 1 ATCF1 |

| R/S | 2.00 20,014.26 | Year 2 ATCF2 |

| R/S | 3.00 22,048.90 | Year 3 ATCF3 |

| R/S | 4.00 24,123.14 | Year 4 ATCF4 |

| R/S | 5.00 26,234.69 | Year 5 ATCF5 |

After-Tax Net Cash Proceeds of Resale

The After-Tax Net Cash Proceeds of Resale (ATNCPR) is the after-tax reversion to equity; generally, the estimated resale price of the property less commissions, outstanding debt and any tax claim.

The After-Tax Net Cash Proceeds can be found using the HP-12C program which follows. In calculating the owner's income tax liability on resale, this program assumes that the owner elects to have his capital gain taxed at 40% of his Marginal Tax Rate. This assumption is in accordance with a 1978 Federal tax ruling. (Federal Taxes, code sec. 1202 (32,036))

This program uses declining balance depreciation to find the amount of depreciation from purchase to sale. This amount is used to determine the excess depreciation (which is equal to the amount of actual depreciation minus the amount of the straight line depreciation).

The user may change to a different depreciation method by keying in the desired function at line 35 in place of f DE.

| KEYSTROKES | DISPLAY |

| f P/R | |

| f CLEAR PRGM | 00- |

| g END | 01- 43 8 |

| STO 2 | 02- 44 2 |

| R↓ | 03- 33 |

| % | 04- 25 |

| - | 05- 30 |

| STO | 06- 44 0 |

| - | 07- 30 |

| · | 08- 48 |

| 4 | 09- 4 |

| x | 10- 20 |

| STO 1 | 11- 44 1 |

| RCL PMT | 12- 45 14 |

| f RND | 13- 42 14 |

| PMT | 14- 14 |

| RCL 2 | 15- 45 2 |

| g 12x | 16- 43 11 |

| FV | 17- 15 |

| STO + 0 | 18-44 40 0 |

| f CLEAR FIN | 19- 42 34 |

| RCL 3 | 20- 45 3 |

| PV | 21- 13 |

| RCL 4 | 22- 45 4 |

| n | 23- 11 |

| RCL 5 | 24- 45 5 |

| i | 25- | 12 |

| RCL 2 | 26- | 45 2 |

| f SL | 27- | 42 23 |

| RCL 2 | 28- | 45 2 |

| x | 29- | 20 |

| · | 30- | 48 |

| 6 | 31- | 6 |

| x | 32- | 20 |

| STO + 1 | 33-44 | 40 1 |

| RCL 2 | 34- | 45 2 |

| f DB | 35- | 42 25 |

| x≥y | 36- | 34 |

| RCL PV | 37- | 45 13 |

| - | 38- | 30 |

| STO + 1 | 39-44 | 40 1 |

| RCL 6 | 40- | 45 6 |

| EEX | 41- | 26 |

| 2 | 42- | 2 |

| ÷ | 43- | 10 |

| RCL 1 | 44- | 45 1 |

| x | 45- | 20 |

| RCL 0 | 46- | 45 0 |

| + | 47- | 40 |

| g GTO 00 | 48-43 | 33 00 |

| f P/R | ||

| REGISTER | ||

| n: Used | i: Used | |

| PV: Used | PMT: Used | |

| FV: Used | R0: Used | |

| R1: Used | R2: Desired yr. | |

| R3: Dep. value | R4: Dep. life | |

| R5: Factor | R6: MTR | |

| R7-R3: Unused | ||

- Key in the program and press f CLEAR REG

- Key in the loan values:

Key in annual interest rate and press g 12÷

Key in mortgage amount and press PV.

Key in monthly payment and press CHS PMT. (If any of the values are unknown, they should be solved for.)

- Key in depreciable value and press STO 3.

- Key in depreciable life in years and press STO 4.

- Key in accelerated depreciation factor for the declining balance method and press STO 5.

- Key in your Marginal Tax Rate as a percentage and press STO 6.

- Key in the purchase price and press ENTER

- Key in the sale price and press ENTER

- Key in the % commission charged on the sale and press ENTER* *If a dollar value is desired instead of a commission rate, key in g END, which does not affect the register values, at line 04 of the program.

- Key in the number of years after purchase and press R/S

Example 1: An apartment complex, purchased for 900,000 ten years ago, is sold for 1,750,000. The closing cost are 8% of the sale price and the income tax rate is 48%.

A (700,000 loan for 20 years at (9.5\%) annual interest was used to purchase the complex. When it was purchased the depreciable value was (\$ 750,000)with a useful life of 25 years. Using (125\%) declining balance depreciation, what are the After- Tax Net Cash Proceeds in year 10?

| Keystrokes | Display | |

| g END f CLEAR REG | 0.00 | |

| 700000 PV | 700,000.00 | Mortgage. |

| 9.5 g 12÷ | 0.79 | Monthly interest. |

| 20 g 12x | 240.00 | Number of payments. |

| PMT | -6,524.92 | Monthly payment. |

| 750000 STO 3 | 750,000.00 | Depreciable value. |

| 25 STO 4 | 25.00 | Depreciable life. |

| 125 STO 5 | 125.00 | Factor. |

| 48 STO 6 | 48.00 | Marginal Tax Rate. |

| 900000 ENTER | 900,000.00 | Purchase price. |

| 1750000 ENTER | 1,750,000.00 | Sale price. |

| 8 ENTER | 8.00 | Commission rate. |

| 10 R/S | 911,372.04 | ATNCPR. |

Lending

Loan With a Constant Amount Paid Towards Principal

This type of loan is structured such that the principal is repaid in equal installments with the interest paid in addition. Therefor each periodic payment has a constant amount applied toward the principle and a varying amount of interest.

Loan Reduction Schedule

If the constant periodic payment to principal, annual interest rate, and loan amount are known, the total payment, interest portion of each payment, and remaining balance after each successive payment may be calculated as follows:

- Key in the constant periodic payment to principal and press STO 0.

- Key in periodic interest rate and press ENTER ENTER ENTER

- Key in the loan amount. If you wish to skip to another time period, press ENTER. Then key in the number of payments to be skipped, and press RCL 0 x -

- Press ≥ y to obtain the interest portion of the payment.

- Press RCL 0 + to obtain the total payment.

- Press CLX RCL 0 to obtain the remaining balance of the loan.

- Return to step 4 for each successive payment.

Example 1: A (60,000 land loan at (10 \%)interest calls for equal semi- annual principal payments over a 6- year maturity. What is the loan reduction schedule for the first year? (Constant payment to principal is (\$ 5000)semi- annually). What is the fourth year's schedule (skip 4 payments)?

| Keystrokes | Display | |

| 5000 STO 0 10 ENTER 2 ÷ ENTER ENTER ENTER | 5.00 | Semi-annual interest rate. |

| 60000 x ≥ y % | 3,000.00 | First payment's interest. |

| RCL 0 + | 8,000.00 | Total first payment. |

| CLX RCL 0 - | 55,000.00 | Remaining balance. |

| x≥y % | 2,750.00 | Second payment's interest. |

| RCL 0 + | 7,750.00 | Total second payment. |

| CLX RCL 0 - | 50,000.00 | Remaining balance after the first year. |

| 4 RCL 0 x - | 1,500.00 | Seventh payment's interest. |

| x≥y % | ||

| RCL 0 + | 6,500.00 | Total seventh payment. |

| CLX RCL 0 - | 25,000.00 | Remaining balance. |

| x≥y % | 1,250.00 | Eighth payment's interest. |

| RCL 0 + | 6,250.00 | Total eighth payment. |

| CLX RCL 0 - | 20,000.00 | Remaining balance after fourth year. |

Add-On Interest Rate Converted to APR

An add-on interest rate determines what portion of the principal will be added on for repayment of a loan. This sum is then divided by the number of months in a loan to determine the monthly payment. For example, a 10% add-on rate for 36 months on 3000 means add one-tenth of3000 for 3 years (300 x 3) - usually called the "finance charge" - for a total of 3900. The monthly payment is3900/36.

This keystroke procedure converts an add-on interest rate to a annual percentage rate when the add-on rate and number of months are known.

- Press g END and press f CLEAR FIN

- Key in the number of months in loan and press n ENTER RCL g 12x

- Key in the add-on rate and press .

- Key in the amount of the loan and press PV * ( *Positive for cash received; negative for cash paid out.) x y % +

- Press x ≥ y ÷ CHS PMT

- Press 12 to obtain the APR.

Example 1: Calculate the APR and monthly payment of a 12 % 1000 add- on loan which has a life of 18 months.

| Keystrokes | Display | |

| g ENDf CLEAR FIN18 n ENTERRCL g 12x 12x1000 PV x y % + | 1,180.00 | Amount of loan. |

| x y ÷ CHS PMT | -65.56 | Monthly payment. |

| i 12 x | 21.64 | Annual Percentage Rate. |

APR Converted to Add-On Interest Rate.

Given the number of months and annual percentage rate, this procedure calculates the corresponding add-on interest rate.

- Press g END and press f CLEAR FIN

- Enter the following information:

a. Key in number of months of loan and press n

b. Key in APR and press 12÷

c. Key in 100 and press PV PMT

- Press RCL PV RCL n ++++ CHS 12 x to obtain the add-on rate.

Example 1: What is the equivalent add-on rate for an 18 month loan with an APR of 14% .

| Keystrokes | Display | |

| g ENDf CLEAR FIN18 n 14 g 12÷100 PV PMT RCL PVRCL n ÷ + CHS12 x | 7.63 | Add-On Interest Rate. |

Add-On Rate Loan with Credit Life.

This HP-12C program calculates the monthly payment amount, credit life amount (an optional insurance which cancels any remaining indebtedness at the death of the borrower), total finance charge, and annual percentage rate (APR) for an add-on interest rate (AIR) loan. The monthly payment is rounded (in normal manner) to the nearest cent. If other rounding techniques are used, slightly different results may occur.

| KEYSTROKES | DISPLAY | ||

| f | P/R | ||

| f | CLEAR PRGM | 00- | |

| g | END | 01- 43 8 | |

| 1 | 02- 1 | ||

| RCL0 | 03- 45 0 | ||

| 1 | 04- 1 | ||

| 2 | 05- 2 | ||

| 0 | 06- 0 | ||

| 0 | 07- 0 | ||

| ÷ | 08- 10 | ||

| STO4 | 09- 44 4 | ||

| RCL2 | 10- 45 2 | ||

| x | 11- 20 | ||

| - | 12- 30 | ||

| g | LSTX | 13- 43 36 | |

| RCL1 | 14- 45 1 | ||

| x | 15- 20 | ||

| RCL4 | 16- 45 4 | ||

| x | 17- 20 | ||

| - | 18- 30 | ||

| RCL4 | 19- 45 4 | ||

| RCL1 | 20- 45 1 | ||

| x | 21- 20 | ||

| 1 | 22- | 1 | |

| + | 23- | 40 | |

| x≥y | 24- | 34 | |

| ÷ | 25- | 10 | |

| RCL 3 | 26- | 45 3 | |

| x | 27- | 20 | |

| RCL 0 | 28- | 45 0 | |

| ÷ | 29- | 10 | |

| f RND | 30- | 42 14 | |

| CHS | 31- | 16 | |

| PMT | 32- | 14 | |

| R/S | 33- | 31 | |

| RCL PMT | 34- | 45 14 | |

| RCL 0 | 35- | 45 0 | |

| x | 36- | 20 | |

| CHS | 37- | 16 | |

| PV | 38- | 13 | |

| RCL PV | 39- | 45 13 | |

| RCL 2 | 40- | 45 2 | |

| % | 41- | 25 | |

| RCL 0 | 42- | 45 0 | |

| x | 43- | 20 | |

| 1 | 44- | 1 | |

| 2 | 45- | 2 | |

| ÷ | 46- | 10 | |

| STO 5 | 47- | 44 5 | |

| EEX | 48- | 26 | |

| 2 | 49- | 2 | |

| x | 50- | 20 | |

| g FRAC | 51- 43 35 |

| g x=0 | 52- 43 35 |

| g GTO 61 | 53-43, 33 61 |

| RCL 5 | 54- 45 5 |

| · | 55- 48 |

| 0 | 56- 0 |

| 1 | 57- 1 |

| + | 58- 40 |

| f RND | 59- 42 14 |

| STO 5 | 60- 44 5 |

| RCL 5 | 61- 45 5 |

| R/S | 62- 31 |

| RCL PV | 63- 45 13 |

| x y | 64- 34 |

| - | 65- 30 |

| RCL 3 | 66- 45 3 |

| - | 67- 30 |

| CHS | 68- 16 |

| R/S | 69- 31 |

| RCL 5 | 70- 45 5 |

| RCL 3 | 71- 45 3 |

| + | 72- 40 |

| + | 73- 13 |

| RCL 0 | 74- 45 0 |

| n | 75- 11 |

| i | 76- 12 |

| RCL g 12÷ | 77-45, 43 12 |

| g GTO 00 | 78-43, 33 00 |

| f P/R | |

| REGISTER | |

| n: N | i: i |

| PV: Used | PMT: PMT |

| FV: 0 | R0: N |

| R1: AIR | R2: CL (%) |

| R3: Loan | R4: N/1200 |

| R5: Used | R6-R9: Unused |

- Key in the program.

- Press f CLEAR FIN

- Key in the number of monthly payments in the loan and press STO 0.

- Key in the annual add-on interest rate as a percentage and press STO 1.

- Key in the credit life as a percentage and press STO 2.

- Key in the loan amount and press STO 3.

- Press R/S to find the monthly payment amount.

- Press R/S to obtain the amount of credit life.

- Press / to calculate the total finance charge.

- Press R/S to calculate the annual percentage rate.

- For a new loan return to step 3.

Example 1: You wish to quote a loan on a (3100 balance, payable over 36 months at an add-on rate of (6.75\%). Credit life (CL) is (1\%). What are the monthly payment amount, credit life amount, total finance charge, and APR?

| Keystrokes | Display | |

| f CLEAR FIN 36 STO 0 | 36.00 | Months. |

| 6.75 STO 1 | 6.75 | Add-on interest rate. |

| 1 STO 2 | 1.00 | Credit life (%). |

| 3100 STO 3 | 3100.00 | Loan. |

| R/S | -107.42 | Monthly payment. |

| R/S | 116.02 | Credit life. |

| R/S | -651.10 | Total finance charge. |

| R/S | 12.39 | APR. |

Interest Rebate - Rule of 78's

This procedure finds the unearned interest rebate, as well as the remaining principal balance due for a prepaid consumer loan using the Rule of 78's. The known values are the current installment number, the total number of installments for which the loan was written, and the total finance charge (amount of interest). The information is entered as follows:

- Key in number of months in the loan and press STO 1.

- Key in payment number when prepayment occurs and press STO 2 1

- Key in total finance charge and press RCL 1 ENTER RCL 1 + ÷ RCL 2 to obtain the unearned interest (rebate).

- Key in periodic payment amount and press RCL 2 x x y - to obtain the amount of principal outstanding.

Example 1: A 30 month 1000 loan having a finance charge of 180, is being repaid at $39.33 per month. What is the rebate and balance due after the 25th regular payment?

| Keystrokes | Display | |

| 30 STO 125 - STO 21 + 180 xRCL 1 ENTERx RCL 1 +÷ RCL 2 x | 5.81 | Rebate. |

| 39.33 RCL 2 xx≥y - | 190.84 | Outstanding principal. |

The following HP-12C program can be used to evaluate the previous example.

| KEYSTROKES | DISPLAY |

| f P/R | |

| f CLEAR PRGM | 00- |

| STO 0 | 01- 44 0 |

| R↓ | 02- 33 |

| STO 2 | 03- 44 2 |

| R↓ | 04- 33 |

| STO 1 | 05- 44 1 |

| RCL 2 | 06- 45 2 |

| - | 07- 30 |

| STO 2 | 08- 44 2 |

| 1 | 09- 1 |

| + | 10- 40 |

| RCL 0 | 11- 45 0 |

| x | 12- 20 |

| RCL 1 | 13- 45 1 |

| ENTER | 14- 36 |

| x | 15- 20 |

| RCL 1 | 16- 45 1 |

| + | 17- 40 |

| ÷ | 18- 10 |

| RCL 2 | 19- 45 2 |

| x | 20- 20 |

| R/S | 21- 31 |

| RCL 2 | 22- 45 2 |

| x | 23- 20 |

| x≥y | 24- 34 |

| - | 25- 30 |

| g GTO 00 | 26-43, 33 00 |

| f P/R | |

| REGISTER | |

| n: Unused | i: Unused |

| PV: Unused | PMT: Unused |

| FV: Unused | R0: Fin. charge |

| R1: Payment# | R2: # moths |

| R3-R6: Unused | |

- Key in the program.

- Key in the number of months in the loan and press ENTER

- Key in the payment number when prepayment occurs and press ENTER

- Key in the total finance charge and press R/S to obtain the unearned interest (rebate).

- Key in the periodic payment amount and press R/S to find the amount of principal outstanding.

- For a new case return to step 2.

| Keystrokes | Display | |

| 30 ENTER | 5.81 | Rebate. |

| 25 ENTER | ||

| 180 R/S | ||

| 39.33 R/S | 190.84 | Outstanding principal. |

Graduated Payment Mortgages

The Graduated Payment Mortgage is designed to meet the needs of young home buyers who currently cannot afford high mortgage payments, but who have the potential of increasing earning in the years on come.

Under the Graduated Payment Mortgage plan, the payments increase by a fixed percentage at the end of each year for a specified number of years. Thereafter, the payment amount remains constant for remaining life of the mortgage.

The result is that the borrower pays a reduced payment (a payment which is less than a traditional mortgage payment) in the early years, and in the later years makes larger payments than he would with a traditional loan. Over the entire term of the mortgage, the borrower would pay more than he would with conventional financing.

Given the term of the mortgage (in years), the annual percentage rate, the loan amount, the percentage that the payments increase, and the number of years that the payments increase, the following HP-12C program determines the monthly payments and remaining balance for each year until the level payment is reached.

| KEYSTROKES | DISPLAY | |||

| f | P/R | |||

| f | CLEAR PRGM | 00- | ||

| g | END | 01- | 43 8 | |

| STO 2 | 02- | 44 2 | ||

| x≥y | 03- | 34 | ||

| 1 | 04- | 1 | ||

| % | 05- | 25 | ||

| 1 | 06- | 1 | ||

| + | 07- | 40 | ||

| STO 0 | 08- | 44 0 | ||

| RCL n | 09- | 45 11 | ||

| RCL 2 | 10- | 45 2 | ||

| - | 11- | 30 | ||

| g | 12x | 12- | 43 11 | |

| RCL i | 13- | 45 12 | ||

| g | 12÷ | 14- | 43 12 | |

| RCL PV | 15- | 45 13 | ||

| STO 3 | 16- | 44 3 | ||

| 1 | 17- | 1 | ||

| CHS | 18- | 16 | ||

| PMT | 19- | 14 | ||

| PV | 20- | 13 | ||

| CHS | 21- | 16 | ||

| FV | 22- | 15 | ||

| 1 | 23- | 1 | ||

| g | 12x | 24- | 43 11 | |

| RCL PMT | 25- | 45 14 | ||

| RCL 0 | 26- | 45 0 | ||

| ÷ | 27- | 10 | ||

| PMT | 28- | 14 | ||

| PV | 29- | 13 | ||

| CHS | 30- | 16 | ||

| FV | 31- | 15 | ||

| 1 | 32- | 1 | ||

| STO + 1 | 33- | 1 | ||

| RCL 1 | 34-44 | 40 1 | ||

| RCL 2 | 35- | 45 2 | ||

| - | 36- | 30 | ||

| g x=0 | 37- | 43 35 | ||

| g GTO 40 | 38-43, | 33 40 | ||

| g GTO 25 | 39-43, | 33 25 | ||

| RCL 3 | 40- | 45 3 | ||

| RCL PV | 41- | 45 13 | ||

| ÷ | 42- | 10 | ||

| STO 4 | 43- | 44 4 | ||

| RCL 3 | 44- | 45 3 | ||

| PV | 45- | 13 | ||

| 1 | 46- | 1 | ||

| STO 3 | 47- | 44 3 | ||

| RCL 3 | 48- | 45 3 | ||

| R/S | 49- | 31 | ||

| RCL 4 | 50- | 45 4 | ||

| 1 | 51- | 1 | ||

| RCL 0 | 52- | 45 0 | ||

| RCL 1 | 53- | 45 1 | ||

| yx | 54- | 21 | ||

| ÷ | 55- | 10 | ||

| x | 56- | 20 | ||

| CHS | 57- | 16 | ||

| f RND | 58- 42 | 14 | ||

| PMT | 59- | 14 | ||

| R/S | 60- | 31 | ||

| FV | 61- | 15 | ||

| FV | 62- | 15 | ||

| f RND | 63- 42 | 14 | ||

| R/S | 64- | 31 | ||

| CHS | 65- | 16 | ||

| PV | 66- | 13 | ||

| 1 | 67- | 1 | ||

| STO + 3 | 68-44 40 | 3 | ||

| STO - 1 | 69-44 30 | 1 | ||

| RCL 1 | 70- 45 | 1 | ||

| g x=0 | 71- 43 | 35 | ||

| g GTO 74 | 72-43, 33 | 74 | ||

| g GTO 48 | 73-43, 33 | 48 | ||

| RCL 4 | 74- 45 | 4 | ||

| CHS | 75- | 16 | ||

| R/S | 76- | 31 | ||

| g GTO 76 | 77-43, 33 | 76 | ||

| f P/R | ||||

| REGISTERS | ||||

| n: Used | i: i/12 | |||

| PV: Used | PMT: Used | |||

| FV: Used | R0: Used | |||

| R1: Used | R2: Used | |||

| R3: Used | R4: Level Pmt. | |||

| R5-R9: Unused | ||||

-

Key in the program.

-

Press CLEAR REG

- Key in the term of the loan and press n

- Key in the annual interest rate and press i

- Key in the total loan amount and press PV

- Key in the rate of graduation (as a percent) and press ENTER

- Key in the number of years for which the loan graduates and press R/S. The following information will be displayed for each year until a level payment is reached.

a. The current year.

Then press R/S to continue.

b. The monthly payment for the current year.

Then press R/S to continue.

c. The remaining balance to be paid on the loan at the end of the current year. Then press R/S to return to step a. unless the level payment is reached. If the level payment has been reached, the program will stop, displaying the monthly payment over the remaining term of the loan.

- For a new case press GTO 00 and return to step 2.

Example: A young couple recently purchased a new house with a Graduated Payment Mortgage. The loan is for (50,000 over a period of 30 years at an annual interest rate of (12.5\%). The monthly payments will be graduating at an annual rate of (5\%) for the first 5 years and then will be level for the remaining 25 years. What are the monthly payment amount for the first 6 years?

| Keystrokes | Display | |

| f CLEAR REG | 0.00 | |

| 30 n | 30.00 | Term |

| 12.5 i | 12.50 | Annual interest rate |

| 50000 PV | 50,000.00 | Loan amount |

| 5 ENTER | 5.00 | Rate of graduation |

| 5 R/S | 1.00 | Year 1 |

| R/S | -448.88 | 1st year monthly payment. |

| R/S | -50,194.67 | Remaining balance after 1st year. |

| R/S | 2.00 | Year 2 |

| R/S | -471.33 | 2nd year monthly payment. | |

| R/S | -51,665.07 | Remaining balance after 2nd year. | |

| R/S | 3.00 | Year 3 | |

| R/S | -494.89 | 3rd year monthly payment. | |

| R/S | -52,215.34 | Remaining balance after 3rd year. | |

| R/S | 4.00 | Year 4 | |

| R/S | -519.64 | 4th year monthly payment. | |

| R/S | -52.523.34 | Remaining balance after 4th year. | |

| R/S | 5.00 | Year 5 | |

| R/S | -545.62 | 5th year monthly payment. | |

| R/S | -52,542.97 | Remaining balance after 5th year. | |

| R/S | -572.90 | Monthly payment for remainder of term. |

Variable Rate Mortgages

As its name suggests, a variable rate mortgage is a mortgage loan which provides for adjustment of its interest rate as market interest rates change. As a result, the current interest rate on a variable rate mortgage may differ from its origination rate (i.e., the rate when the loan was made). This is the difference between a variable rate mortgage and the standard fixed payment mortgage, where the interest rate and the monthly payment are constant throughout the term.

Under the agreement of the variable rate mortgage, the mortgage is examined periodically to determine any rate adjustments. The rate adjustment may be implemented in two ways:

- Adjusting the monthly payment.

- Modifying the term of the mortgage.

The period and limits to interest rate increases vary from state to state. Each periodic adjustment may be calculated by using the HP-12C with the following keystroke procedure. The original terms of the mortgage are assumed to be known.

-

Press g END and press f CLEAR FIN

-

Key in the remaining balance of the loan and press . The remaining balance is the difference between the loan amount and the total principal from the payments which have been made.

To calculate the remaining balance, do the following:

a. Key in the previous remaining balance. If this is the first mortgage adjustment, this value is the original amount of the loan. Press PV.

b. Key in the annual interest rate before the adjustment (as a percentage) and press g 12÷

c. Key in the number of years since the last adjustment. If this is the first mortgage adjustment, then key in the number of years since the origination of the mortgage. Press 12x .

d. Key in the monthly payment over this period and press CHS PMT

e. Press FV to find the remaining balance, then press f CLEAR FIN CHS PV

- Key in the adjusted annual interest rate (as a percentage) and press g 12÷ . To calculate the new monthly payment:

a. Key in the remaining life of the mortgage (years) and press g 12x

b. Press PMT to find the new monthly payment.

To calculate the revised remaining term of the mortgage:

c. Key in the present monthly payment and press PMT.

d. Press 12 ÷ to find the remaining term of the mortgage in years.

Example: A homeowner purchased his house 3 years ago with a 50,000 variable rate mortgage. With a 30-year term, his current monthly payment is 495.15. When the interest rate is adjusted from 11.5% to 11.75%, what will the monthly payment be? If the monthly payment remained unchanged, find the revised remaining term on the mortgage.

| Keystrokes | Display | |

| g END f CLEAR FIN 50000 PV | 50,000.00 | Original amount of loan. |

| 11.5 g 12÷ | 0.96 | Original monthly interest rate. |

| 3 g 12x | 36.00 | Period. |

| 495.15 CHS PMT | -495.15 | Previous monthly payment. |

| FV | -49,316.74 | |

| f CLEAR FIN CHS PV | 49,316.74 | Remaining balance. |

| 11.75 g 12÷ | 0.98 | Adjusted monthly interest. |

| 30 ENTER 3 - | 27.00 | Remaining life of mortgage. |

| g 12x | 324.00 | |

| PMT | -504.35 | New monthly payment. |

| 495.15 CHS PMT | -495.15 | Previous monthly payment. |

| n 12 ÷ | 31.67 | New remaining term (years). |

Skipped Payments

Sometimes a loan (or lease) may be negotiated in which a specific set of monthly payments are going to be skipped each year. Seasonally is usually the reason for such an agreement. For example, because of heavy rainfall, a bulldozer cannot be operated in Oregon during December, January, and February, and the lessee wishes to make payments only when his machinery is being used. He will make nine payments per year, but the interest will continue to accumulate over the months in which a payment is not made.

To find the monthly payment amount necessary to amortize the loan in the specified amount of time, information is entered as follows:

- Press g END and press f CLEAR FIN

- Key in the number of the last payment period before payments close the first time and press n.

- Key in the annual interest rate as a percentage and press g 12÷ 1 PMT FV

- Press CHS PV 12 RCL n - n 0 PMT FV STO 0 RCL n

- Key in the number of payments which are skipped and press - n 1 PMT 0 PV FV STO + 0.

- Press 0 PMT 12 n 100 PV FV RCL PV + CHS f CLEAR FIN i

-

Key in the total number of years in the loan and press n

-

Key in the loan amount and press PV PMT RCL 0 to obtain the monthly payment amount when the payment is made at the end of the month.

- Press CHS FV 0 PMT 1 n

- Key in the annual interest rate as a percent and press g 12÷ PV to find the monthly payment amount when the payment is made at the beginning of the month.

Example: A bulldozer worth 100,000 is being purchased in September. The first payment is due one month later, and payments will continue over a period of 5 years. Due to the weather, the machinery will not be used during the winter months, and the purchaser does not wish to make payments during January, February, and March (months 4 thru 6). If the current interest rate is14\%$ , what is the monthly payment necessary to amortize the loan?

| Keystrokes | Display | |

| g ENDf CLEAR FIN3 n | 3.00 | Number of payment made before a group of payments is skipped. |

| 14 g 12÷1 PMT FV CHS PV12 RCL n - n0 PMT FV STO 0RCL n 3 - n1 PMT 0 PV FVSTO + 00 PMT 12 n100 PV FVRCL PV + CHSf CLEAR FIN i5 n 100000 PVPMT RCL 0 ÷ | 3,119.98 | Monthly payment in arrears. |

Savings

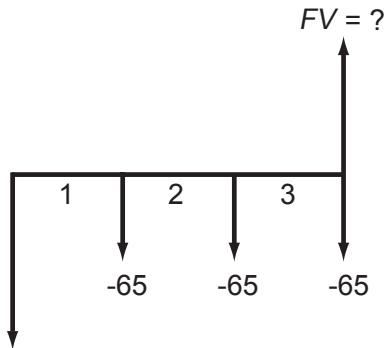

Initial Deposit with Periodic Deposits

Given an initial deposit into a savings account, and a series of periodic deposits coincident with the compounding period, the future value (or accumulated amount) may be calculated as follows:

- Press g END and press f CLEAR FIN

- Key in the initial investment and press CHS PV

- Key in the number of additional periodic deposits and press n

- Key in the periodic interest rate and press i

- Key in the periodic deposit and press CHS PMT

- Press FV to determine the value of the account at the end of the time period.

Example: You have just opened a savings account with a 200 deposit. If you deposit 50 a month, and the account earns 5 1/4 % compounded monthly, how much will you have in 3 years?

| Keystrokes | Display | |

| g ENDf CLEAR FIN200 CHS PV3 g 12x5.25 g 12÷50 CHS PMT FV | 2,178.94 | Value of the account. |

Note: If the periodic deposits do not coincide with the compounding periods, the account must be evaluated in another manner. First, find the future value of the initial deposits and store it. Then use the procedure for compounding periods different from payment periods to calculate the future value of the periodic deposits. Recall the future value of the initial deposit and add to obtain the value of the account.

Number of Periods to Deplete a Savings Account or to Reach a Specified Balance.

Given the current value of a savings account, the periodic interest rate, the amount of the periodic withdrawal, and a specified balance, this procedure determines the number of periods to reach that balance (the balance is zero if the account is depleted).

- Press g END and press f CLEAR FIN

- Key in the value of the savings account and press CHS PV

- Key in the periodic interest rate and press i

- Key in the amount of the periodic withdrawal and press PMT

- Key in the amount remaining in the account and press FV. This step may be omitted if the account is depleted (FV=0).

- Press to determine the number of periods to reach the specified balance.

Example: Your savings account presently contains 18,000 and earns 5 1/4% compounded monthly. You wish to withdraw 300 a month until the account is depleted. How long will this take? If you wish to reduce the account to $5,000, how many withdrawals can you make?

| Keystrokes | Display | |

| g ENDf CLEAR FIN18000 CHS PV5.25 g 12÷300 PMT n | 71.00 | Months to deplete account. |

| 5000 FV n | 53.00 | Months to reduce the account to $5,000 |

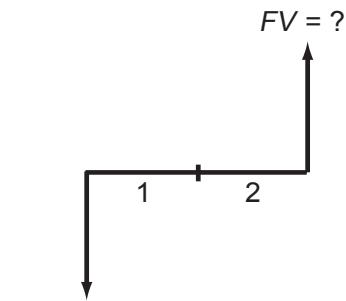

Periodic Deposits and Withdrawals

This section is presented as a guideline for evaluating a savings plan when deposits and withdrawals occur at irregular intervals. One problem is given, and a step by step method for setting up and solving the problem is presented:

Example: You are presently depositing 50 and the end of each month into a local savings and loan, earning 5 1/2% compounded monthly. Your current balance is 1023.25. How much will you have accumulated in 5 months?

The cash flow diagram looks like this:

PV=-1023.25

| Keystrokes | Display | |

| g ENDf CLEAR FIN50 CHS PMT5.5 g 12÷1023.25 CHS PV5 n FV | 1,299.22 | Amount in account. |

Now suppose that at the beginning of the 6th month you withdrew $80.

What is the new balance?

| Keystrokes | Display | |

| 80 - | 1,219.22 | New balance. |

You increase your monthly deposit to (65. How much will you have in 3 months?

The cash flow diagram looks like this:

PV = -1219.22

| Keystrokes | Display | |

| CHS PV 65 CHS PMT 3 n FV | 1,431.95 | Account balance. |

Suppose that for 2 months you decide not to make a periodic deposit.

What is the balance in the account?

PV = -1431.95

| Keystrokes | Display | |

| CHS PVT2 n0 PMT FV | 1,455.11 | Account balance. |

This type of procedure may be continued for any length of time, and may be modified to meet the user's particular needs.

Savings Account Compounded Daily

This HP 12C program determines the value of a savings account when interest is compounded daily, based on a 365 day year. The user is able to

calculate the total amount remaining in the account after a series of transactions on specified dates.

| KEYSTROKES | DISPLAY |

| f P/R | |

| f CLEAR PRGM | 00- |

| CHS | 01- 16 |

| PV | 02- 13 |

| R↓ | 03- 33 |

| 3 | 04- 3 |

| 6 | 05- 6 |

| 5 | 06- 5 |

| ÷ | 07- 10 |

| i | 08- 12 |

| R↓ | 09- 33 |

| STO 0 | 10- 44 0 |

| RCL PV | 11- 15 13 |

| CHS | 12- 16 |

| R/S | 13- 31 |

| STO 2 | 14- 44 2 |

| R↓ | 15- 33 |

| STO 1 | 16- 44 1 |

| RCL 0 | 17- 45 0 |

| RCL 1 | 18- 45 1 |

| g ΔDYS | 19- 43 26 |

| n | 20- 11 |

| FV | 21- 15 |

| f RND | 22- 42 14 |

| FV | 23- 15 |

| ENTER | 24- 36 |

| RCL PV | 25- 45 13 |

| + | 26- | 40 |

| STO + 3 | 27-44 40 3 | |

| RCL FV | 28- 45 15 | |

| RCL 2 | 29- 45 2 | |

| + | 30- | 40 |

| CHS | 31- | 16 |

| PV | 32- | 13 |

| RCL 1 | 33- 45 1 | |

| STO 0 | 34- 44 0 | |

| RCL PV | 35- 45 13 | |

| CHS | 36- | 16 |

| g GTO 13 | 37-43, 33 13 | |

| f P/R | ||

| REGISTER | ||

| n: Δdays | i: i/365 | |

| PV: Used | PMT: 0 | |

| FV: Used | R0: Initial date | |

| R1: Next date | R2: $ amount | |

| R3: Interest | R4-R4: Unused | |

- Key in the program

- Press f CLEAR REG and press g M.DY.

- Key in the date (MM.DDYYYY) of the first transaction and press ENTER.

- Key in the annual nominal interest rate as a percentage and press ENTER

- Key in the amount of the initial deposit and press R/S

- Key in the date of the next transaction and press ENTER

- Key in the amount of the transaction (positive for money deposited, negative for cash withdrawn) and press R/S to determine the amount in the account.

- Repeat steps 6 and 7 for subsequent transactions.

-

To see the total interest to date, press RCL 3.

-

For a new case press f PRGM and go to step 2.

Example: Compute the amount remaining in this 5.25% account after the following transactions:

- January 19, 1981 deposit $125.00

- February 24, 1981 deposit $60.00

- March 16, 1981 deposit $70.00

- April 6, 1981 withdraw $50.00

- June 1, 1981 deposit $175.00

- July 6, 1981 withdraw $100.00

| Keystrokes | Display | |

| f CLEAR REGg M.D.Y1.191981 ENTER5.25 ENTER125 R/S | 125.00 | Initial Deposit. |

| 2.241981 ENTER60 R/S | 185.65 | Balance in account, February 24, 1981. |

| 3.161981 ENTER70 R/S | 256.18 | Balance in account, March 16, 1981. |

| 4.061981 ENTER50 R/S | 206.95 | Balance in account, April 6 1981. |

| 6.0111981 ENTER175 R/S | 383.62 | Balance in account, June 1, 1981. |

| 7.061981 ENTER100 R/S | 285.56 | Balance in account, July 6, 1981. |

| RCL 3 | 5.56 | Total interest. |

Compounding Periods Different From Payment Periods

In financial calculations involving a series of payments equally spaced in time with periodic compounding, both periods of time are normally equal and coincident. This assumption is preprogrammed into the HP 12C.

I savings plans however, money may become available for deposit or investment at a frequency different from the compounding frequencies offered. The HP 12C can easily be used in these calculations. However, because of the assumptions mentioned the periodic interest rate must be adjusted to correspond to an equivalent rate for the payment period.

Payments deposited for a partial compounding period will accrue simple interest for the remainder of the compounding period. This is often the case, but may not be true for all institutions.

These procedures present solutions for future value, payment amount, and number of payments. In addition, it should be noted that only annuity due (payments at the beginning of payment period) calculations are shown since this is the most common in savings plan calculations.

To calculate the equivalent payment period interest rate, information is entered as follows:

- Press g REG and press f CLEAR FIN

- Key in the annual interest rate (as a percent) and press ENTER

- Key in the number of compounding periods per year and press n ÷

- Key in 100 and press PV FV

- Key in the number of payments (deposits) per year and press n i f CLEAR FIN i

The interest rate which corresponds to the payment period is now in register "i" and you are ready to proceed.

Example 1: Solving for future value.

Starting today you make monthly deposits of (25 into an account paying 5% compounded daily (365-day basis). At the end of 7 years, how much will you receive from the account?

| Keystrokes | Display | |

| g BEG f CLEAR FIN 5 ENTER 365 n ÷ i 100 PV FV 12 n i f CLEAR FIN i | 0.42 | Equivalent periodic interest rate. |

| 7 g 12x 25 CHS PMT FV | 2,519.61 | Future value. |

Example 2: Solving for payment amount.

For 8 years you wish to make weekly deposits in a savings account paying 5.5% compounded quarterly. What amount must you deposit each week to accumulate $6000.

| Keystrokes | Display | |

| g BEG f CLEAR FIN 5.5 ENTER 4 n ÷ i 100 PV FV 52 n i f CLEAR FIN i | 0.11 | Equivalent periodic interest rate. |

| 8 ENTER 52 x n 6000 FV PMT | -11.49 | Periodic payment. |

Example 3: Solving for number of payment periods.

You can make weekly deposits of (10 in to an account paying (5.25 \%)compounded daily (365- day basis). How long will it take you to accumulate (\$ 1000)?

| Keystrokes | Display | |

| g BEG f CLEAR FIN 5.25 ENTER 365 n ÷ i 100 PV FV 52 n i f CLEAR FIN i | 0.10 | Equivalent periodic interest rate. |

| 8 CHS PMT 1000 FV n | 96.00 | Weeks. |

Investment Analysis

Lease vs. Purchase

An investment decision frequently encountered is the decision to lease or purchase capital equipment or buildings. Although a thorough evaluation of a complex acquisition usually requires the services of a qualified accountant, it is possible to simplify a number of the assumptions to produce a first approximation.

The following HP-12C program assumes that the purchase is financed with a loan and that the loan is made for the term of the lease. The tax advantages of interest paid, depreciation, and the investment credit which accrues from ownership are compared to the tax advantage of treating the lease payment as an expense. The resulting cash flows are discounted to the present at the firm's after-tax cost of capital.

| KEYSTROKES | DISPLAY | ||

| f | P/R | ||

| f | CLEAR PRGM | 00- | |

| - | 01- | 30 | |

| 1 | 02- | 1 | |

| STO + 0 | 03-44 | 40 0 | |

| RCL 3 | 04- | 45 3 | |

| - | 05- | 30 | |

| x | 06- | 20 | |

| STO 8 | 07- | 44 8 | |

| 1 | 08- | 1 | |

| f | AMORT | 09- | 42 11 |

| STO 1 | 10- | 44 1 | |

| RCL PV | 11- | 45 13 | |

| STO 9 | 12- | 44 9 | |

| RCL PMT | 13- | 45 14 | |

| STO - | 14-44 | 48 0 | |

| RCL n | 15- | 45 | 11 |

| STO 1 | 16-44 | 48 | 1 |

| RCL i | 17- | 45 | 12 |

| STO 2 | 18-44 | 48 | 2 |

| RCL 5 | 19- | 45 | 5 |

| PV | 20- | 13 | |

| RCL 6 | 21- | 45 | 6 |

| n | 22- | 11 | |

| RCL 7 | 23- | 45 | 7 |

| i | 24- | 12 | |

| RCL 0 | 25- | 45 | 0 |

| f SOYD | 26- | 42 | 24 |

| STO + 1 | 27-44 | 40 | 1 |

| RCL 9 | 28- | 45 | 9 |

| PV | 29- | 13 | |

| RCL 0 | 30-45 | 48 | 0 |

| PMT | 31- | 14 | |

| RCL 1 | 32-45 | 48 | 1 |

| n | 33- | 11 | |

| RCL 2 | 34-45 | 48 | 2 |

| i | 35- | 12 | |

| RCL 1 | 36- | 45 | 1 |

| RCL 3 | 37- | 45 | 3 |

| x | 38- | 20 | |

| RCL PMT | 39- | 45 | 14 |

| - | 40- | 30 | |

| RCL 8 | 41- | 45 | 8 |

| - | 42- | 30 | |

| RCL 4 | 43 - 45 4 |

| RCL 0 | 44 - 45 0 |

| y' | 45 - 21 |

| ÷ | 46 - 10 |

| STO + 2 | 47-44 40 2 |

| g GTO 00 | 48-43, 33 00 |

| f P/R | |

| REGISTER | |

| n: Used | i: Used |

| PV: Used | PMT: Used |

| FV: 0 | R0: Used |

| R1: Used | R2: Purch. Adv. |

| R3: Tax | R4: Discount |

| R5: Dep. Value | R6: Dep. life |

| R7: Factor (DB) | R8: Used |

| R9: Used | R.0: Used |

| R.1: Used | R.2: Used |

| R.3: Unused | |

Instructions:

- Key in the program.

-Select the depreciation function and key in at line 26. - Press g END and press f CLEAR REG

- Input the following information for the purchase of the loan:

-Key in the number of years for amortization and press n.

-Key in the annual interest rate and press i.

-Key in the loan amount (purchase price) and press CHS PV

-Press PMT to find the annual payment.

- Key in the marginal effective tax rate (as a decimal) and press STO 3.

- Key in the discount rate (as a decimal) or cost of capital and press ENTER 1 + STO 4.

- Key in the depreciable value and press STO 5.

-

Key in the depreciable live and press STO 6.

-

For declining balance depreciation, key in the depreciation factor (as a percentage) and press STO 7.

- Key in the total first lease payment (including any advance payments) and press ENTER 1 RCL 3 - x STO 2.

- Key in the first year's maintenance expense that would be anticipated if the asset was owned and press. If the lease contract does not include maintenance, then it is not a factor in the lease vs. purchase decision and 0 expense should be used.

- Key in the next lease payment and press R/S. During any year in which a lease payment does not occur (e.g. the last several payments of an advance payment contract) use 0 for the payment.

- Repeat steps 10 and 11 for all maintenance expenses and lease payments over the term of the analysis. Optional - If the investment tax credit is taken, key in the amount of the credit after finishing steps 10 and 11 for the year in which the credit is taken and press GTO 43 R/S. Continue steps 10 and 11 for the remainder of the term.

- After all the lease payments and expenses have been entered (steps 10 and 11), key in the lease buy back option and press ENTER 1 RCL 3 - x GTO 43 R/S. If no buy back option exists, use the estimated salvage value of the purchased equipment at the end of the term.

- To find the net advantage of owning press RCL 2. A negative value represents a net lease advantage.

Example: Home Style Bagel Company is evaluating the acquisition of a mixer which can be leased for 1700 a year with the first and last payments in advance and a 750 buy back option at the end of 10 years (maintenance is included).

The same equipment could be purchased for 10,000 with a 12% loan amortized over 10 years. Ownership maintenance is estimated to be 2% of the purchase price per year for the first for years. A major overhaul is predicted for the 5th year at a cost of 1500. Subsequent yearly maintenance of 3% is estimated for the remainder of the 10-year term. The company would use sum of the years digits depreciation on a 10 year life with $1500 salvage value. An accountant informs management to take the 10% capital investment tax credit at the end of the second year and to figure the cash flows at a 48% tax rate. The after tax cost of capital (discounting rate) is 5 percent.

Because lease payments are made in advance and standard loan payments are made in arrears the following cash flow schedule is appropriate for a lease with the last payment in advance.

| Year | Maintenance | Lease Payment | Tax Credit | Buy Back |

| 0 | 1700+700 | |||

| 1 | 200 | 1700 | ||

| 2 | 200 | 1700 | 1000 | |

| 3 | 200 | 1700 | ||

| 4 | 200 | 1700 | ||

| 5 | 1500 | 1700 | ||

| 6 | 300 | 1700 | ||

| 7 | 300 | 1700 | ||

| 8 | 300 | 1700 | ||

| 9 | 300 | 0 | 750 | |

| 10 | 300 | 0 |

| Keystrokes | Display | |

| g BEG f CLEAR REG | 0.00 | |

| 10 n 12 i 10000 CHS PV | -10,000.00 | Always use negative loan amount. |

| PMT | 1,769.84 | Purchase payment. |

| .48 STO 3 | 0.48 | Marginal tax rate. |

| .05 ENTER 1 + STO 4 | 1.05 | Discounting factor. |

| 10000 ENTER 1500 - STO 5 | 8,500.00 | Depreciable value. |

| 10 STO 6 | 10.00 | Depreciable life. |

| 1700 ENTER + | 3,400.00 | 1st lease payment. |

| 1 RCL 3 - x STO 2 | 1,768.00 | After-tax expense. |

| 200 ENTER 1700 R/S | 312.36 | Present value of 1st year's net purchase. |

| 200 ENTER 1700 R/S | 200.43 | 2nd year's advantage. |

| 1000 g GTO 43 | 1,000.00 | Tax credit. |

| R/S | 907.03 | Present value of tax credit. |

| 200 ENTER 1700 R/S | 95.05 | 3rd year. |

| 200 ENTER 1700 R/S | -4.38 | 4th year. |

| 200 ENTER 1700 R/S | -628.09 | 5th year. |

| 200 ENTER 1700 R/S | -226.44 | 6th year. |

| 200 ENTER 1700 R/S | -309.48 | 7th year. |

| 200 ENTER 1700 R/S | -388.81 | 8th year. |

| 300 ENTER 0 R/S | -1,034.72 | 9th year. |

| 300 ENTER 0 R/S | -1,080.88 | 10th year. |

| 750 ENTER | 750.00 | Buy back. |

| 1 RCL 3 - x | 390.00 | After tax buy back expense. |

| g GTO 43 R/S | 239.43 | Present value. |

| RCL 2 | -150.49 | Net lease advantage. |

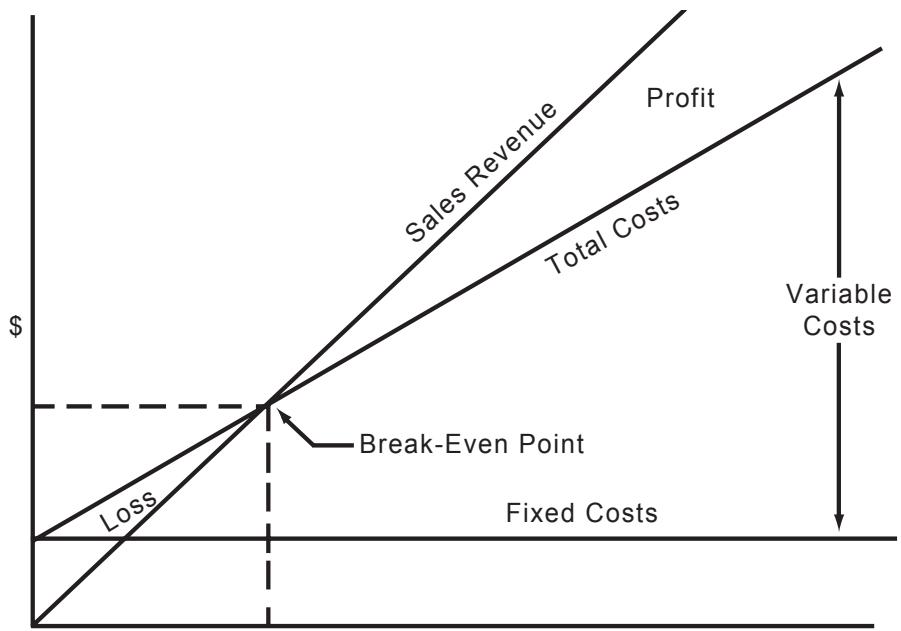

Break-Even Analysis

Break-even analysis is basically a technique for analyzing the relationships among fixed costs, variable costs, and income. Until the break even point is reached at the intersection of the total income and total cost lines, the producer operates at a loss. After the break-even point each unit produced and sold makes a profit. Break even analysis may be represented as follows.

The variables are: fixed costs (F) , Sales price per unit (P) , variable cost per unit (V) , number of units sold (U) , and gross profit (GP) . One can readily evaluate GP , U or P given the four other variables. To calculate the break-even volume, simply let the gross profit equal zero and calculate the number of units sold (U) .

To calculate the break-even volume:

- Key in the fixed costs and press ENTER

- Key in the unit price and press ENTER

- Key in the variable cost per unit and press - .

- Press ÷ to calculate the break-even volume.

To calculate the gross profit at a given volume:

- Key in the unit price and press ENTER

- Key in the variable cost per unit and press - .

- Key in the number of units sold and press .

- Key in the fixed cost and press - to calculate the gross profit.

To calculate the sales volume needed to achieve a specified gross profit:

- Key in the desired gross profit and press ENTER

- Key in the fixed cost and press + .

- Key in sales price per unit and press ENTER

- Key in the variable cost per unit and press [-] .

- Press 12 to calculate the sales volume.

To calculate the required sales price to achieve a given gross profit at a specified sales volume:

- Key in the fixed costs and press ENTER

- Key in the gross desired and press ENTER

- Key in the specified sales volume in units and press 12 .

- Key in the variable cost per unit and press + to calculate the required sales price per unit.

Example 1: The E.Z. Sells company markets textbooks on salesmanship. The fixed cost involved in setting up to print the books are 12,000. The variable cost per copy, including printing and marketing the books are6.75 per copy. The sales price per copy is $13.00. How many copies must be sold to break even?

| Keystrokes | Display | |

| 12000 ENTER | 12,000.00 | Fixed cost. |

| 13 ENTER | 13.00 | Sales price. |

| 6.75 - ÷ | 1,920.00 | Break-even volume. |

Find the gross profit if 2500 units are sold.

| 13 ENTER | 13.00 | Sales price. |

| 6.75 - | 6.25 | Profit per unit. |

| 2500 × | 15,625.00 | |

| 12000 - | 3,625.00 | Gross profit. |

If a gross profit of (4,500 is desired at a sales volume of 2500 units, what should the sales price be?

| 12000 | ENTER | 12,000.00 | Fixed cost. |

| 4500 | + | 16,500.00 | |

| 2500 | ÷ | 6.60 | |

| 6.75 | + | 13.35 | Sales price per unit to achieve desired gross profit. |

For repeated calculation the following HP-12C program can be used.

| KEYSTROKES | DISPLAY |

| f P/R | |

| f CLEAR PRGM | 00- |

| RCL 3 | 01- 45 3 |

| RCL 2 | 02- 45 2 |

| - | 03- 30 |

| g GTO 00 | 04-43, 33 00 |

| RCL 4 | 05- 45 4 |

| x | 06- 20 |

| RCL 1 | 07- 45 1 |

| - | 08- 30 |

| g GTO 00 | 09-43, 33 00 |

| RCL 5 | 10- 45 5 |

| RCL 1 | 11- 45 1 |

| + | 12- 40 |

| x≥y | 13- 34 |

| ÷ | 14- 10 |

| g GTO 00 | 15-43, 33 00 |

| RCL 1 | 16- 45 1 |

| RCL 5 | 17- 45 5 |

| ÷ | 18- 40 |

| RCL 4 | 19- 45 4 |

| ÷ | 20- 10 |

| RCL 2 | 21- 45 2 |

| + | 22- 40 |

| g GTO 00 | 23-43, 33 00 |

| f P/R | |

| REGISTER | |

| n: Unused | i: Unused |

| PV: Unused | PMT: Unused |

| FV: Unused | R0: Unused |

| R1: F | R2: V |

| R3: P | R4: U |

| R5: GP | R6-R6: Unused |

- Key in the program and store the know variables as follows:

a. Key in the fixed costs, F and press STO 1.

b. Key in the variable costs per unit, V and press STO 2.

c. Key in the unit price, P (if known) and press STO 3.

d. Key in the sales volume, U , in units (if known) and press STO 4.

e. Key in the gross profit, GP , (if known) and press STO 5.

- To calculate the sales volume to achieve a desired gross profit:

a. Store values as shown in 1a, 1b, and 1c.

b. Key in the desired gross profit (zero for break even) and press STO 5.

c. Press R/S g GTO 10 R/S to calculate the required volume.

- To calculate the gross profit at a given sales volume.

a. Store values as shown in 1a, 1b, 1c, and 1d.

b. Press R/S g GTO 05 R/S to calculate gross profit.

- To calculate the sales price per unit to achieve a desired gross profit at a specified sales volume:

a. Store values as shown in 1a, 1b, 1d, and 1e.

b. Press GTO 16 R/S to calculate the required sales price.

Example 2: A manufacturer of automotive accessories produces rear view mirrors. A new line of mirrors will require fixed costs of 35,00 to produce. Each mirror has a variable cost of8.25. The price of mirrors is tentatively set at $12.50 each. What volume is needed to break even?

| Keystrokes | Display | |

| 35000 STO 1 | 35,000.00 | Fixed cost. |

| 8.25 STO 2 | 8.25 | Variable cost. |

| 12.5 STO 3 | 12.50 | Sales price. |

| 0 STO 5 | 0.00 | |

| R/S g GTO 10 R/S | 8,235.29 | Break-even volume is between 8,235 and 8,236 units. |

What would be the gross profit if the price is raised to $14.00 and the sales volume is 10,000 units?

| Keystrokes | Display | |

| 14 STO 3 | 14.00 | Sales price. |

| F and V are already stored. | ||

| 10000 STO 4 | 10,000.00 | Volume. |

| R/S g GTO 05 R/S | 22,500.00 | Gross Profit. |

Operating Leverage

The degree of operating leverage (OL) at a point is defined as the ratio of the percentage change in net operating income to the percentage change in units sold. The greatest degree of operating leverage is found near the break even point where a small change in sales may produce a very large increase in profits. Likewise, firms with a small degree of operating leverage are operating farther from the break even point, and they are relatively insensitive to changes in sales volume.

The necessary inputs to calculate the degree of operating leverage and fixed costs (F) , sales price per unit (P) , variable cost per unit (V) and number of units (U) .

The operating leverage may be readily calculated as follows:

- Key in the sales price per unit and press ENTER

-

Key in the variable cost per unit and press - .

-

Key in the number of units and press x ENTER ENTER

- Key in the fixed cost and press -÷ to obtain the operating leverage.

Example 1: For the data given in example 1 of the Break-Even Analysis section, calculate the operating leverage at 2000 units and at 5000 units when the sales price is $13 a copy

| Keystrokes | Display | |

| 13 ENTER | 13.00 | Price per copy. |

| 6.75 - | 6.25 | Profit per copy. |

| 2000 x ENTER | 25.00 | Close to break-even point. |

| ENTER 12000 - ÷ | ||

| 13 ENTER | 13.00 | Price per copy. |

| 6.75 - | 6.25 | Profit per copy. |

| 5000 x ENTER | 1.62 | Operating further from the breakeven point and lesssensitive to changes in sales volume. |

| ENTER 12000 - ÷ |

For repeated calculations the following HP-12C program can be used:

| KEYSTROKES | DISPLAY | |

| f | P/R | |

| f | CLEAR PRGM | 00- |

| RCL 3 | 01- 45 3 | |

| RCL 2 | 02- 45 2 | |

| - | 03- 30 | |

| x | 04- 20 | |

| ENTER | 05- 36 | |

| ENTER | 06- 36 | |

| RCL 1 | 07- 45 1 | |

| - | 08- 30 | |

| ÷ | 09- 10 | |

| g | GTO 00 | 10-43, 33 00 |

| f | P/R | |

| REGISTER | |

| n: Unused | i: Unused |

| PV: Unused | PMT: Unused |

| FV: Unused | R0: Unused |

| R1: F | R2: V |

| R3: P | R4-R8: Unused |

- Key in the program.

- Key in and store input variables F, V and P as described in the Break-Even Analysis program.

- Key in the sales volume and press R/S to calculate the operating leverage.

- To calculate a new operating leverage at a different sales volume, key in the new sales volume and press R/S

Example 2: For the figures given in example 2 of the Break-Even Analysis section, calculate the operating leverage at a sales volume of 9,000 and 20,000 units if the sales price is $12.50 per unit.

| Keystrokes | Display | |

| 35000 STO 1 | 35,000.00 | Fixed costs. |

| 8.25 STO 2 | 8.25 | Variable cost. |

| 12.5 STO 3 | 12.50 | Sales price. |

| 9000 R/S | 11.77 | Operating leverage near break-even. |

| 20000 R/S | 1.70 | Operating leverage further from break-even. |

Profit and Loss Analysis

The HP-12C may be programmed to perform simplified profit and loss analysis using the standard profit income formula and can be used as a dynamic simulator to quickly explore ranges of variables affecting the profitability of a marketing operation.

The program operates with net income return and operating expenses as percentages. Both percentage figures are based on net sales price.

It may also be used to simulate a company wide income statement by replacing list price with gross sales and manufacturing cost with cost of goods sold.

Any of the five variables: a) list price, b) discount (as a percentage of list price), c) manufacturing cost, d) operating expense (as a percentage), e) net profit after tax (as a percentage) may be calculated if the other four are known.

Since the tax rage varies from company to company, provision is made for inputting your applicable tax rate. The example problem uses a tax rate of 48% .

| KEYSTROKES | DISPLAY | ||

| f | P/R | ||

| f | CLEAR PRGM | 00- | |

| RCL5 | 01- | 45 5 | |

| RCL6 | 02- | 45 6 | |

| ÷ | 03- | 10 | |

| RCL4 | 04- | 45 4 | |

| + | 05- | 40 | |

| CHS | 06- | 16 | |

| RCL0 | 07- | 45 0 | |

| + | 08- | 40 | |

| RCL0 | 09- | 45 0 | |

| ÷ | 10- | 10 | |

| g | GTO 00 | 11-43, | 33 00 |

| RCL3 | 12- | 45 3 | |

| RCL1 | 13- | 45 1 | |

| RCL2 | 14- | 45 2 | |

| RCL0 | 15- | 45 0 | |

| ÷ | 16- | 10 | |

| CHS | 17- | 16 | |

| 1 | 18- | 1 | |

| + | 19- | 40 | |

| x | 20- | 20 | |

| R/S | 21- | 31 | |

| ÷ | 22- | 10 | |

| CHS | 23- | 16 | |

| 1 | 24- | 1 | |

| + | 25- | 40 | |

| RCL0 | 26- | 45 0 | |

| x | 27- | 20 | |

| g GTO 00 | 28-43, | 33 0 | |

| ÷ | 29- | 10 | |

| CHS | 30- | 16 | |

| RCL1 | 31- | 45 1 | |

| + | 32- | 40 | |

| RCL1 | 33- | 45 1 | |

| ÷ | 34- | 10 | |

| RCL0 | 35- | 45 0 | |

| x | 36- | 20 | |

| g GTO 00 | 37-43, | 33 00 | |

| RCL5 | 38- | 45 5 | |

| RCL6 | 39- | 45 6 | |

| ÷ | 40- | 10 | |

| - | 41- | 30 | |

| g GTO 00 | 42-43, | 33 00 | |

| RCL4 | 43- | 45 5 | |

| - | 44- | 30 | |

| RCL6 | 45- | 45 6 | |

| x | 46- | 20 | |

| g GTO 00 | 47-43, | 33 00 | |

| f P/R | |||

| REGISTERS | |||

| n: Unused | i: Unused | ||

| PV: Unused | PMT: Unused | ||

| FV: Unused | R0: 100 | ||

| R1: list price | R2: % discount | ||

| R3: mfg. cost | R4: % op. exp. | ||

| R5: % net profit | R6: 1-% tax | ||

| R7-R3: Unused | |||

-

Key in the program and press f CLEAR REG, then key in 100 and press STO 0.

-

Key in 1 and press ENTER, then key in your appropriate tax rate as a decimal and press -STO 6.

3.

a. Key in the list price in dollars (if known) and press STO 1.

b. Key in the discount in percent (if known) and press STO 2.

c. Key in the manufacturing cost in dollars (if known) and press STO 3.

d. Key in the operating expense in percent (if known) and press STO 4.

e. Key in the net profit after tax in percent (if known) and press STO 5.

- To calculate list price:

a. Do steps 2 and 3b, c, d, e above.

b. Press RCL 3 R/S ÷ 1 g GTO 14 R/S ÷ g GTO 00.

- To calculate discount:

a. Do steps 2 and 3a, c, d, e above.

b. Press RCL 3 R/S g GTO 29 R/S

- To calculate manufacturing cost:

a. Do steps 2 and 3a, b, d, e, above.

b. Press GTO 13 R/S g GTO 01 R/S x

- To calculate operating expense:

a. Do steps 2 and 3a, b, c, e, above.

b. Press GTO 12 R/S R/S GTO 38 R/S

- To calculate net profit after tax:

a. Do steps 2 and 3a, b, c, d, above.

Example: What is the net return on an item that is sold for (11.98, discounted through distribution an average of (35\%) and has a manufacturing cost of (\$ 2.50?) The standard company operating expense is (32\%) of net shipping (sales) price and tax rate is (48\%).

| Keystrokes | Display | |

| f CLEAR REG 100 STO 0 | 100.00 | |

| 1 ENTER .48 - STO 6 | 0.52 | 48% tax rate. |

| 11.98 STO 1 | 11.98 | List price () . |

| 35 STO 2 | 35.00 | Discount (%). |

| 2.50 STO 3 | 2.50 | Manufacturing cost () . |

| 32 STO 4 | 32.00 | Operating expenses (%). |

| g GTO 12 R/S R/S | 67.90 | |

| g GTO 43 R/S | 18.67 | Net profit (%). |

If manufacturing expenses increase to $3.25, what is the effect on net profit?

| 3.25 | STO | 3 | 3.25 | Manufacturing cost. | |

| g | GTO | 12 | R/S | R/S | 58.26 |

| g | GTO | 43 | R/S | 13.66 | |

| Net profit reduced to 13.66% | |||||

If the manufacturing cost is maintained at $3.25, how high could the overhead (operating expense) be before the product begins to lose money?

| 0 STO 5 | 0.00 | ||||

| g | GTO | 12 | R/S | R/S | 58.26 |

| g | GTO | 38 | R/S | 58.26 | |

| Maximum operating expense (%). | |||||

At 32 % operating expense and 3.25 manufacturing cost, what should the list price be to generate20 \%$ net profit?

| 20 STO 5 | 20.00 | |

| RCL 3 R/S ÷ | 11.00 | |